Q2 corporate earnings season in the States has been little help for US index futures. Despite it being a strong earnings season for positive surprises, the associated boost that markets have been lacking. It means that as earnings season winds down, the positive outlook on the technical analysis will have plenty of heavy lifting to do to keep the bull market running.

- A positive earnings season has done little to lift markets

- Positive technical signals are being tested

Positive US earnings have come with a caveat

As US earnings season begins to wind down (close to 90% of S&P 500 companies have reported now), it is difficult not to feel that the impact on index futures has been somewhat disappointing for investors. US earnings kicked off on the 13th of July with e-mini S&P 500 futures opening at 4510. As I write this, the futures are barely any higher, at 4530.

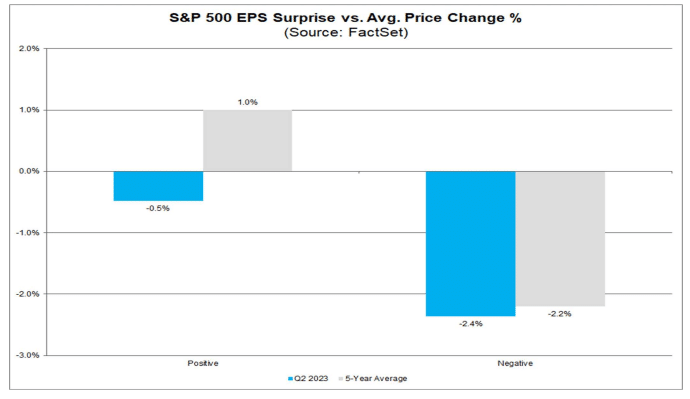

However, this has come with more companies than normal posting better-than-expected results. According to FactSet data, as of 4th August, 79% of companies had beaten estimates on earnings (versus a 5-year average of 77% and a 10-year average of 73%). Earnings have beaten earnings per share (EPS) estimates by an average of 7.2% which is a shade down from the 8.4% 5-year average but better than the 10-year average of 6.4%. So I would say that overall, this is a pretty strong showing from companies across the board.

However, Factset also shows that the price reaction for those beating on earnings from the two days prior to the announcement to the two days post has been on average -0.5%. The average reaction over the past five years has been +1.0%. Positive earnings are causing share prices to fall. But why?

These positive earnings are coming with a caveat. The outlook for Q3 has been more slightly negative than normal. 62% of Q3 earnings guidance has been negative (above the 5-year average of 59%). However, reportedly, analysts are keeping their powder dry on the prospects for Q3, with the net aggregate earnings estimates for the market all but unchanged for Q3 so far.

Perhaps also traders are seeing the recent rally from March of over 20% on the e-mini S&P 500 futures as being a run that may be maturing. The valuation of the S&P 500 is now at 19.2x forward earnings. This is above the 5-year average of 18.6x. Perhaps the market needed an even stronger performance to justify chasing it higher.

Traders seem to be far more interested in the Fed and the data

There might also be another reason for this lack of follow-through in performance on indices. There has been considerable focus on the macro picture recently. As confirmed by Fed Chair Powell at the latest FOMC press conference, the outlook for the Federal Reserve “will continue to take a data-dependent approach”.

Markets are subsequently highly reactive to economic data surprises. Any data that is causing a shift in the view of the Fed for the September decision is going to be market-moving. Looking forward, the Fed speakers will also be garnered the same attention. The result is that this earnings season has had little real impact on the direction of markets.

Technicals also have some heavy lifting to do

Markets have been rallying since March, but the fluctuations that we have seen in US index futures are now testing the credentials of the multi-month bull run. This has been a classic rally in many ways. Consistent higher lows and higher highs, with old breakouts becoming new support. The latest pullback is subsequently into a key band of support. How markets react around here will be telling the health of the rally.

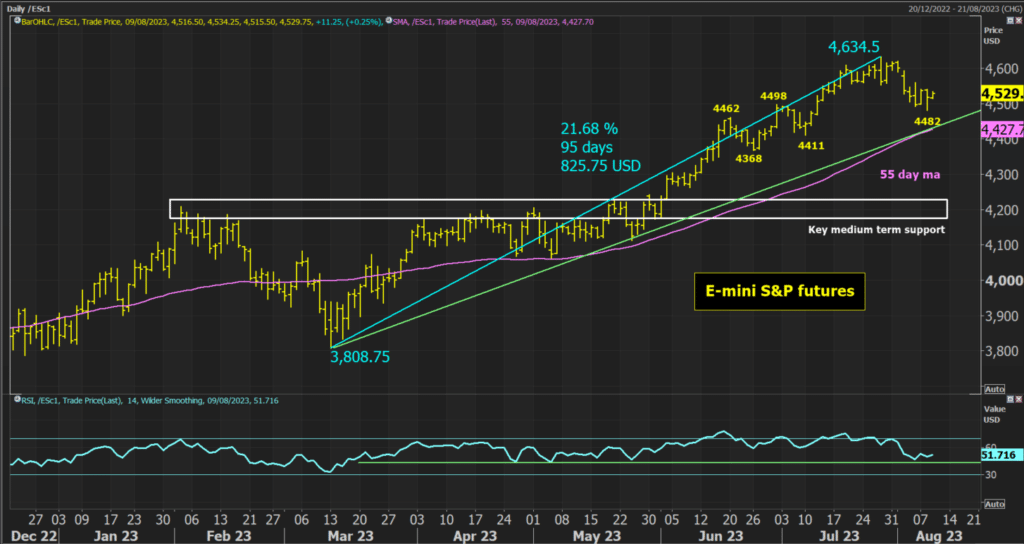

The e-mini S&P 500 futures have pulled back into the breakout band of support between 4462/4498. A near five-month uptrend is also being flanked by the 55-day moving average as a basis of support. The Relative Strength Index continues to find lows between 40/50. This is a crucial moment for the outlook. If the support can hold between 4462/4498 and another higher low form above the 4411 reaction low from mid-July, then this may be seen to be another important buying opportunity within the rally. A move above resistance at 4553/4561 could re-ignite the bull run once more.

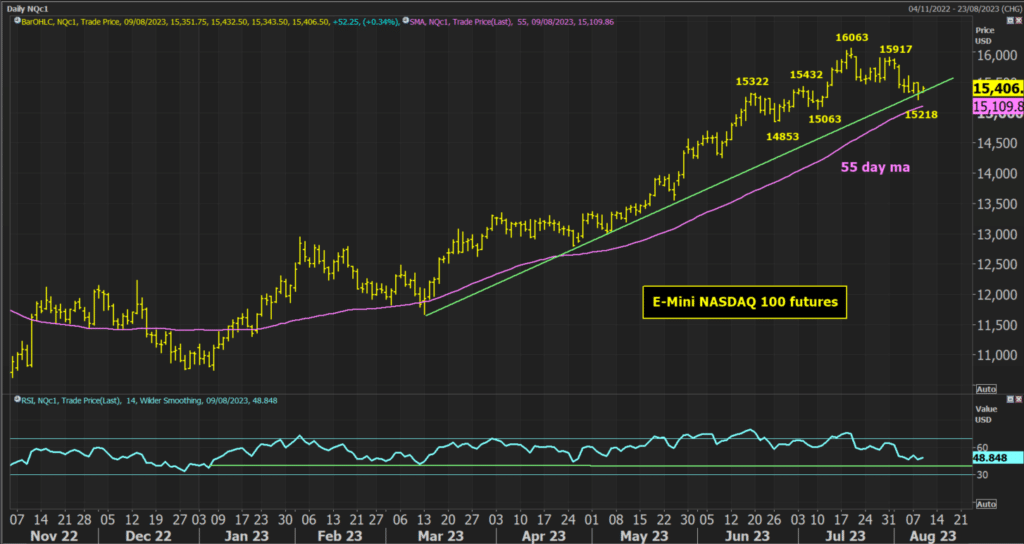

The e-mini NASDAQ 100 futures are arguably at a more important technical crossroads. The support of the five-month uptrend is coming under considerable scrutiny, whilst the rising 55-day moving average which has been an important element of support throughout this time is just below. The RSI is also back towards the 40/45 area where important lows in the price have formed. The futures have dipped briefly below the 15322/15432 support but importantly, so far, the 15063 reaction low is intact. A close below 14853 would confirm the bull run has turned corrective.