Macroeconomic/ geopolitical developments

- US stock averages reached record highs again. Both the S&P 500 and Nasdaq composite closed at all-time highs, propelled by investor optimism regarding potential Federal Reserve rate cuts this year.

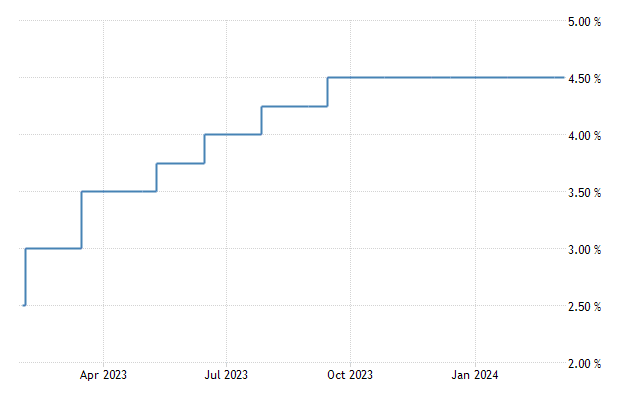

- Fed chair Powell sent mixed messages regarding the central bank’s future monetary policy actions. He said the Fed is nearing the confidence required to consider interest rate cuts but emphasised that such decisions would hinge on the evolving economic outlook and data on inflation and employment.

- The ECB opted to maintain its benchmark interest rates during its March meeting, but they reiterated their commitment to restoring price pressures to the medium-term target.

- There is growing anticipation of a Bank of Japan March rate hike. This would terminate its negative interest rate policy, but there is no unanimous agreement yet.

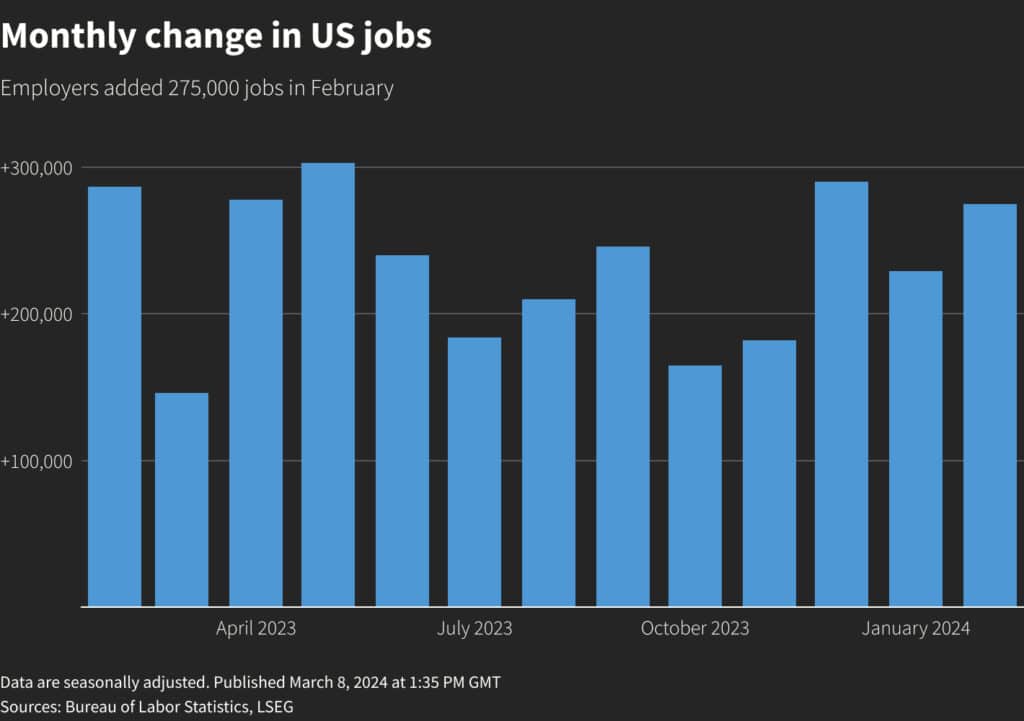

- The US Employment report presented a mixed picture on Friday. Nonfarm payrolls increased by 275,000 during the month, exceeding economists’ expectations, but the unemployment rate edged higher to 3.9%.

Global financial market developments

- Global equity index futures rallied to again post multiyear and new records.

- US and European moved to multi-week low yields.

- The US Dollar Index weakened to multi-week lows.

- Gold futures extended the prior week’s surge to a new record.

- Oil futures posted a week of negative consolidation.

Key this week

Central Bank Watch: Nothing of note from central banks this week, but as ever Fed speakers must be watched.

Macro Data Watch: The standout data for the week will be US CPI on Tuesday, plus we also get the UK Employment report and German CPI earlier that day. US Retails Sales is noteworthy on Thursday, plus the UK, EU and US all release Industrial Production data Wednesday and Friday.

Other Events: The US has moved to Daylight Savings Time on Sunday March 10, so traders from other countries should be aware that US data releases and US market open and closing times may differ in their local time zones.

| Date | Major Macro Data |

| 03/11/2024 | Japan GDP (QoQ, YoY) |

| 03/12/2024 | German CPI (MoM, YoY); UK Employment Report; US CPI (MoM, YoY); |

| 03/13/2024 | UK GDP, Manufacturing and Industrial Production; EU Industrial Production |

| 03/14/2024 | US PPI and Retail Sales |

| 03/15/2024 | US Industrial Production and Michigan Consumer Sentiment Index |