GBP has been one of the standout performers on major forex for several months. The move has been driven by continued high inflation and eyewatering expectations of Bank of England rate hike expectations. However, the CPI inflation data for June has come in below expectations and markets are reacting. This could now trigger a re-assessment of further rate hikes and begin to weigh on GBP performance.

- UK CPI finally drops back in June

- UK Gilt yields and interest rate expectations retreat

- GBP is starting to retrace outperformance

- There are key levels to watch on on GBP crosses

UK inflation finally falls

UK inflation is finally falling. The headline CPI data peaked several months ago at around 11% and has retreated to 7.9%, but this was largely due to external factors (the decline in fuel costs mostly). However, crucially, there are signs now that finally, core CPI may also be starting to track lower. After months of upside surprises and stubbornly high inflation readings, the data has surprised to the downside. This is very welcome news for the Bank of England which has been spectacularly struggling to control inflation.

- UK CPI dropped to 7.9% from 8.7% in May, lower than the 8.2% consensus forecast.

- UK Core CPI dropped to 6.9% from 7.1% in May, where expectations had been for it to remain at 7.1%.

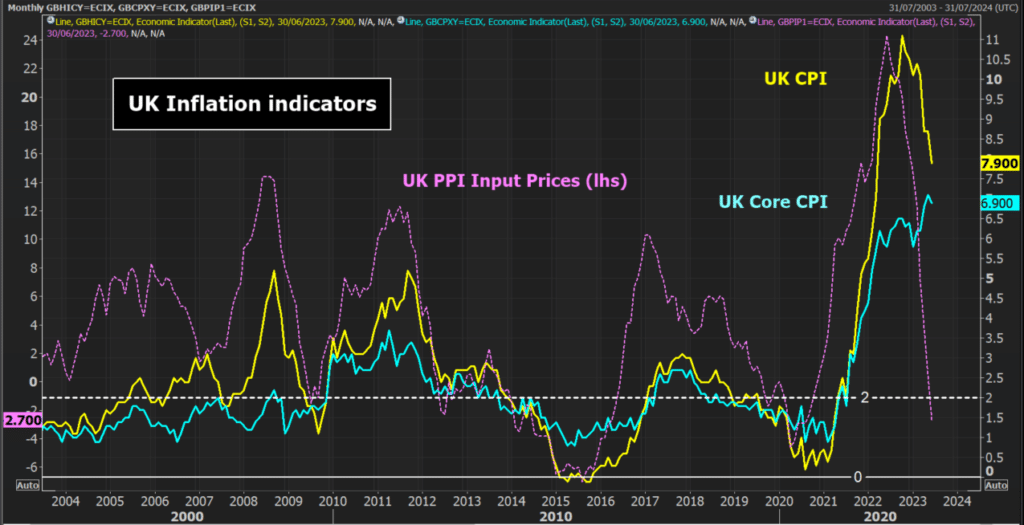

The chart below shows the decline in the CPI. However, it also shows (on the left-hand scale due to its much larger spikes) the sharp reduction in the UK PPI (input prices), which is now -2.7% year on year.

The chart shows that CPI prices tend to follow the PPI lower, with a lag of a few months. The headline CPI reacted with a peak around four months after the PPI. However, the Core CPI has been far more stubborn, moving counter to the PPI move. Although one month does not make a trend, perhaps this will now begin to also track lower.

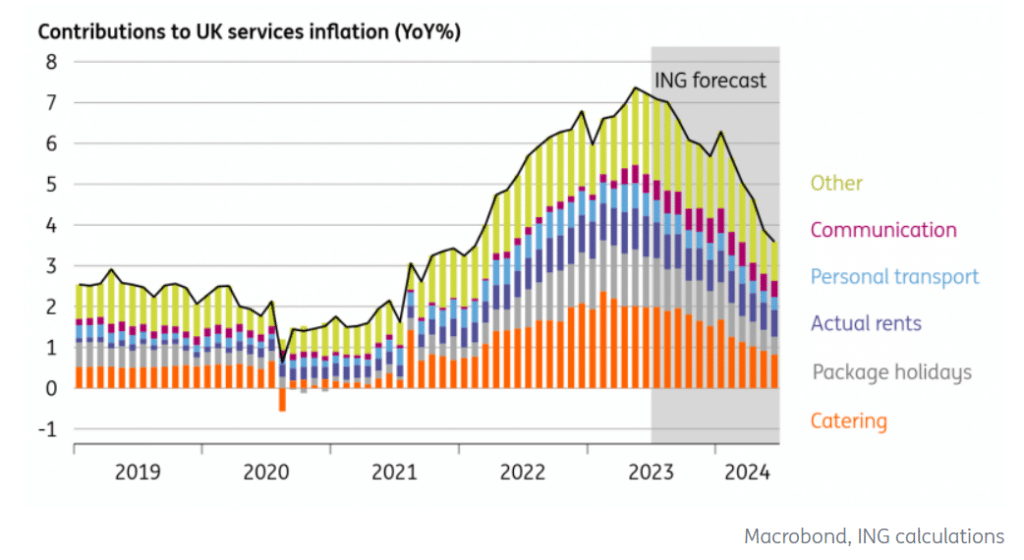

One of the key factors in keeping inflation so high has been the contribution of services inflation with the high price of food in the UK. Food price inflation seems to now appear to have peaked, falling to 17.4% in June from 18.4% in May (and below the 19.2% March 2023 peak). The continued reduction in the UK PPI should help to further reduce food price inflation in the months to come.

The Bank of England gives significant focus to the direction of services inflation. Services inflation was forecast by the BoE to remain at 7.4% in June but reduced to 7.2%. This will certainly be welcome news for the Monetary Policy Committee. According to ING forecasts, services inflation has now peaked and will start to unwind decisively in the coming months.

Falling inflation, falling yields and tempering BoE expectations

Given its woeful attempts at controlling inflation in the UK, it may come as a significant surprise that the Bank of England correctly predicted in May that inflation would fall to 7.9% in June. However, that is pretty much the only thing that it has got right recently (forecasting a 15-month recession last year immediately springs to mind…).

Despite this, the expectation will now be that inflation will continue to fall in the months ahead. ING is suggesting 6.6% on both headline and core CPI for July.

Markets are reacting to this. Last month there had been an explosion in Gilt yields and rate hike expectations for the Bank of England. Gilt yields are now coming back decisively. Yields have opened around -25 basis points below yesterday’s close on the 2-year Gilt.

The SONIA rate (UK interest rate futures) which is effectively the market expectation of peak rates, was looking at over 6.50% a couple of weeks ago. However, this has tempered slightly and a peak rate of 6.00% is more likely now. It will be interesting to see if this continues to reduce.

The Bank of England’s Base Rate is currently 5.00%. Inflation has been far more stubborn to reduce than in many other countries (the lack of transmission has been a problem). However, if this is the case, then rates at 6.00% still seems fairly high. What this inflation data does is gives the BoE a decision to make over 25bps or 50bps in its August meeting. There are arguments now for both.

Time for a GBP unwind?

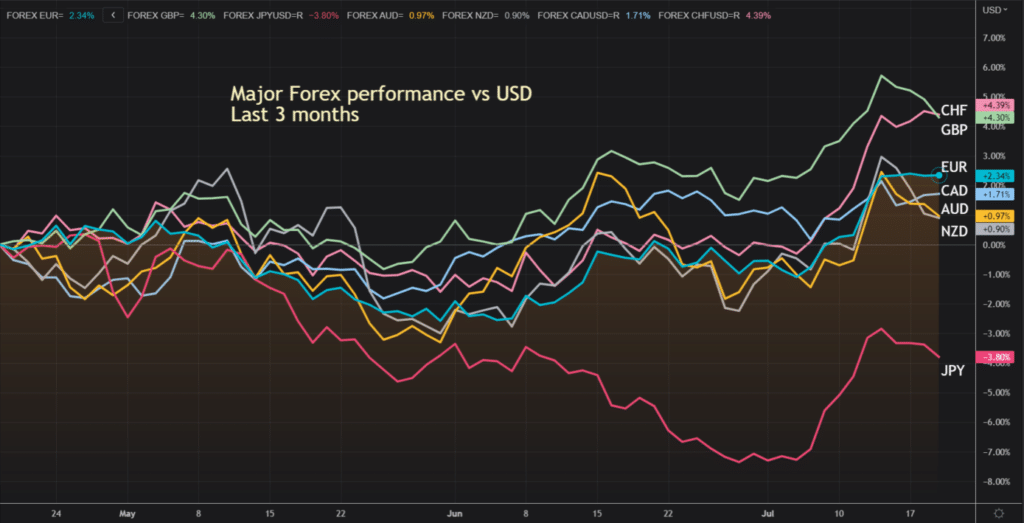

The market impact on GBP has been significant today, with decisive underperformance taking hold. This move is a retracement to the consistent outperformance that GBP has had in recent months. The chart below shows GBP has been the strongest major currency in that time.

However, there is plenty of room therefore for this move to unwind. If the market takes a view that these huge expectations of Bank of England interest rates have been overblown, then GBP could begin to struggle, at least near term versus majors such as the EUR, CHF and CAD.

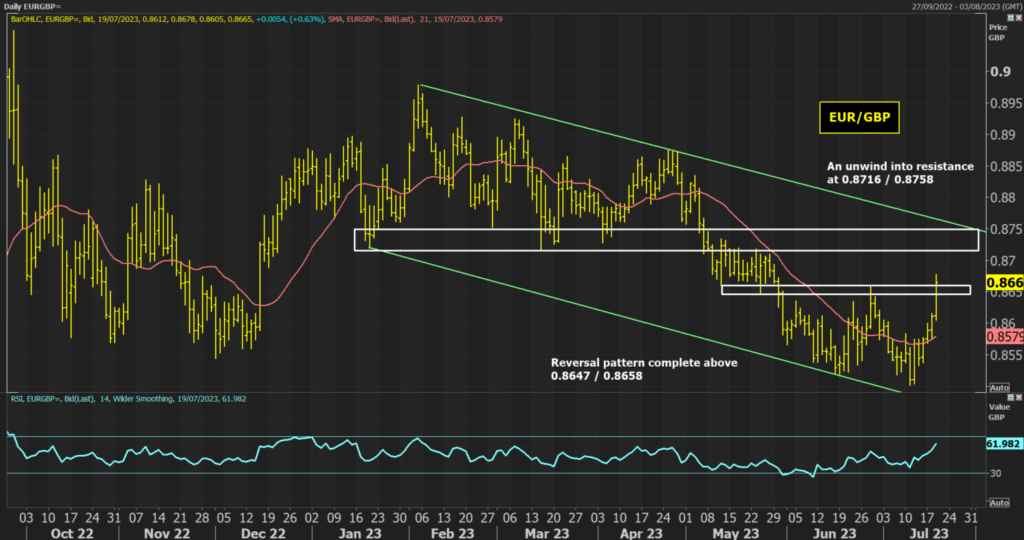

Key levels to watch on EUR/GBP

There is room now for a GBP unwind. I looked at a potential retracement on GBP/USD yesterday from the point of view of a USD oversold rally. There could be a retreat on Cable back into 1.2680/1.2848.

However, I see EUR/GBP as having turned an important corner, at least near term. The pair has been channelling lower throughout 2023, but the GBP weakness today looks to be completing a reversal pattern above 0.8658. If seen on a closing basis it would open a rally towards at least a test of the key resistance between 0.8716/0.8758. This is also the top of the downtrend channel. RSI momentum is positive above 60 to suggest that momentum is with the recovery now. Near-term supported weakness that holds above 0.8612 would be a chance to buy for this recovery.