Equity markets had a strong run higher in March and April. However, moving into May the rallies are looking tired. Macro factors are starting to weigh on sentiment ahead of crucial monetary policy announcements from the Federal Reserve and the European Central Bank. Sentiment is threatening to sour and this could mean a period of profit-taking is approaching.

- The US banking crisis claims another victim

- Yellen’s debt ceiling warning

- An increase in volatility on equity markets

- A bull failure posted on E-Mini S&P 500 futures

The US banking crisis claims a third failure

Over the weekend, First Republic Bank, a mid-tier bank in the US became the latest victim of a banking crisis that has threatened to take hold of the US economy. It is the third bank to fail in the US (after Silicon Valley and Signature) and is the largest bank to fail since 2008.

With JP Morgan Chase picking up the assets of First Republic, this helps to stabilise the immediate concerns, but there will be a legacy of the failure. Is it just putting a thumb in the wall of the dam only to spring another leak elsewhere?

That is what traders will continue to ask themselves in the weeks ahead.

A warning from Janet Yellen on the US debt ceiling

The argument over the raising of the US debt ceiling continues to rumble on.

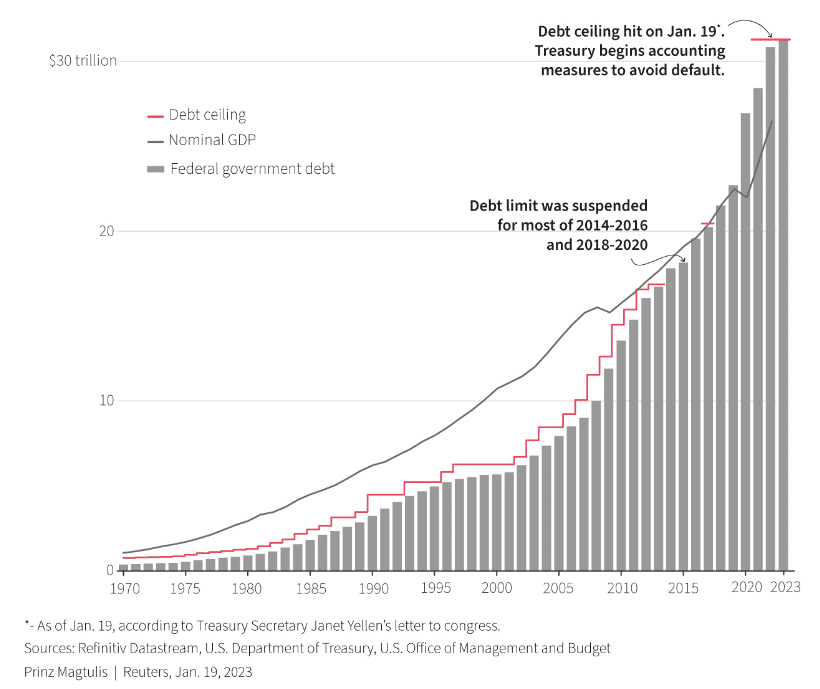

The debt ceiling of $31.4 trillion was reached on 19th January. Ever since, the US Treasury has been engaging in a series of cash management measures to keep up with payments on its debt, benefits and obligations.

However, time is running out ahead of what would be an unprecedented default on its debt. The issue was brought into focus for traders on Monday after Janet Yellen, the Treasury Secretary (and former Fed Chair) claimed in a letter to Congress that the US Government would run out of road on its spending “potentially as early as the 1st June”.

Here’s a great graphic from Refinitiv showing the level of the US Government debt, the debt ceiling and nominal GDP.

This may be a little bit of political brinkmanship, as Yellen also noted that:

“It is impossible to predict with certainty the exact date when Treasury will be unable to pay the government’s bills”

If the Government can fudge through June, there are a few A bipartisan agreement is a long way off in Congress, so the longer this one goes, the more prescient markets will become. Nerves will fray, and market fears will rise.

That means volatility will begin to increase once more.

Volatility on equities is starting to increase again

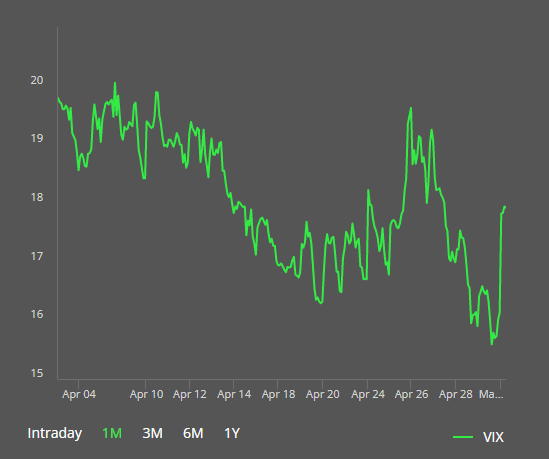

We have seen the rumblings of increased volatility in recent sessions.

Despite mounting concerns over a US recession, it seems as though markets had reached levels of near complacency in recent weeks. On Monday, the VIX Index of S&P 500 options volatility had fallen to 15.7 which was the lowest level since November 2021.

However, could there now be a shift in the gauge? A mini spike up to 17.9 today might not sound a lot but it is up 14% from the low and could be the start of something.

Here is the VIX Index from the CBOE.

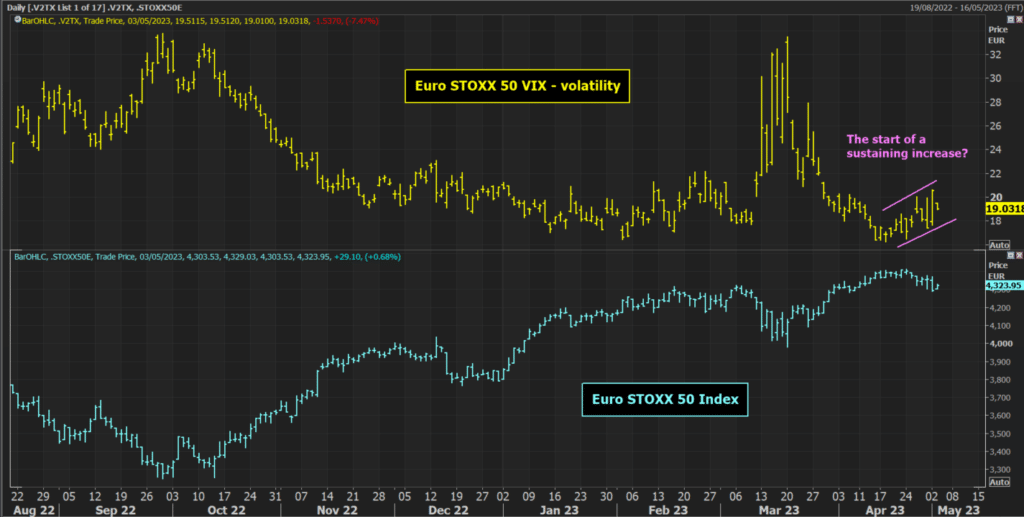

The situation is not restricted to the US either. In European indices, the VIX volatility gauges are also starting to trend higher.

This chart of the VIX on the Euro STOXX 50 (an index of the 50 largest European stocks) shows volatility is trending higher.

There is a clear negative correlation between volatility and stocks. If volatility continues to increase, then we can expect that European equities will fall.

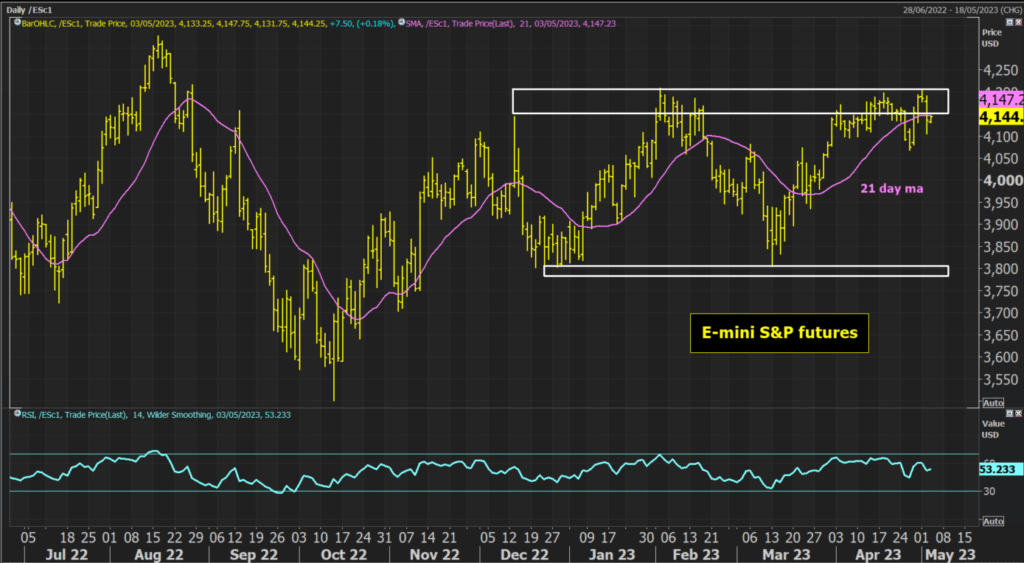

A bull failure on E-Mini S&P 500 futures

Back onto the US stocks, looking at the technical analysis of the E-Mini S&P 500 futures, we see that the sharp move lower yesterday is once more the futures posting a bull failure around key resistance.

The rally that was seen throughout March and into April seems to be running out of steam. The daily RSI momentum has already been tailing off recently. Also, yesterday’s decisive decline into the close should serve as a warning. It seems as though there is little upside potential around the highs of a trading range of the past five months. The reaction to support initially at 4105 but more importantly at 4069 will be a key gauge in the coming days.

Traders will obviously give great importance to the Fed meeting announcement later today (but also the ECB meeting tomorrow). It will be an intriguing market reaction. Any sense that the Fed’s rate tightening is coming to an end should send US equities higher. However, if there is another bull failure under the resistance at 4208 this will add to the feeling that this rally is on its last legs.

Furthermore, there are the Apple results after the closing bell on Thursday too. It could be an important few days ahead for equities and stock markets.