Macroeconomic/ geopolitical developments

- As expected, the Federal Open Market Committee (FOMC) increased rates on Wednesday by 0.75%, taking the benchmark Fed Funds rate to about 2.5%

- Powell highlighted a Fed Funds range of 3.0%-3.5% by year end, implying about 50-100 basis points of more tightening over the three meetings for the balance of this year, meaning the pace of rate hikes could slow.

- Markets and many market participants interpreted Fed Chair Jerome Powell’s post-meeting press conference as a dovish “pivot”.

- Quarterly earnings from Alphabet (GOOG) and Amazon (AMZN) were better than forecast, which produced a 4%, one day gain for the Nasdaq Composite.

- US gross domestic product (GDP) contracted by an annual rate of 0.9% in Q2, with consensus expectations for an increase of 0.5%.

- This softer data was taken as a “risk on” signal, reinforcing the view of a possible pivot to less hawkish, de facto more dovish, by the Fed.

Global financial market developments

- The major US stock averages were significantly higher last week, building on bullish technical signals from July, pushing again above notable resistance barriers from June and posting their best monthly gains since 2020.

- European and Asian equity indices were also very positive, reinforcing intermediate-term bottoming signals and in some instances again producing best monthly gains since 2020.

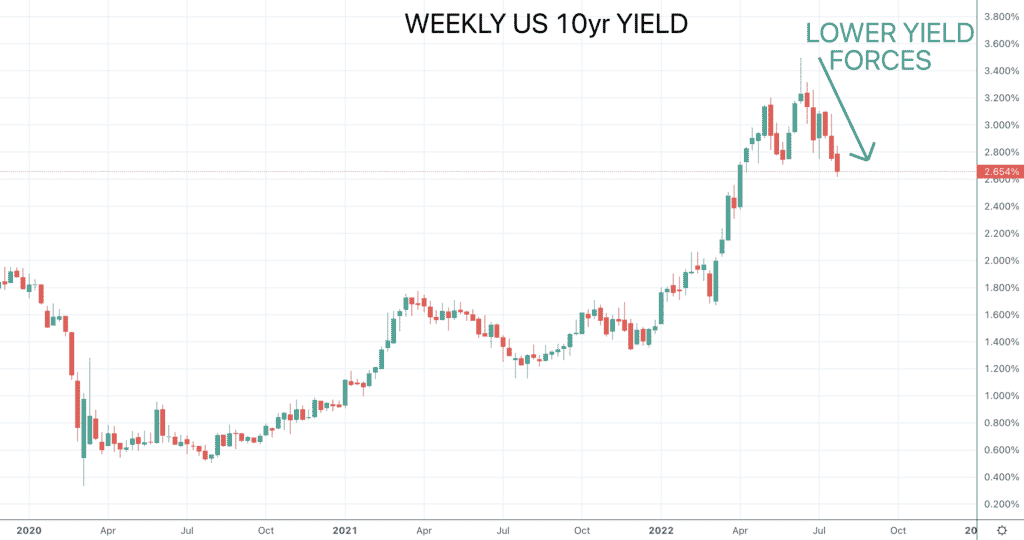

- US 10yr yields pushed even through the May yield lows, still encouraging lower yield pressures.

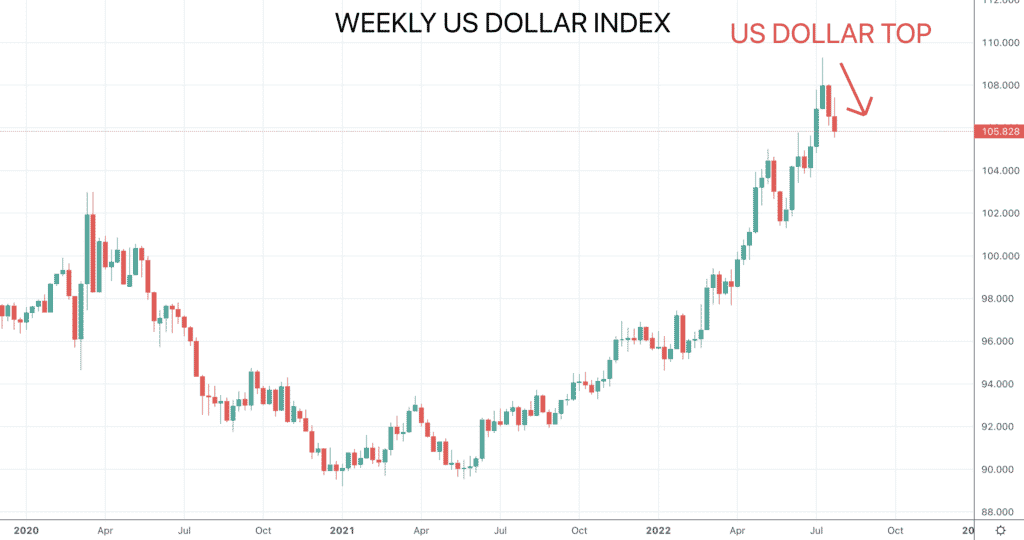

- The US Dollar Index sold off again, reinforcing the sell off from the mid-July multi-year high to reinforce signals a top, with risk staying lower.

- EURUSD consolidated the prior week’s rebounded for a developing base, aiming higher.

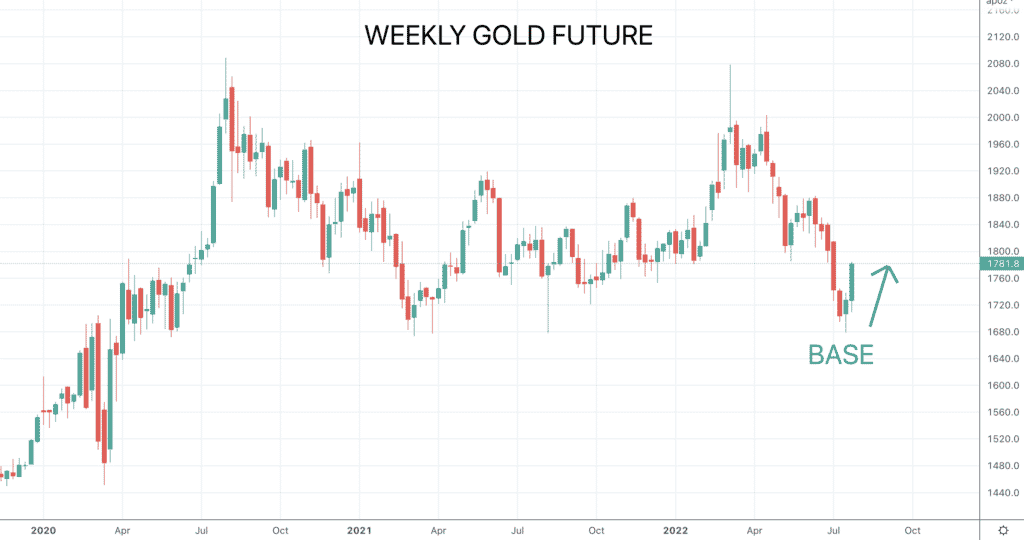

- Gold surged after the prior week’s bounce from 2021 supports, confirming a basing pattern and upside risks.

- Oil consolidated again, still unable to build on the rebound from mid-July, with bigger risks still skewed lower.

- Copper surged higher for to build on the previous cautious rebound effort, to shift positive.

Key this week

- Geopolitical focus: Still monitoring the war in Ukraine.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) interest rate decision, statement and press conference on Tuesday and the same from the Bank of England (BOE) on Thursday.

- Macroeconomic data: On the data front Monday brings global Manufacturing PMI from S&P Global and US ISM Manufacturing PMI, plus the equivalent Composite & Services PMI data on Thursday, plus the much-watched US Employment report is out on Friday.

| Date | Key Macroeconomic Events |

| 01/08/22 | German Retail Sales; global Manufacturing PMI from S&P Global; US ISM Manufacturing PMI |

| 02/08/22 | RBA interest rate decision, statement and press conference |

| 03/08/22 | Global Composite & Services PMI from S&P Global; US ISM Services PMI; EU Retail Sales |

| 04/08/22 | BOE interest rate decision, statement and press conference |

| 05/08/22 | US Employment report; Canadian Employment report |