On 22nd September 2022, with the USD/JPY pair having risen above 145, the Bank of Japan felt that enough was enough. The Japanese yen had weakened to such an extent that the BoJ felt compelled to intervene in the forex markets (by selling USD) for the first time in 24 years. Over the next few weeks, the BoJ intervened several times to try and prop up the ailing yen. Now, with the Japanese yen weakness (and USD strength) once more pulling USD/JPY above 145, will this induce another bout of intervention? The time may be close, but intervention is not a given.

- Intervention in September/October 2022 worked, for a while

- Rising US yields drive persistent JPY weakness, but volatility is relatively low

- Could safe haven flows help the BoJ?

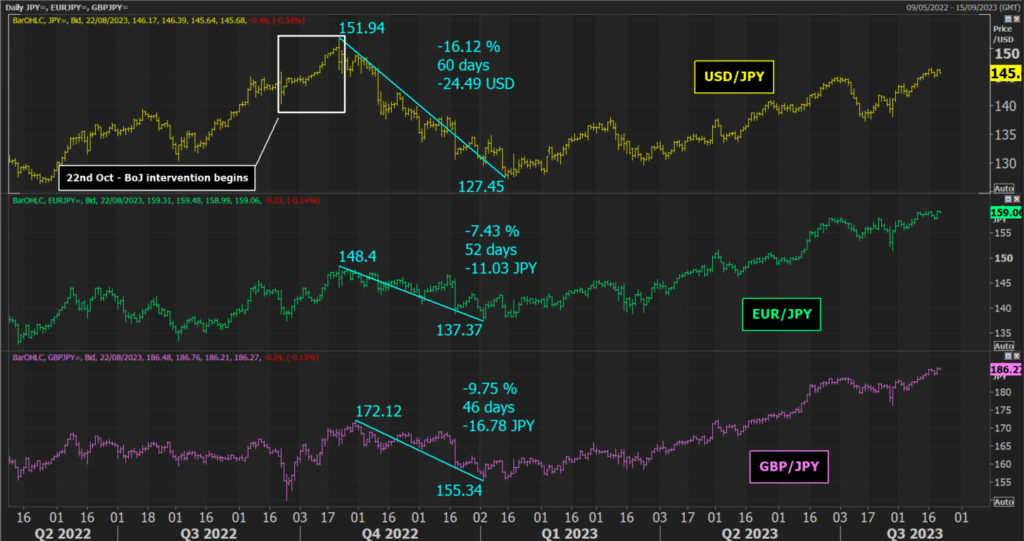

BoJ intervention of September/October 2022

According to daily intervention records (released on a quarterly basis), the Bank of Japan’s (BoJ) intervention in forex markets started on 22nd September before further moves on the 21st and 24th October. On those three occasions, the BoJ spent around 9.19 trillion yen, with the total intervention estimated to be around $68bn.

The moves began with the pair edging above 145 in late September. However, the largest intervention came on 21st October which coincided with the USD/JPY peaking at 151.94. The move certainly seemed to work, at least for a while. The pair then spent the next 60 days in retreat, with a decline of over -16%.

However, as is so often the case with currency interventions, any improvements tend to be short-lived (the most classic case being George Soros, the GBP and Black Wednesday). Once more over recent months, the yen has been weakening. It would seem that buying around $68bn worth of yen does little when interest rate differentials are so wide.

As the USD/JPY pair rallied towards 145 in late June, I wrote about how weakness in the Japanese yen impacted the prospects of another BoJ intervention. The pair backed off for a few weeks but has now rallied once more. The USD/JPY pair is now above 145 again. This has come as the yield on the US 10-year Treasury has soared back to the levels seen in October (c. 4.33%).

According to CEIC Data, the Bank of Japan is sitting on around $1.13 trillion of foreign reserves (as of July). Spending similar amounts again would cost it around 6% of its forex reserves. But does this mean that the BoJ will intervene again? The conditions are slightly different this time around.

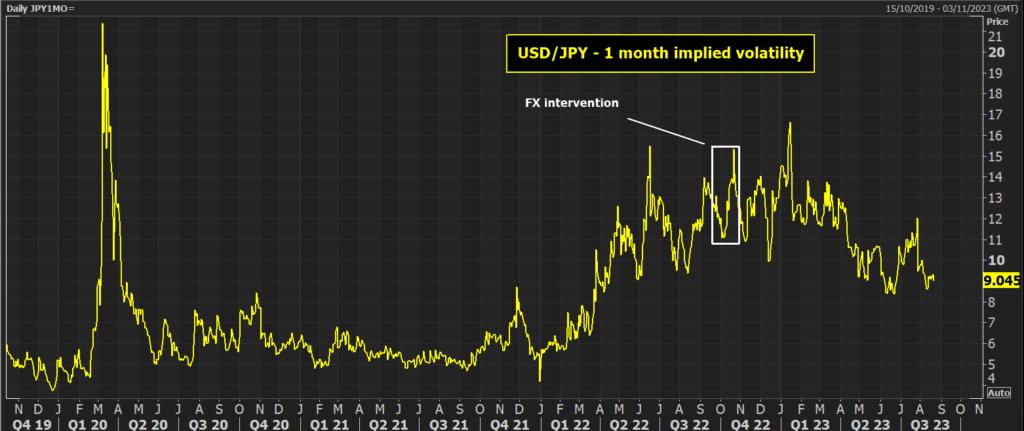

Volatility is lower this time around

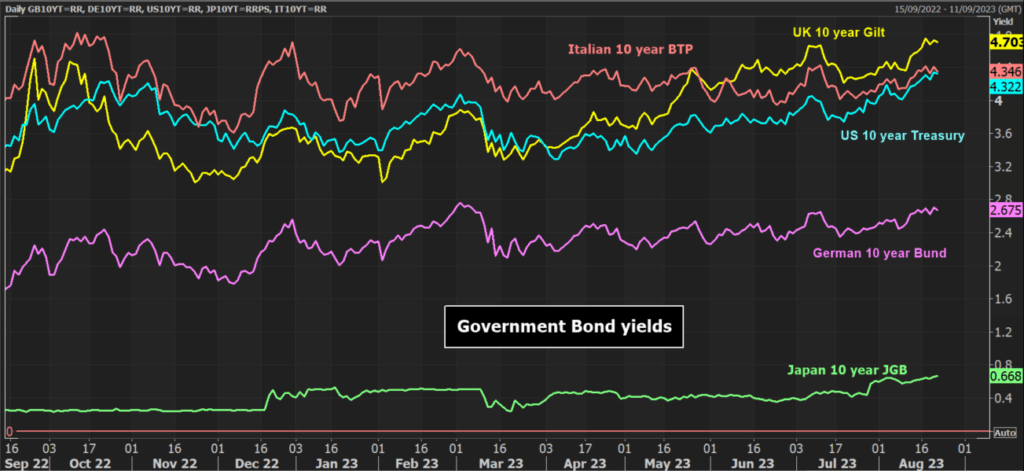

The higher level of JGB rates may have a part to play in reducing the prospect of immediate intervention. The 10-year JGB is at 0.668% today, helped higher in recent weeks by the surprise move from the BoJ to allow a wider band on the 10-year yield.

Volatility for USD/JPY is now much lower than it was in October. The chart of the 1-month implied volatility is trading around 15-month lows currently. This helps to keep an orderly market.

The Japanese yen remains one of the weakest performing of the major currencies. But could this begin to turn around? Might the Bank of Japan be looking at current market conditions? There is a more risk-averse market sentiment forming. This could induce a natural flow into the safe haven yen in the coming weeks.

The performance of the US economy and how hawkish the Federal Reserve tends to be will likely have a big role in defining how much stronger the USD becomes and subsequently, how high the USD/JPY goes. The US economy is proving to be stronger than most had expected and this is likely to encourage a more hawkish positioning from the Fed. Fed Chair Powell’s speech at Jackson Hole will make for interesting reading.

So perhaps the moves above 145 are a warning sign, but given the current market conditions, perhaps the BoJ will hold off just for now. However, moves towards 150 will likely begin to make the BoJ sweat again.

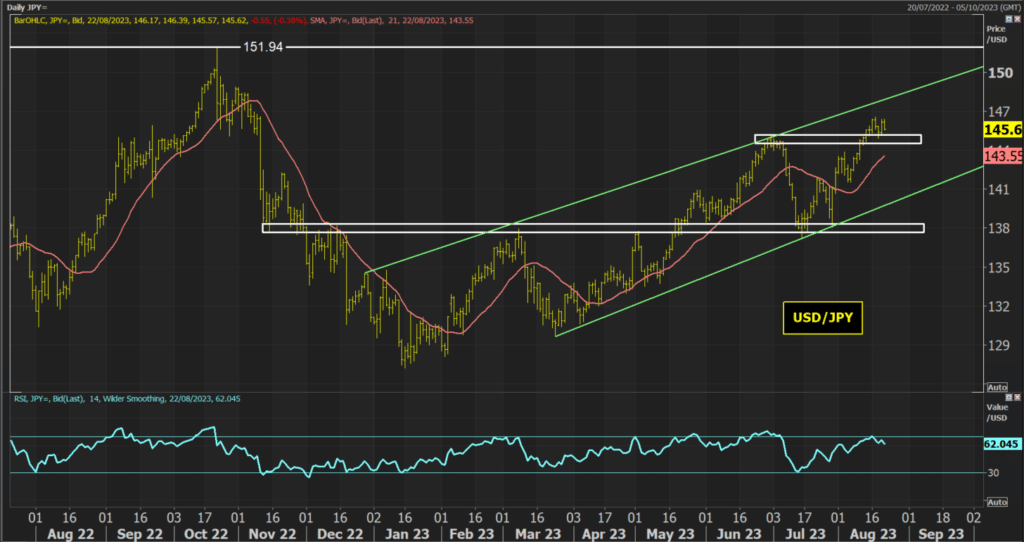

Technicals show the path higher

Looking at the technical analysis of USD/JPY, we see a pair now in a decisive uptrend channel. The breakout above the June high of 145.07 is now an initial basis of support, with a pullback having already tested the support. However, there is toom to run higher within the channel. It has the look of a chart to buy into weakness. The rising 21-day moving average is consistently a good gauge for the support of near-term corrective moves. The initial resistance is the recent high at 146.56 but above there, the way is once more open towards the key October high at 151.94.