Inflation has always been a crucial factor in how central banks devise their monetary policy positions. As the Federal Reserve has paused its rate hikes amid mounting signs of recession, the FOMC members will be hoping that inflation begins to accelerate lower. The monthly data suggest they may just get their wish in the coming months, whilst April’s CPI will also be cheered. For the US dollar bulls, the situation looks to be quite the opposite.

- Inflation remains as crucial as ever for central banks such as the Federal Reserve.

- Trends in inflation reduction have been sluggish but this is about to change.

- April US CPI dropped more than expected.

- Marekt reaction shows a weaker USD

The Fed still needs inflation to reduce

According to its dual mandate, “stable prices” (i.e. controlling inflation) is one of the two driving forces of the Fed’s monetary policy decisions. The other part is the promotion of “maximum employment”, in addition to the longer-term aim of “moderate long-term interest rates”.

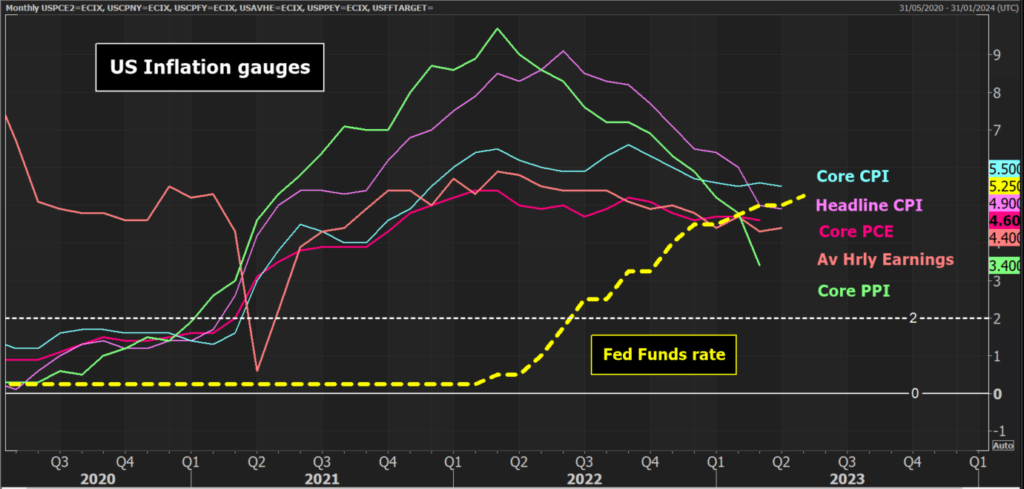

In the past two and a half years, achieving “stable prices” has proved to be somewhat tricky. However, with inflation indicators now tracking lower for several months, there is a feeling that the rate hikes are doing their job.

After the most aggressive monetary policy tightening in four decades, it appears as though the Federal Reserve has finally hiked for the final time in this cycle.

The 25bps increase in the Fed Funds rate to a range of 5.00%/5.25% came with key adjustments to the language in the FOMC statement that suggested it would take a lot to hike any more in this cycle.

However, with Fed Chair Powell not ready to call victory in the fight against high inflation, this requires the trends to continue lower in the months to come.

The path lower is sluggish but will accelerate in the coming months

So the big question is whether inflation is decisively falling. Inflation has been stubbornly higher than many had been hoping in recent months. However, there was a mild downside surprise in today’s US CPI (see below), but this is also likely to be followed by a sharper decline in the months to come.

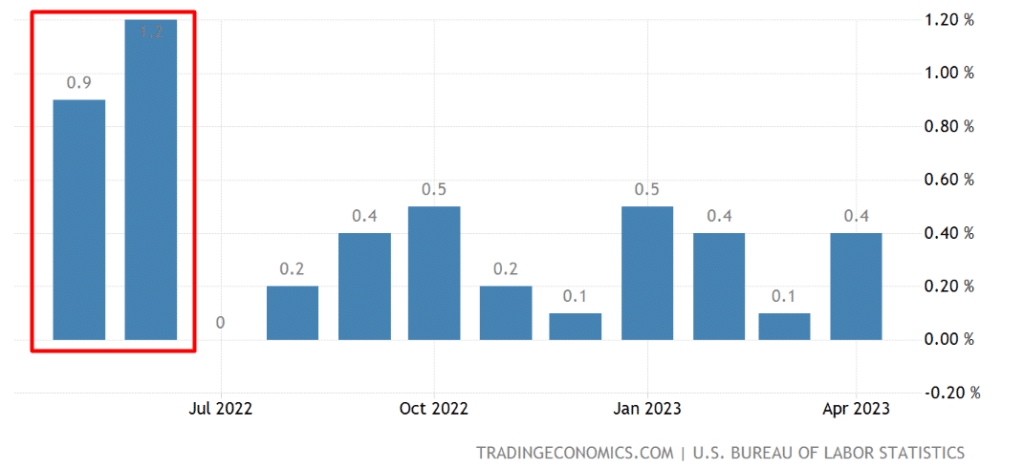

Looking at the month-on-month readings, in the next two months, the huge monthly increases of +0.9% in May 2022 and 1.2%$ in June 2022 will drop out of the data.

If the monthly growth continues around +0.4% for the next couple of months, this would leave year-on-year headline CPI dropping to 4.4% in May and then to 3.6% in June.

Whilst this is still not back towards target, this is a far healthier-looking inflation path for the Fed to be able to consider cutting interest rates perhaps later in the year.

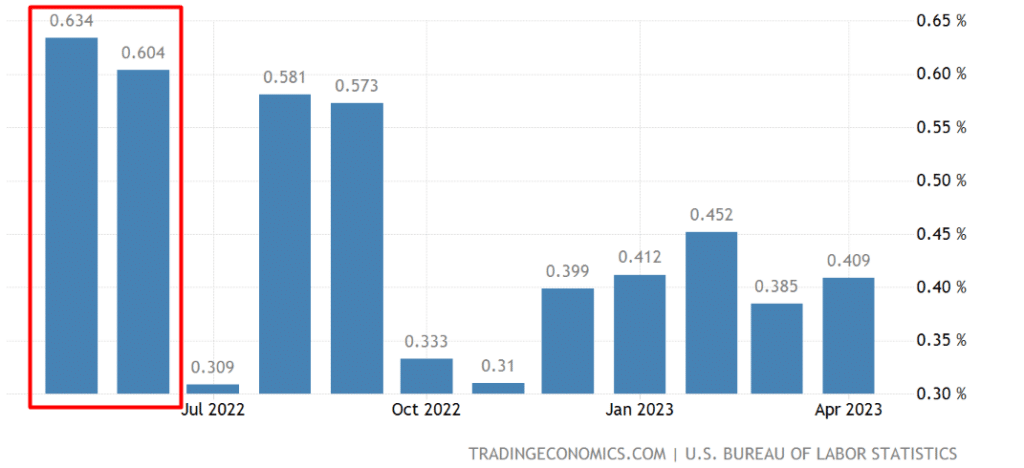

However, as the volatile energy costs continue to drop out of the headline, the core CPI remains far more stubborn. This is reflected in the month-on-month data too.

Core CPI has been on a run-rate of around +0.4% for the past five months, so if this continues, then it would mean that YoY Core CPI would only drop to c. 5.2% in May and then c. 5.0% in June.

There is indeed more work to be done to be assured that inflation is moving towards the target of around 2%.

US CPI falls more than expected in April

Today’s US CPI data for April will have therefore come as something of a relief to the Fed but is not a game-changer by any means.

The headline CPI came in slightly lower than expected by the consensus, whilst core CPI was in line:

- US CPI increased by +0.4% MoM which meant YoY US CPI fell slightly to 4.9% (from 5.0% in March, 5.0% exp)

- US Core CPI increased by +0.4% MoM which kept YoY core CPI at 5.5% (5.5% in March, 5.5% exp)

According to the Bureau of Labor Statistics, shelter costs remain a crucial driver of inflation, however, the sharp increase in monthly costs of used cars and trucks also caught our eye.

The USD is underperforming, and Gold remains positive

Although the core PCE (Personal Consumption Expenditure) is the Fed’s preferred measure of inflation, the CPI readings are still the market-moving inflation data.

Inflation dropping a shade more than expected on the headline CPI leaves the Fed on the right track, but is not screaming out for any imminent allowance for rate cuts. That seems to be the root of the reaction in markets today.

Initial declines on US Treasury yields with some USD weakening. However, nothing has overly changed:

- The US 10-year yield has slipped slightly but remains around the middle of an 8-week band of 40 basis points between 3.25% and 3.65%.

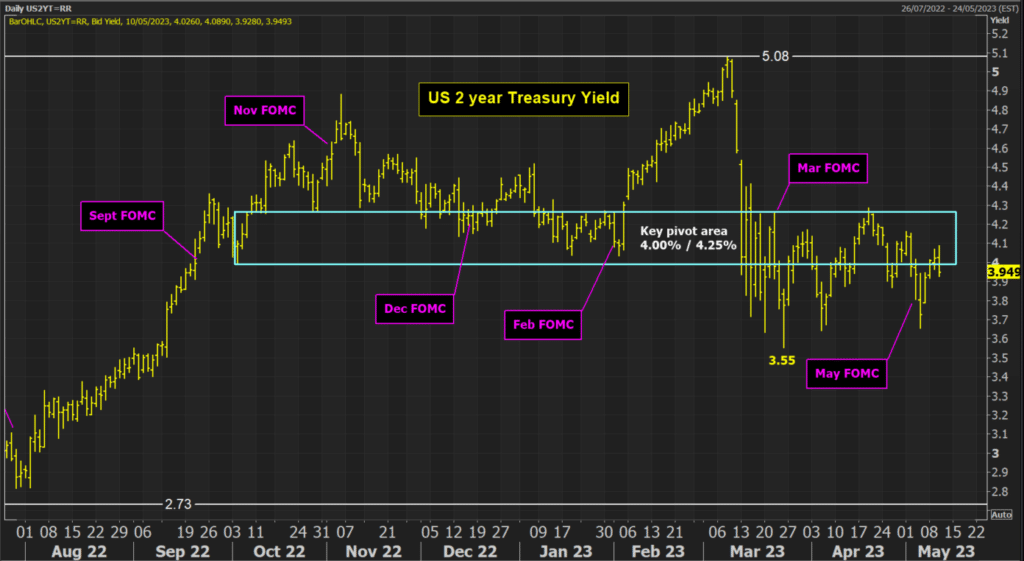

- The US 2-year yield is still more sensitive and volatile. It has dropped back under 4.00% once more unable to sustain a move into the 4.00%/4.25% area. It may now begin to track lower towards the 3.50%/3.75% area once more.

- The USD is tracking lower as a result of these lower yields. The key support on the Dollar Index remains at 100.78. If this is breached it would signal upside breaks on the likes of EUR/USD and GBP/USD.

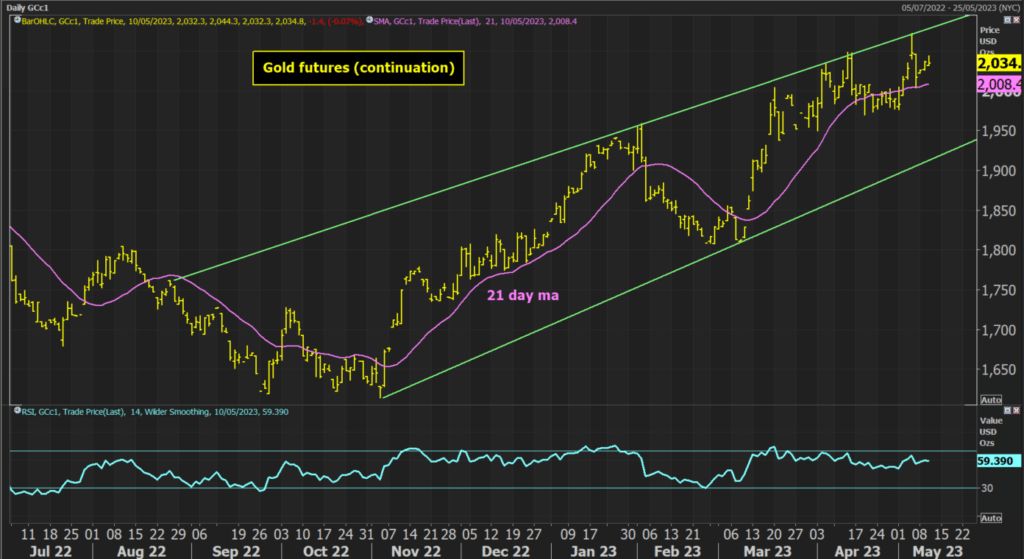

- Gold futures continue to trend higher. Having rebounded once more from $2004, the market is moving higher once more within the uptrend channel. A retest of the recent high at $2072 cannot be ruled out.