Macroeconomic/ geopolitical developments

- The focus this past week was on the US Federal Open Market Committee (FOMC) interest rate decision, statement and press conference, with a still very dovish stance emphasised again.

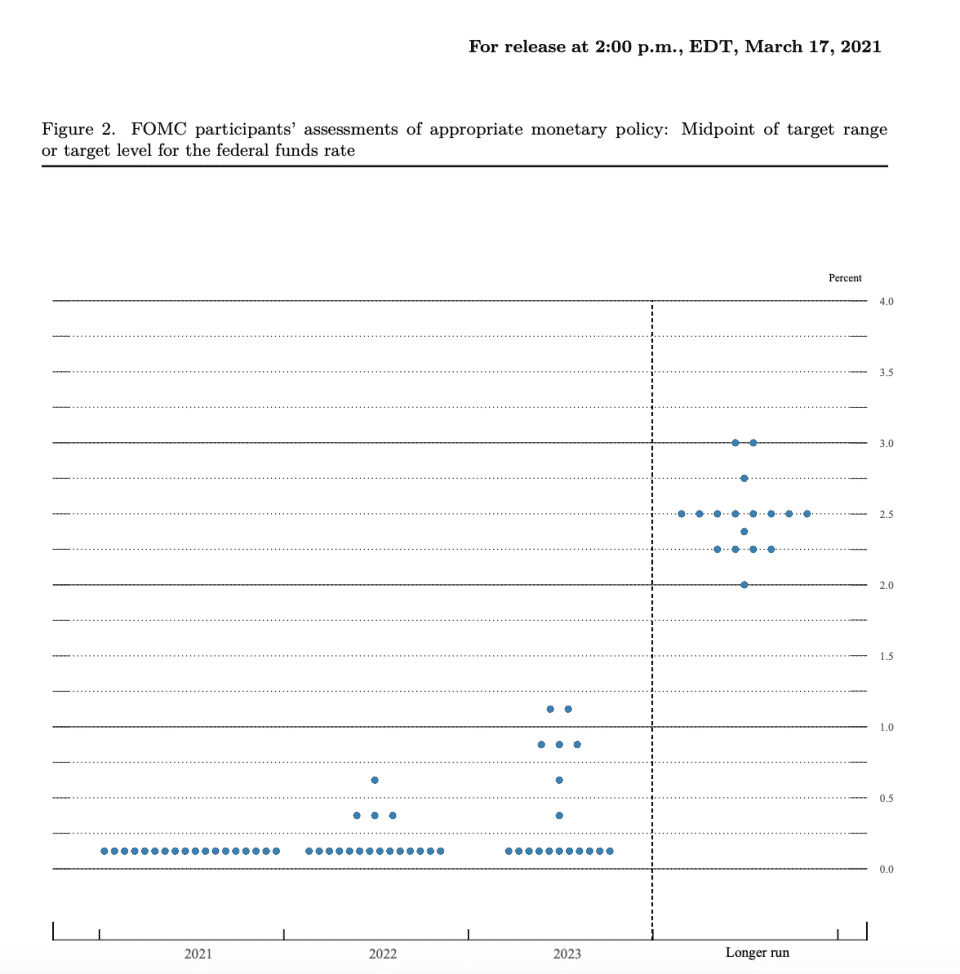

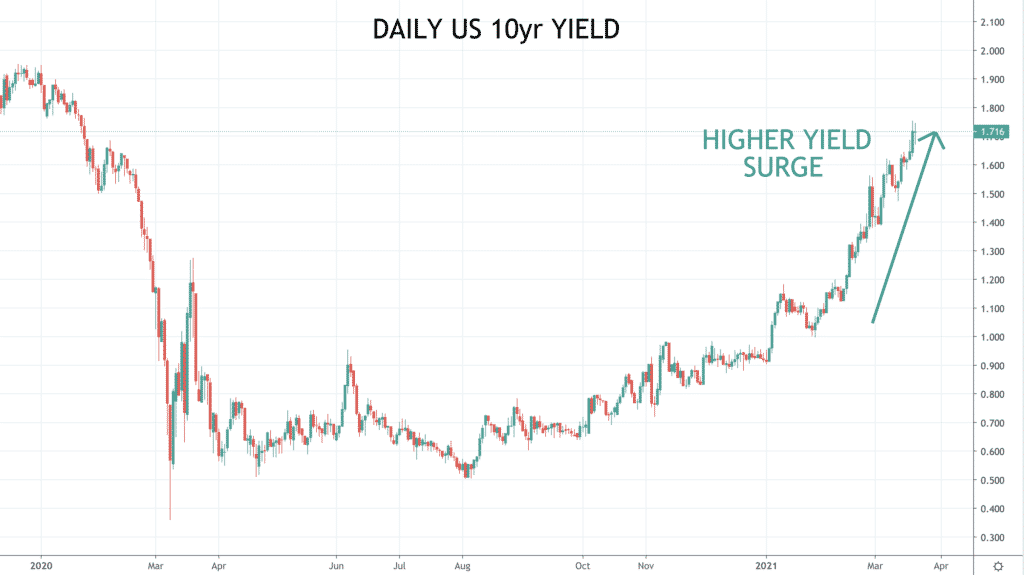

- However, a slight shift in the dot plot chart towards a possibly earlier than expected rate hike in 2022 from some members eventually saw a surge back higher for US Treasury yields (and also for global yields), notably at the longer end of yield curves

- This further highlight inflationary concerns, given ultra-easy monetary policy and the expansive fiscal policy globally, highlighted by the US passing the $1.9 trillion economic relief bill

- This continues to see value stocks pushing higher whilst growth stocks continue to lag and push lower, due to inflation and higher interest rate worries.

- The European vaccination program has resumed after some questioning of the Astra Zeneca vaccine, but continues to lag behind the rollouts in the US and the UK.

- The number of cases, hospitalisations and deaths in the UK continues to fall.

- But cases in some parts of Europe are on the rise again, which has seen France join Italy with moves to another lockdown

- Concerns are that other European nations may also be poised to reintroduce more rigorous measures.

Global financial market developments

- The global bond market sell off led by US bond markets hitting multi-year yield highs continues to be a key focus for global financial markets, the US bond market is the dog that is wagging the tail of the other asset classes.

- Major global stock indices rebounded and then stalled last week with European averages hitting record and multi-month highs.

- US indices were initially led higher by the Dow Jones Industrial Average and the S&P 500 hitting new record highs, but notably setting back at the end of the week.

- The growth stock heavy Nasdaq 100 and Composite resumed their more negative themes evident over the past month.

- The US Dollar has tried to resume its recovery from February-March after initially setting back immediately after Wednesday’s Fed announcement, attempting to renew the positive US Dollar trend evident in 2021

- EURUSD has started to resume its negative theme and the Pound also moved lower with GBPUSD looking to further correct the 2021 bull move.

- The “risk currencies” have started to reverse the prior March rebounds with the Australian and New Zealand Dollars still vulnerable versus the US Dollar.

- But the US Dollar is vulnerable versus the Canadian Dollar, the Canadian Dollar bolstered by the rebounding oil price.

- Oil saw a significant sell off late last week and then a rebound, but the underlying theme is bullish.

- Copper has been sideways since its rebound from the negative correction from a multi-year high.

- Gold staged a further rebound but remains vulnerable as the US Dollar retains an underlying bull tone.

Key this week

- Geopolitics:

- The US switched last weekend to Daylight Savings Time, which means the time between New York (CET) and the UK (GMT) is only 4 hours for another week.

- Watching COVID-19 cases, hospitalisations and deaths globally (notably in Europe).

- Monitoring for possible new lockdown restrictions, particularly in Europe.

- Central Bank Watch:

- The People’s Bank of China (PBoC) interest rate decision is early Monday.

- Fed Chairman JeromePowell speaks at the Bank for International Settlement summit on Monday and testifies to Congressional committees on Tuesday and Wednesday (along with Treasury Secretary Yellen).

- The Bank of Japan (BoJ) Meeting Minutes are released Wednesday.

- There are numerous Fed speakers throughout the week.

- Macroeconomic data: Key this week will be the Markit Economic Flash Manufacturing and Services Purchasing Managers Index (PMI) out on Wednesday and Friday’s release of the US Personal Consumption and Expenditure data (with the PCE deflator the Fed’s preferred inflation measure).

| Date | Key Macroeconomic Events |

| 22/03/21 | PBoC interest rate decision; Fed Chairman Jerome Powell speaks at the Bank for International Settlement summit |

| 23/03/21 | UK Employment report; Jerome Powell testifies to Congressional committees |

| 24/03/21 | Global Markit Economic Flash Manufacturing and Services PMI; Bank of Japan (BoJ) Meeting Minutes; UK inflation data (including CPI); US Durable Goods Orders; Jerome Powell testifies to Congressional committees |

| 25/03/21 | German Gfk Consumer Confidence Survey; US Gross Domestic Product (GDP); US weekly Jobless Claims |

| 26/03/21 | UK Retail Sales; German IFO Survey; US Personal Consumption and Expenditure data |