Macroeconomic/ geopolitical developments

- A busy start to the year on the macroeconomic front from the US saw the Fed Minutes echoing recent Fed statements and comments from Fed speakers that interest rates would need to go higher than markets were pricing and stay there longer.

- ADP’s private sector jobs data showed an increase of 235k for December, significantly above expectations, echoed by Friday’s official Nonfarm payrolls data that increased by 223k in December, again above consensus expectations.

- However, unemployment fell to its September 2022 post-pandemic low of 3.5%, whilst average hourly earnings were up 0.3% for December, below consensus.

- The Institute for Supply Management (ISM) Purchasing Managers Index (PMI) data for both Manufacturing and Services were both below expectations, whilst S&P Global PMI data for major European economies mostly beat expectations.

- Falling energy prices in Europe, notably Natural Gas and lower than expected inflation data for the Eurozone were two positives for the European economic region.

- There were reports that Hong Kong would reopen its border to mainland China and that Beijing was contemplating easing borrowing curbs for the property sector.

Global financial market developments

- The major US stock averages were modestly positive within a consolidation range to start 2023.

- European equity indices posted a positive start to 2023, outperforming their US counterparts. Asian averages were mixed, with Japanese indices lower and Chinese markets rallying.

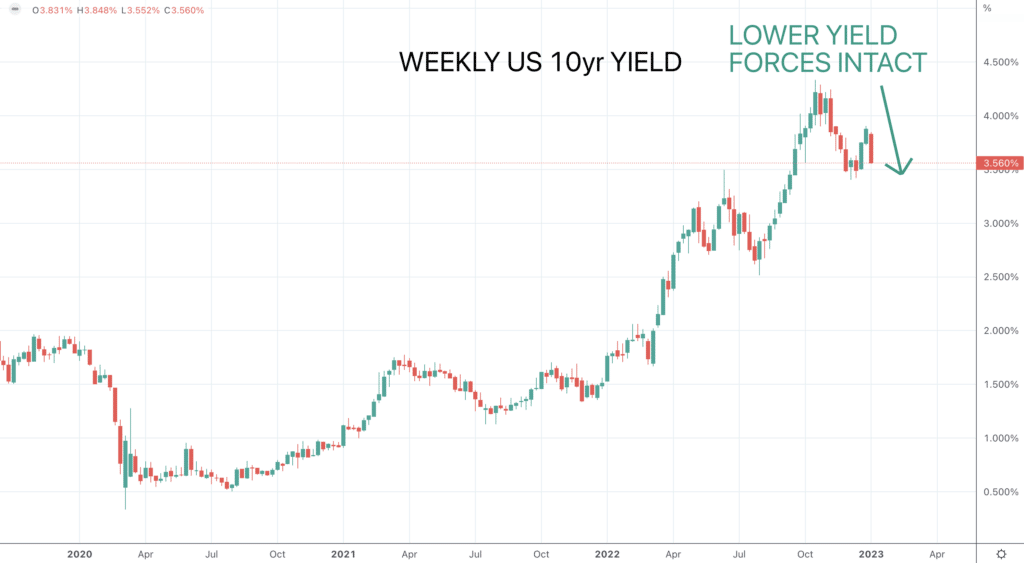

- US Treasury yields plunged (as did European yields).

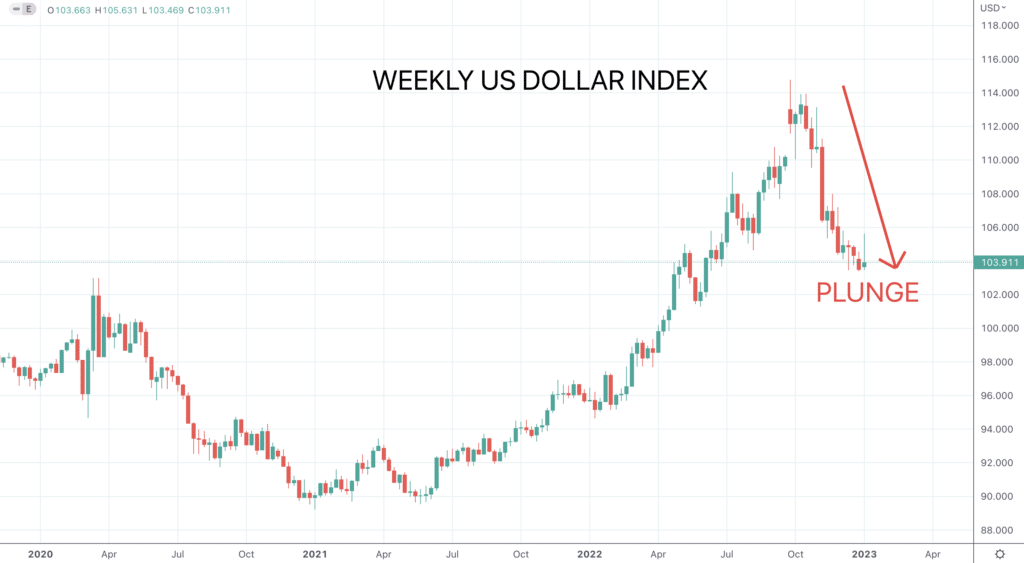

- The US Dollar Index moved back close to multi-month lows.

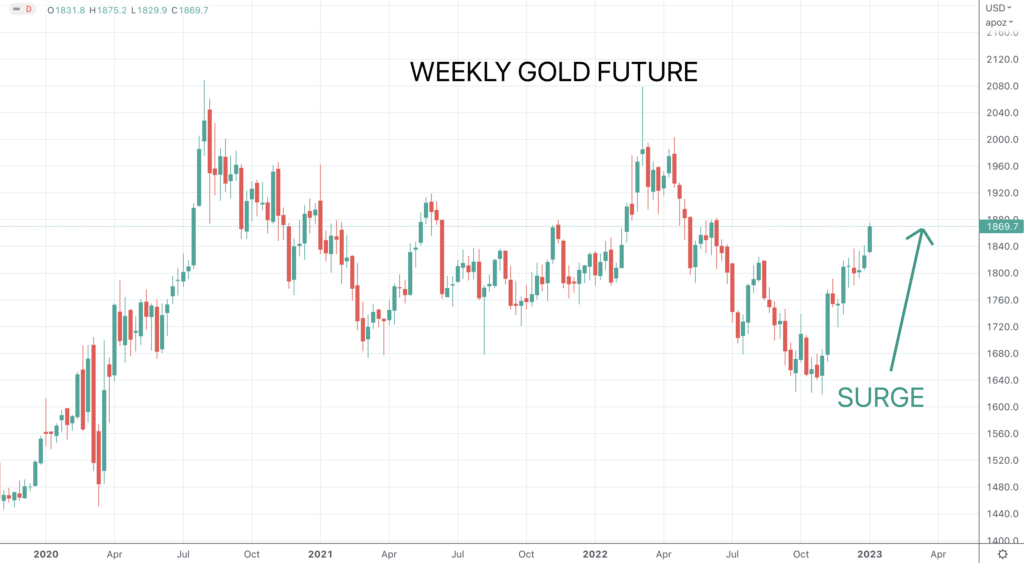

- Gold surged to a multi-month high.

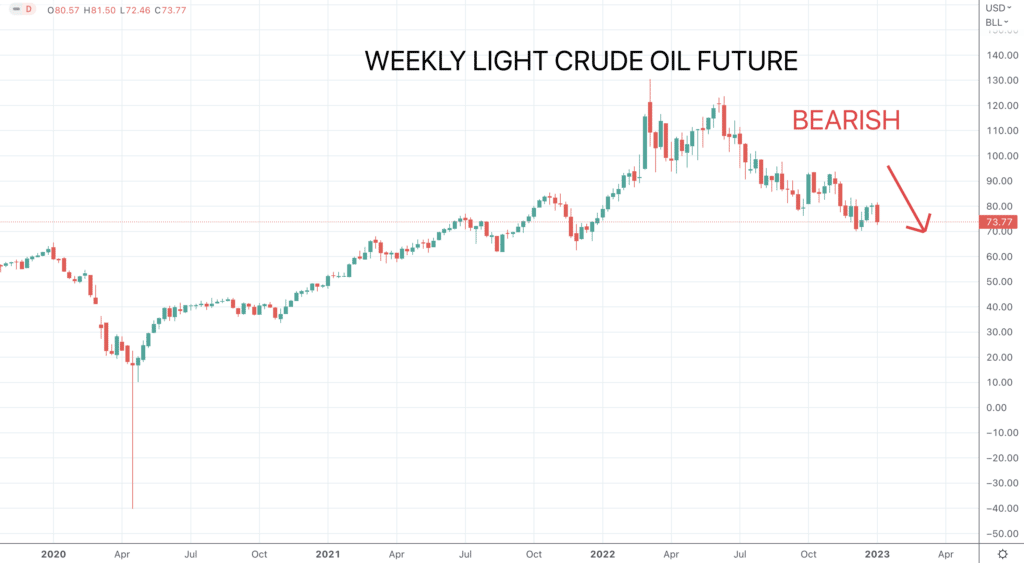

- Oil prices plunged back close to the late 2022 low, retaining bigger negative pressures.

- Copper stayed positive in a broader range phase.

Key this week

- Central Bank Watch: Nothing of note.

- Macroeconomic data: A relatively light data week, BUT with a key release of US CPI on Thursday.

| Date | Key Macroeconomic Events |

| 09/01/23 | EU Unemployment |

| 10/01/23 | Japan CPI |

| 11/01/23 | China CPI |

| 12/01/23 | US CPI |

| 13/01/23 | UK GDP, Industrial & Manufacturing Production; Michigan Consumer Sentiment |