There has been a re-emergence of a banking crisis in 2023. Suddenly, traders are looking out for key indicators of stress in the banking system. This has brought credit default swaps back into focus. This is enough to put the shudders down the spine of even the hardiest of traders.

Credit Default Swaps (or CDS for short) came to mainstream prominence during the Great Financial Crisis of the late 2000s. Fast forward more than a decade later and with the strains being felt in US and European banking, CDS are making an unwelcome return to the headlines.

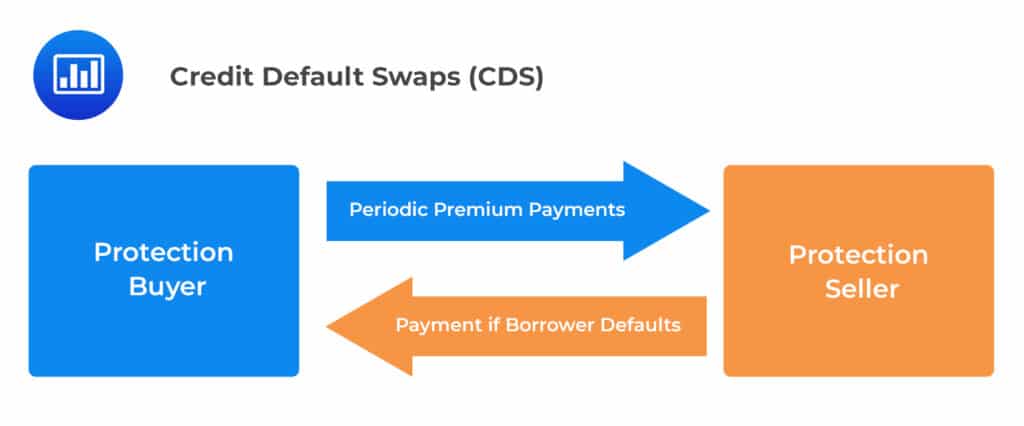

What are credit default swaps

Credit Default Swaps (CDS) are financial derivatives that provide investors with protection against the risk of default by a borrower. The basic structure of a CDS involves two parties: the protection buyer, who purchases protection against a default event, and the protection seller, who receives periodic payments in exchange for assuming the risk of default.

They are designed for protection against a credit event, such as default or bankruptcy, of a specific underlying reference entity, such as a corporation or a sovereign government.

The protection buyer agrees to pay a regular premium to the protection seller for a set period, typically five years. In exchange, the protection seller agrees to pay a predetermined amount to the protection buyer if a default event occurs during the life of the contract. The amount of the payout is typically equal to the face value of the underlying debt instrument, such as a bond.

CDS contracts are often used as a form of hedging or speculation by investors who want to protect against potential credit losses or profit from changes in credit risk. The price of a CDS contract reflects the perceived creditworthiness of the reference entity and is influenced by factors such as market sentiment, economic conditions, and the credit rating of the reference entity.

CDS are often used by investors to hedge against the risk of default in their investment portfolios. For example, an investor who holds a large portfolio of corporate bonds may purchase CDS protection on those bonds to reduce the risk of default. If a default event occurs, the investor can collect the payout from the protection seller to offset the losses from the default.

CDS can also be used for speculative purposes, as investors can purchase protection on debt instruments they do not own. In this case, the investor hopes to profit if the issuer defaults and the payout from the CDS exceed the cost of the premium paid to the protection seller.

CDS contracts have been the subject of controversy and criticism due to their role in the 2008 financial crisis and their potential to create systemic risks in financial markets. However, they continue to be widely used in the financial industry as a tool for managing credit risk.

Overall, CDS provide a means for investors to manage credit risk.

The history of why credit default swaps influence markets

The history of credit default swaps in banking can be traced back to the late 1990s.

In 1994, J.P. Morgan introduced the first credit derivative, which was a type of swap designed to transfer the credit risk of a portfolio of loans from one party to another. However, it wasn’t until 1997 that the first credit default swap was created. This was done by Blythe Masters, a young J.P. Morgan banker who led the team that developed the CDS product.

The early days of credit default swaps were marked by relatively low volumes and limited use. However, as the technology and infrastructure for trading these instruments developed, CDS became increasingly popular among investors looking to hedge their credit risk exposure.

During the early 2000s, credit default swaps became a key tool for banks and other financial institutions to manage their credit risk exposures. These instruments were particularly useful for banks, as they allowed them to transfer the risk of a borrower defaulting on their debt to other parties, thereby reducing their own risk exposure.

Why are CDS so emotive for financial markets?

However, the widespread use of credit default swaps also contributed to the 2008 financial crisis. Many banks and other financial institutions had used CDS to hedge against mortgage-backed securities and other risky assets. But when the housing market collapsed, these institutions found themselves with massive losses that they were unable to cover.

Furthermore, rising CDS prices increased the pressure on already embattled banks. They helped to create a negative spiral of selling pressure on financial institutions bringing increased focus and exacerbating market pressures.

In the aftermath of the financial crisis, there were calls for greater regulation of credit default swaps and other complex financial instruments. Today, credit default swaps remain an important tool for managing credit risk, but they are subject to greater regulatory oversight and more rigorous risk management standards than in the past.

Growing pressure on European banks in 2023

The demise and subsequently forced takeover of Credit Suisse by Swiss banking rival UBS brought a US banking crisis squarely to Europe’s door in March 2023. The chatter amongst traders quickly then turned to, “well who’s next?”.

Deutsche Bank has long been kept under a watchful eye, as a potential black sheep of the European banking family. Despite a series of restructurings, divestments and management changes have struggled to shake off concerns over the longevity of the business.

CDS concerns hit Deutsche Bank and the whole banking sector

Those concerns blew up less than a week after the announcement of the Credit Suisse takeover. Deutsche Bank’s CDS had already been climbing sharply, but on Friday 24th March the accelerated to above 220 basis points. This was up from 142 basis points just two days prior and was the highest level for more than four years. Although this was still below the levels hit during the Eurozone debt crisis in 2011 (close to 300 basis points), this was still a significant enough move to scare markets.

Even if Deutsche Bank is not about to go bust, moves like these have serious implications for stocks across the banking sector. On the day that Deutsche’s Bank CDS prices soared, the share price fell sharply cutting €1.6bn off the value of the company. However, the moves were not limited to Deutsche Bank. More than €30bn was wiped off the value of the European Banking Index. At one stage, the sector index had been down around -20% in just a few weeks.

It is not a repeat of 2008, well, not yet anyway

However, compared to 2008, the big banks of major economies are far better capitalised and more stringently regulated than before the Great Financial Crisis. They have regular stress tests performed by banking authorities to ensure their viability against sharp share price declines and recessions. Central banks such as the Federal Reserve and the European Central Bank conduct annual stress tests.

Furthermore, in response to the banking crisis of 2023, central banks have reiterated their intention to maintain financial stability.

However, the moves higher in CDS prices show that there is concern amongst markets. The banking crisis may have been curbed for now, but contagion is always a risk when market fears are elevated. For that, traders will be sure to keep a close eye on the CDS prices of the banks in the months ahead.