Macroeconomic/ geopolitical developments

- US debt ceiling concerns are rising, Treasury Secretary Janet Yellen commented last week that a US default would be an “economic and financial catastrophe”.

- US CPI headline inflation fell more than expected to 4.9% on Wednesday, whilst core inflation dipped slightly but was in line with expectations at 5.5%.

- Inflation continues to plunge in China, the PPI (factory-gate inflation) accelerated down to -3.6%, with headline CPI at +0.1%, the lowest since early 2021.

- The Bank of England (BoE) joined the Reserve Bank of Australia (RBA), the Fed and the European Central Bank (ECB) hiking by 0.25% on Thursday as widely expected.

- UK interest rate swaps markets are pricing possibly two more 25bps hikes to bring the rate 5.00%, then pausing later in the summer.

Global financial market developments

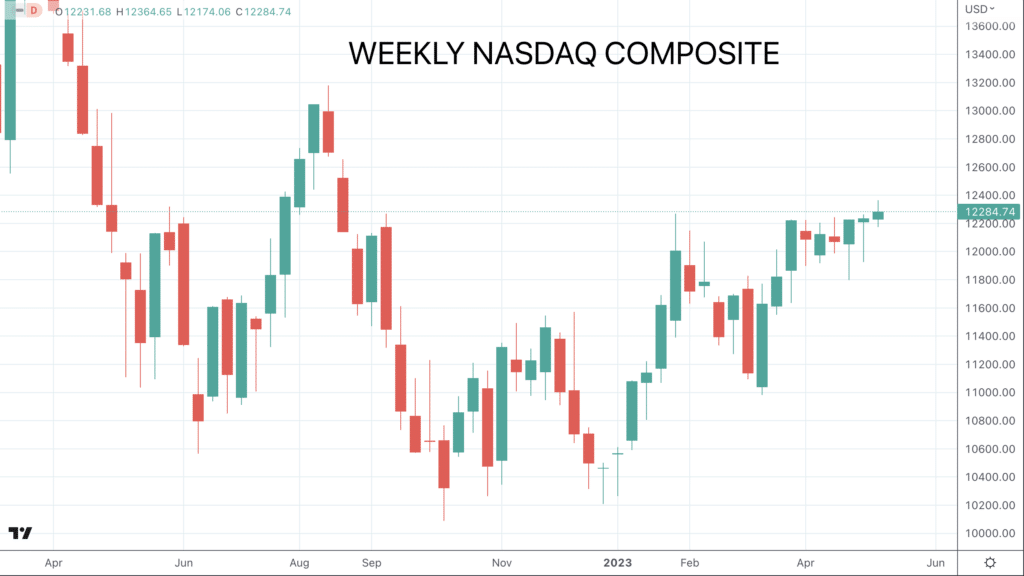

- The major US stock averages were mixed, with a plunge through last week, then a firm rebound Friday, retaining intermediate-term the DJIA lower, the S&P little changed on the week, whilst the Nasdaq hit a multi-month high.

- European indices consolidated, near to recently set multi-month highs.

- US and European Bond yields were in consolidation mode but retain a lower yield bias.

- The US Dollar Index rebounded from near a multi-month low, switching to a more positive tone.

- Gold consolidated below a recently set multi-month high.

- The early may Oil rebound from a multi-week low faltered back lower last week.

Key this week

- Central Bank Watch: Fed speakers in focus, with no significant central back activity in the coming week.

- Macroeconomic data: A quiet data week, UK Unemployment, German ZEW and US Retail Sales are probably the standouts, all released on Tuesday.

| Date | Key Macroeconomic Events |

| 15/05/2023 | Eurozone Industrial Production |

| 16/05/2023 | Chinese Industrial Production & Retail Sales; UK Unemployment; Eurozone Trade Balance; Eurozone GDP (2nd); German ZEW Economic Sentiment; Canadian Inflation; US Retail Sales & Industrial Production |

| 17/05/2023 | Japanese GDP (Q1 prelim) & Industrial Production; Eurozone HICP Inflation (final); US Building Permits & Housing Starts |

| 18/05/2023 | Australian Unemployment, US Weekly Jobless Claims, Philly Fed Manufacturing; US Existing Home Sales |

| 19/05/2023 | Japanese inflation |