Macroeconomic/ geopolitical developments

- On the data front, Monday saw the release of the US ISM Manufacturing PMI activity data, which was below expectations, and also showed falling price pressures (fuelling a risk on theme to start the week, month and quarter).

- Further easing inflation fears and adding to the risk on tone, the US job openings (JOLT) data for August fell to its lowest level in more than a year and by the most in nearly 2.5 years, by more than expected.

- The Reserve Bank of Australia (RBA) interest rate decision and statement on Tuesday brought a less than expected 0.25% rate hike (consensus was for 0.5%), which assisted in a “risk on” rally across global asset classes.

- This “pivot” by the RBA sparked market hopes of similar pivots by other central banks globally, and most notably, potentially by the Fed.

- However, US Federal Reserve speakers remained extremely hawkish in comments throughout last week, in the face of the pivot chatter.

- On Wednesday the OPEC+ group of oil exporters announced a 2 million barrels per day cut in target production, at the upper end of market expectations (sending the oil price higher and raising inflation fears).

- The US Employment report on Friday saw 263K jobs added last month, close to expectations, whilst the unemployment rate fell to match a five-decade low at 3.5%.

- This data release saw markets react with risk off moves across financial assets.

Global financial market developments

- The major US stock averages posted modest gains last week, though gave up much of the early weekly gains

- The S&P 500 added 5.6% in the first two sessions of October, posting its best two-day advance since 2020 and the third-best start to an October since 1930!

- Subsequent losses from Wednesday, however, saw much of these gains surrendered.

- European and Asian equity indices also posted weekly gains.

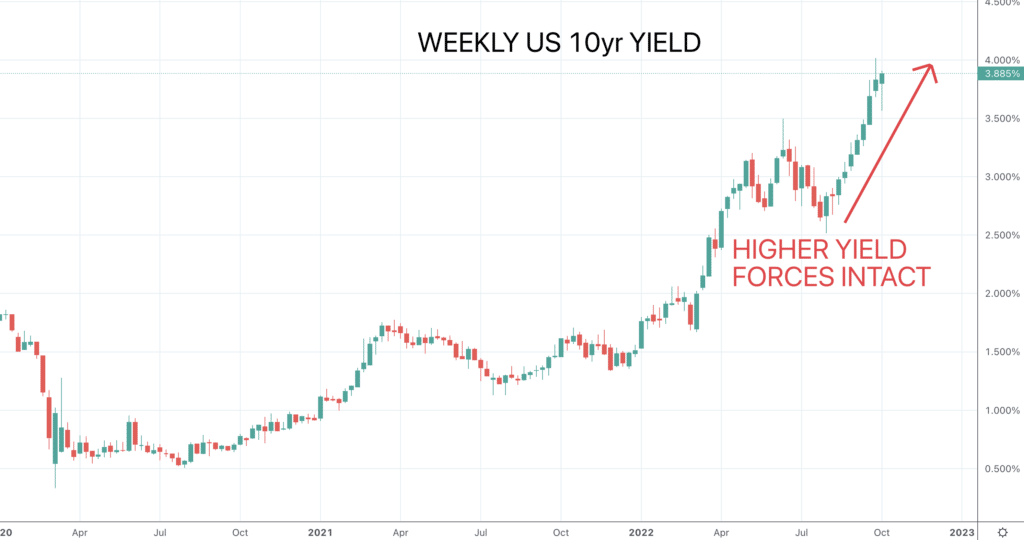

- US 10yr yields were lower then back higher, but closed at a higher yield for the week.

- US Dollar weakened the strengthened again, as DXY closed at a new multi-decade peak.

- GBPUSD advanced then failed lower after the prior week’s plunge and rebound from a record low.

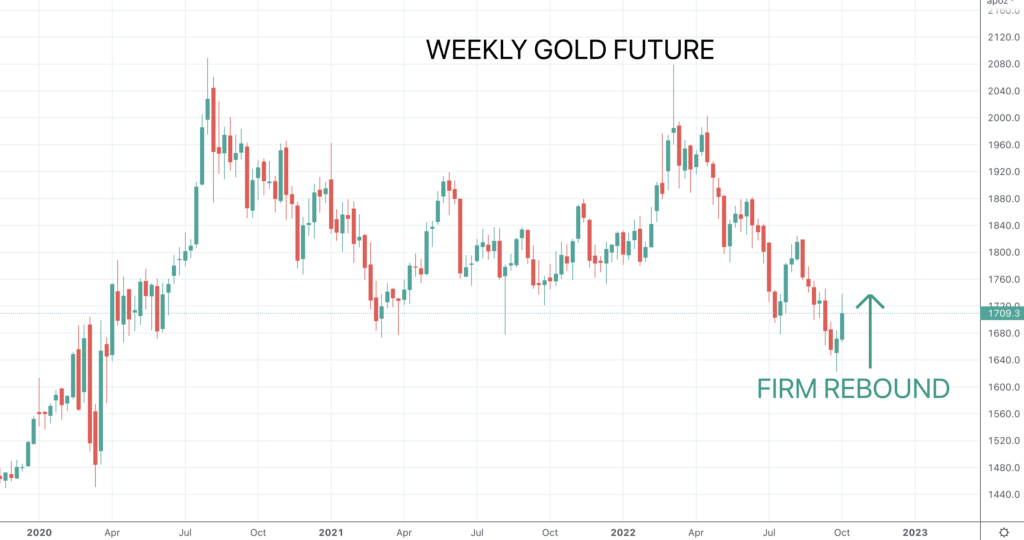

- Gold rebounded further after hitting a multi-month low at the end of September.

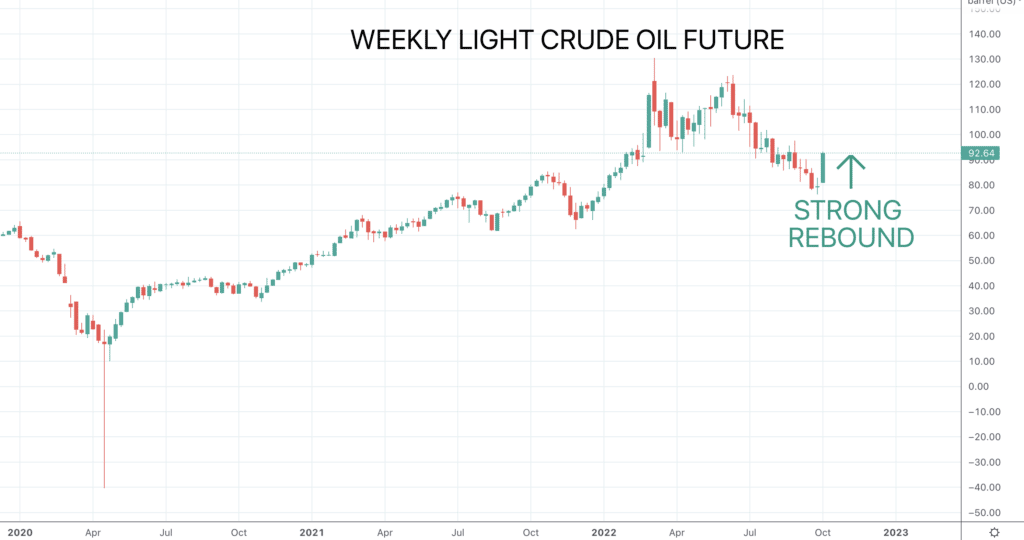

- Oil surged before and then in the wake of the OPEC+ production cut decision, having hit a multi-month low at the end of September.

- Copper rallied and then sold off, retaining a bear tone.

Key this week

- Central Bank Watch: We get the FOMC Minutes on Wednesday.

- Macroeconomic data: Key data comes Thursday with the release of US CPI.

| Date | Key Macroeconomic Events |

| 10/10/22 | Columbus Day holiday, US Bond markets closed |

| 11/10/22 | UK Employment report |

| 12/10/22 | UK GDP, Manufacturing and Industrial Production; US PPI; FOMC Minutes released |

| 13/10/22 | German CPI; US CPI |

| 14/10/22 | China CPI; US Retail Sales |