Macroeconomic/ geopolitical developments

- An absence of any notable developments or contagion in the March mini banking crisis last week to end the month, as no new news was seen as good news, with fears of a more protracted or deeper financial meltdown easing.

- Banks stocks and the financial sector outperformed last week, rebounding after the prior week saw Deutsche Bank shares plunge and the entire banking credit and equity markets into a tailspin on Friday 24th, after a spike in Credit Default Swaps (CDS) in the German bank.

- Friday saw the release of the US Federal Reserve’s preferred inflation gauge, Personal Consumption Expenditure (PCE), with the core data for February still notably higher than the Fed’s long term inflation target, but below the consensus, posting at 4.6%, with expectations of 4.7%.

- Sunday saw OPEC+ unexpectedly announce production cuts of over 1 million barrels per day, outside of the group’s scheduled timetable, surprising markets (which saw Oil surge on Monday’s open)

Global financial market developments

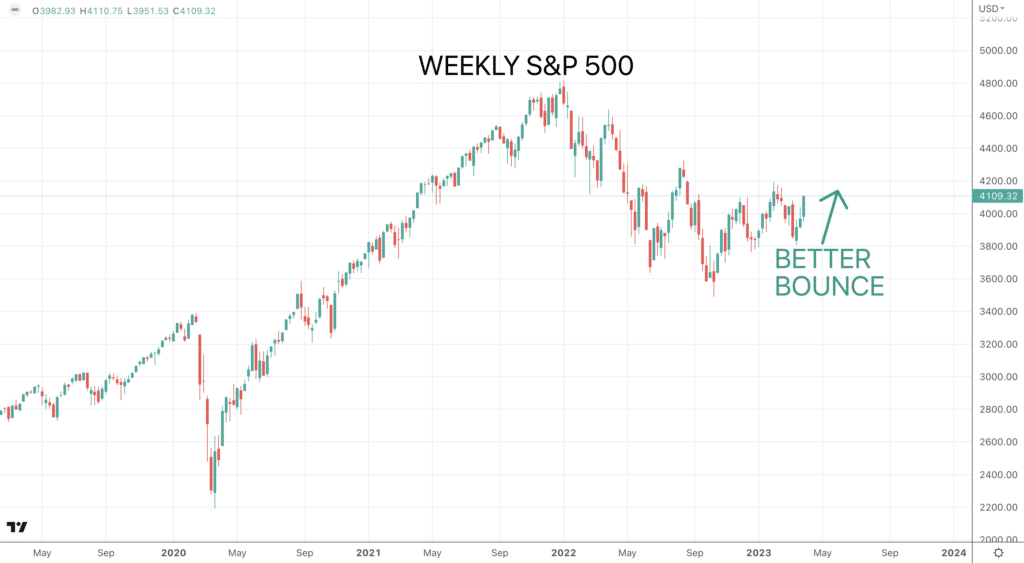

- The major US stock averages advanced further last week, as the turmoil in the banking sector eased with the Nasdaq leading the charge hitting a new 2023 high.

- European indices were also positive last week, reversing the notable losses to the banking sector the prior Friday.

- US and European Bond paused and corrected slightly to higher yields after they had surged to higher prices and lower yields in the wake of banking crisis fears, with the US and German 10yr yields bouncing from multi month yield lows.

- Forex markets were quiet with the US Dollar weakening slightly.

- Gold marked time last week, consolidating the prior push higher to a 2023 and multi-month high, as the ultimate safe haven!

- Oil prices surged on Monday after the aforementioned announcement of supply cuts by OPEC+, with the price leaping over 8% having pushed to a 2023 and multi-month low in March, now back close to a multi-month high.

Key this week

- Geopolitical events: Good Friday holiday on 10th April, UK, European and US bond and stock markets are closed.

- Central Bank Watch: Tuesday sees the Reserve Bank of Australia (RBA) interest rate decision and statement, and we get the same from the Reserve Bank of New Zealand (RBNZ) on Wednesday. From the Fed, Governor Cook speaks Monday and Tuesday, but no other speakers scheduled this week.

- Macroeconomic data: A busy data week, with S&P Global Manufacturing PMI and US ISM PM on Monday and the equivalent for Services released on Wednesday, and despite the Good Friday holiday, US employment data is released Friday.

| Date | Key Macroeconomic Events |

| 03/04/23 | S&P Global Manufacturing PMI (global): US ISM PMI; Fed Governor Cook speaks |

| 04/04/23 | RBA interest rate decision and statement; Fed Governor Cook speaks |

| 05/04/23 | S&P Global Services PMI (global): US ISM PMI; US ADP Employment change |

| 06/04/23 | Canada Employment report |

| 07/04/23 | Good Friday holiday, UK, European and US bond and stock markets are closed; US Employment report |