Macroeconomic/ geopolitical developments

- Another relatively quiet week for global financial markets from a macroeconomic and geopolitical perspective, but as at the end of February price action across the major asset classes was still volatile.

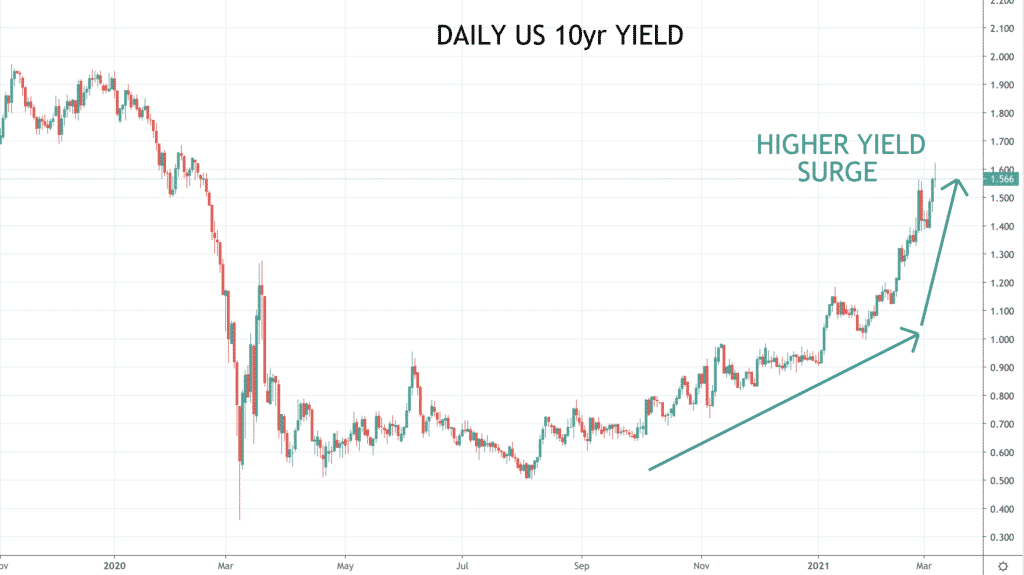

- The ongoing development last week was the continuing surge in global yields, particularly in the US and notably at the longer ends of yield curves, with global yield curves exhibiting bearish steepening.

- This is being driven by ongoing market concerns of strong reflationary pressures leading to inflation.

- Jerome Powell did speak on Thursday, but his still very dovish stance did nothing to quell the inflationary worries of markets.

- We will review the financial markets impacts below in our global financial markets section, with the main effect in the Forex world being a stronger US Dollar, with a mostly negative impact for global stocks indices.

- Despite the release of global PMI data on Monday and Wednesday, the US Employment report on Friday brought the main data influence on markets.

- A better-than-expected US jobs report saw the Non-Farm Payroll element post at 379K jobs added, with consensus closer to 200K.

- This allowed for share averages to stage a rebound from weakness.

- President Biden’s $1.9 trillion COVID relief bill continued its progress passing through the US Senate after markets had closed on Friday, with the House of Representatives expected to approve the plan early this week.

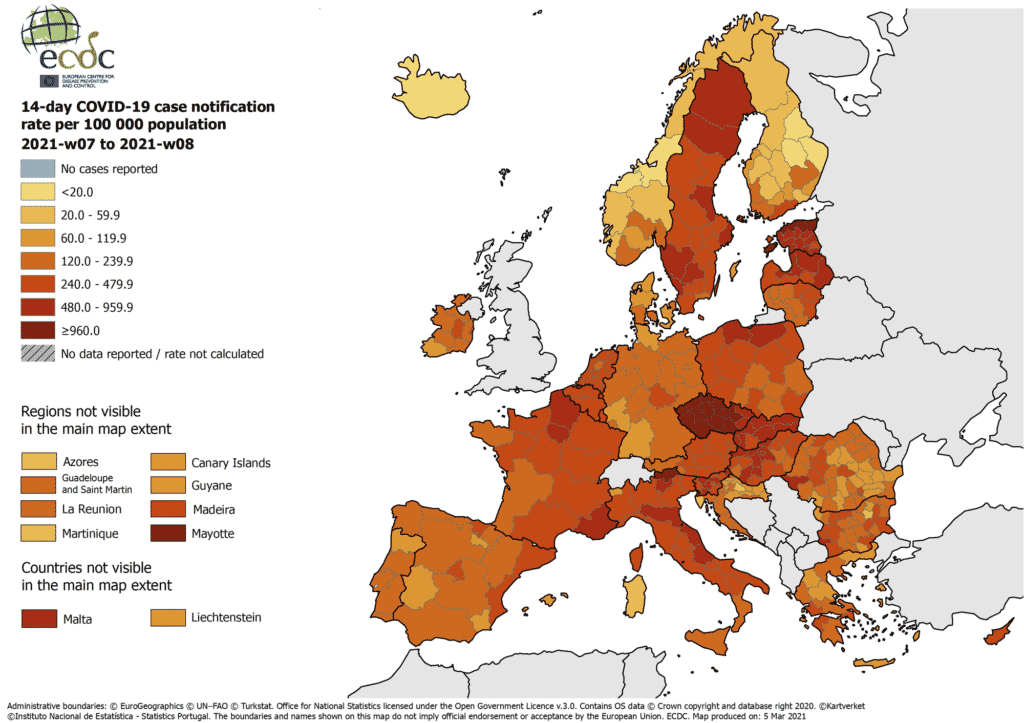

- The European vaccination program continues to improve, but it is still lagging behind the solid vaccination program in the US and the impressive UK rollout.

- The number of cases, hospitalisations and deaths in the UK continues to fall, but there have been rising cases in some parts of Europe, notably eastern and central Europe, but also with some areas of concern in western Europe.

- OPEC+ met and decided to continue to restrict production, the oil price went higher.

Global financial market developments

- The ongoing financial markets development was the extension of the global bond market sell off with worldwide bond markets moving to multi-month and even multi-year yield highs.

- Overall, this has seen an erratic, but mostly negative reaction by major global equity averages, with inflation concerns and the possibility of higher interest rates.

- The US Dollar has extended its surge from February into March, resuming the positive US Dollar recovery theme from early 2021.

- EURUSD has plunged lower.

- The Pound has further weakened with GBPUSD correcting 2021 trends.

- The “risk currencies” performed badly again, with the Australian and New Zealand Dollars plunging further from multi-year highs versus the US Dollar.

- Oil resumed its surge to a new multi-month high as OPEC+ met and decided to continue to restrict production.

- Copper has corrected still lower from multi-year highs, with concerns of inflation and higher yields/ interest rates.

- Gold has edged still lower as the US Dollar has again strengthened.

Key this week

- Geopolitics:

- Watch for the Democrat’s COVID relief bill to be passed by House of Representatives.

- Monitoring COVID-19 cases, hospitalisations and deaths globally (notably in in Europe).

- Central Bank Watch: Bank of England (BoE) Governor Bailey speaks on Monday. We get the Bank of Canada (BoC) and European Central Bank (ECB) interest rate decisions, statements and press conferences on Wednesday and Thursday respectively.

- Macroeconomic data: With the global macroeconomic focus shifting to inflation, the standouts this week are Chinese, US and German CPI.

| Date | Key Macroeconomic Events |

| 08/03/21 | German Industrial Production; BoE Governor Bailey speaks |

| 09/03/21 | Japanese GDP; EU GDP |

| 10/03/21 | Chinese CPI; US CPI; BoC interest rate decision, statement and press conference |

| 11/03/21 | ECB interest rate decision, statement and press conference; US weekly Jobless Claims |

| 12/03/21 | UK Manufacturing and Industrial Production; German CPI; Canadian Employment report |