Initial Parameters:

- Chart analysis is technical and taken from medium-term historical pattern

- Technical projections based on a twelve-month time horizon

- Targets set are based on the most recent, significant technical adjustment

- Analysis is based on Elliot Wave and Fibonacci techniques

- Technical analysis only guides; exogenous factors can shock any market

- Markets, being capricious, forecasts are subject to revision

- Fundamental analysis can be commissioned on request

- Equity sector analysis is thematic

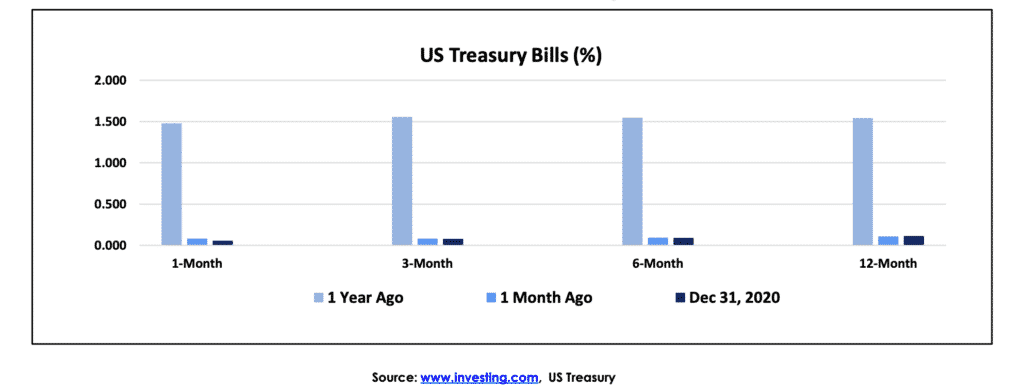

United States of America, T Bills:

- Across the Treasury Bill curve too much cash has chased too little paper

- There is a real prospect of negative yields across the T-Bill curve

- The secured overnight financing rate (SOFR) will follow this path

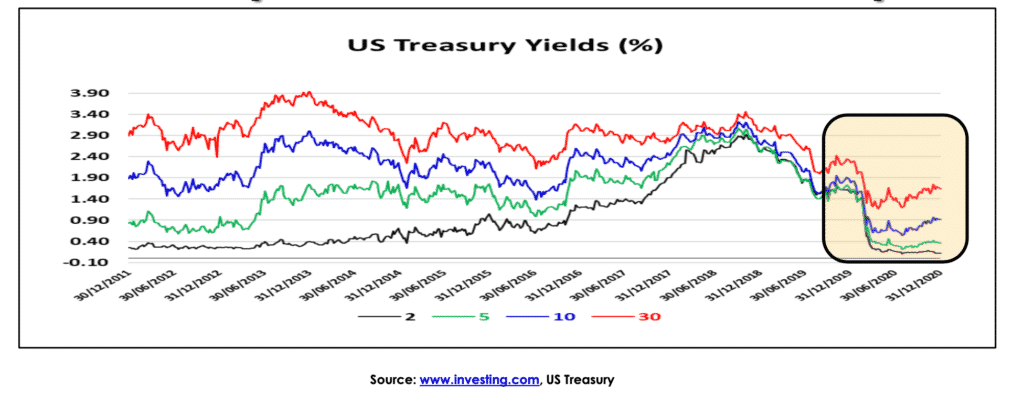

US Treasury Notes and Bond; 2 ~ 30 year

- Since July 2020, T10 note and T30 bond yields have steadily risen

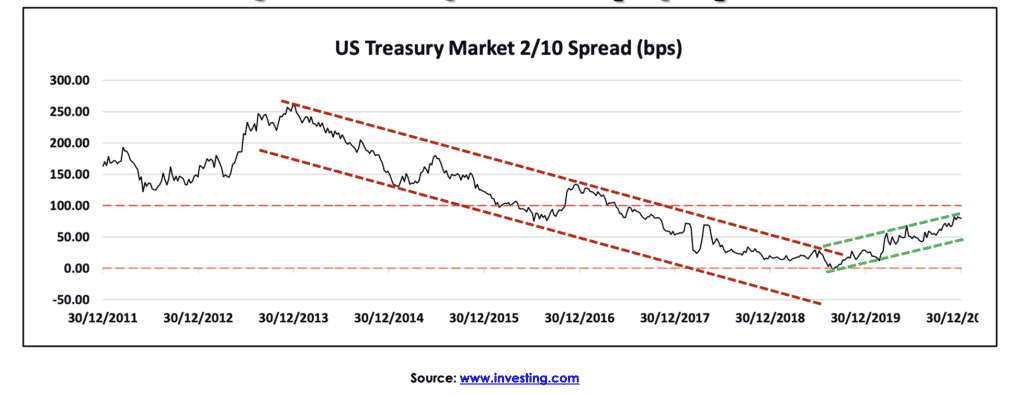

- 2/10 steepened by 53.4 bps since the start of 2020 to Dec 31

- Treasury Department has to quickly signal the path of borrowing

US Treasury 2/10 Spread (bps)

- As Fed has delivered accommodation, so 2/10 spread has recovered

- Any bill shortage will impact the curve out to the T2, T3 and T5

- There will be further steepening

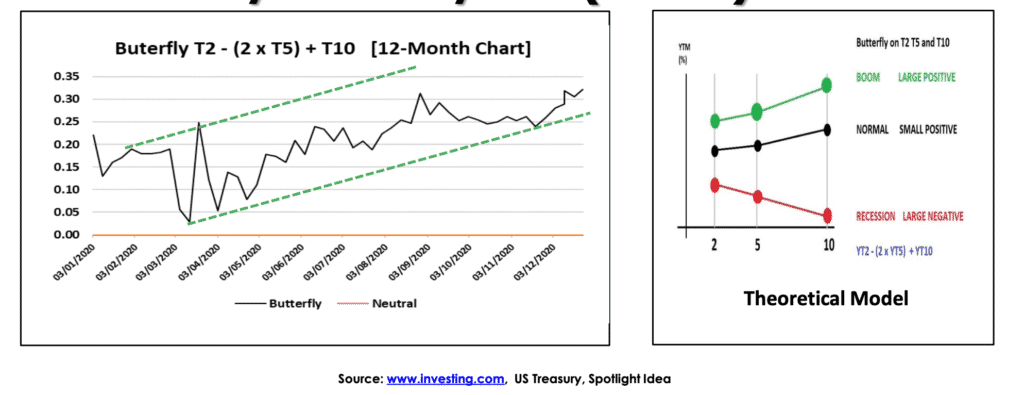

US Treasury Butterfly T2 -(2 x T5) + T10

- Butterfly (Barbell) spread has recovered since April

- The recovery in the economy is supported by this move

- There will be further improvement under Biden and accommodative Fed

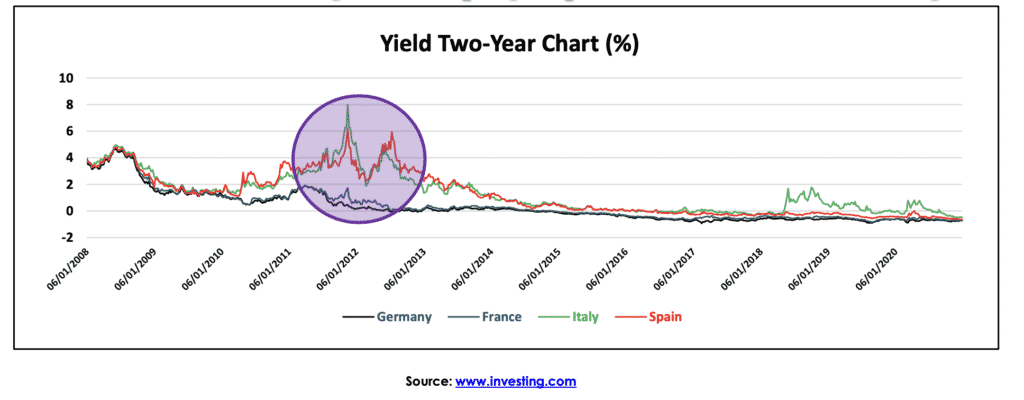

Eurozone ~ 2 year (bps) over Germany:

- Complacency widespread since “…whatever it takes” and “OMT”… … the front end of the market has been skewed by ECB policy

- Italy is a reason to worry as Conte lacks the backing for basic reform

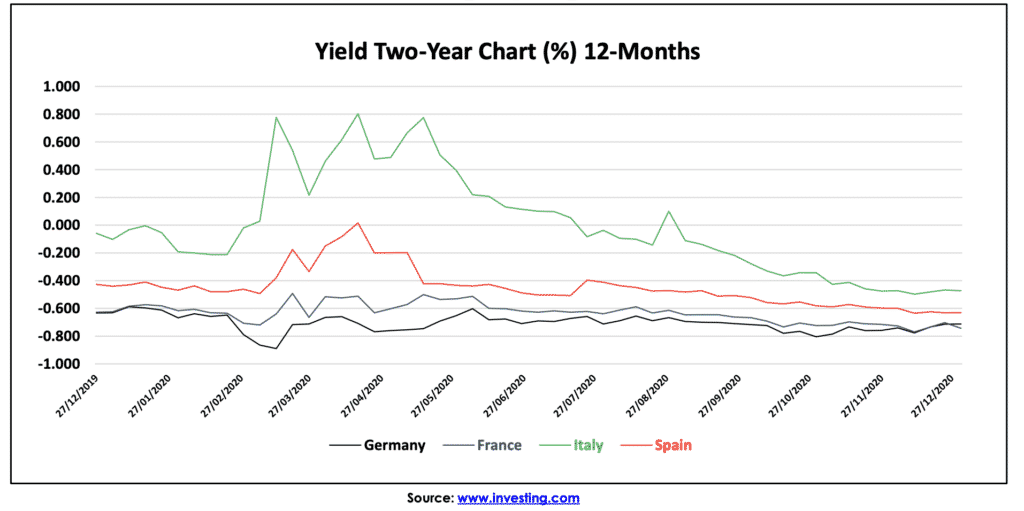

Eurozone ~ 2 year (bps) over Germany:

Why does France yield less than Germany? G2 > F2 3bps Dec 31, 2020!

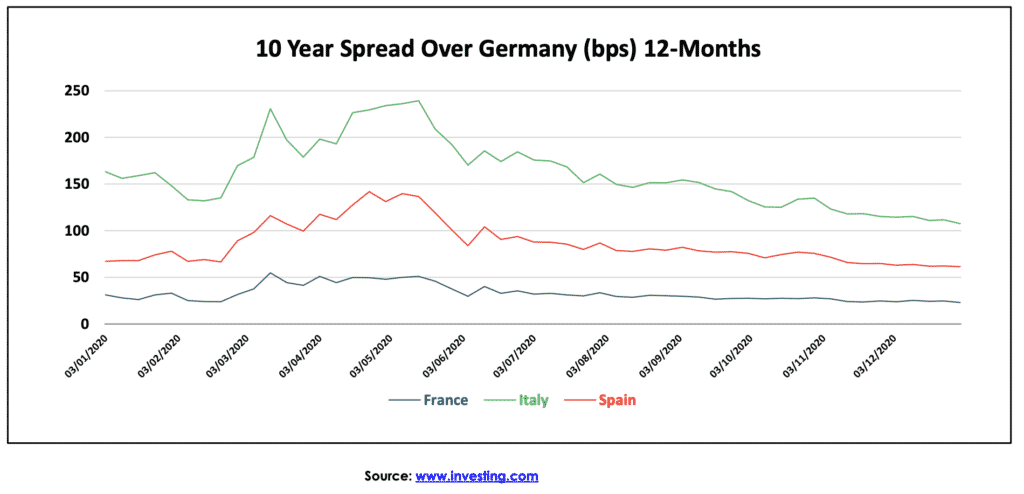

Eurozone ~ 10 year (bps) over Germany:

- Same for 10 year paper…

- Ever since “…whatever it takes” and “OMT”…

- … the long end of the market has been equally skewed by ECB policy

- Look at Italy, trading at a significant margin to Spanish spreads

Eurozone ~ 10 year (bps) over Germany:

France hardly moved, average spread > Germany in 2020 was 33.3bps

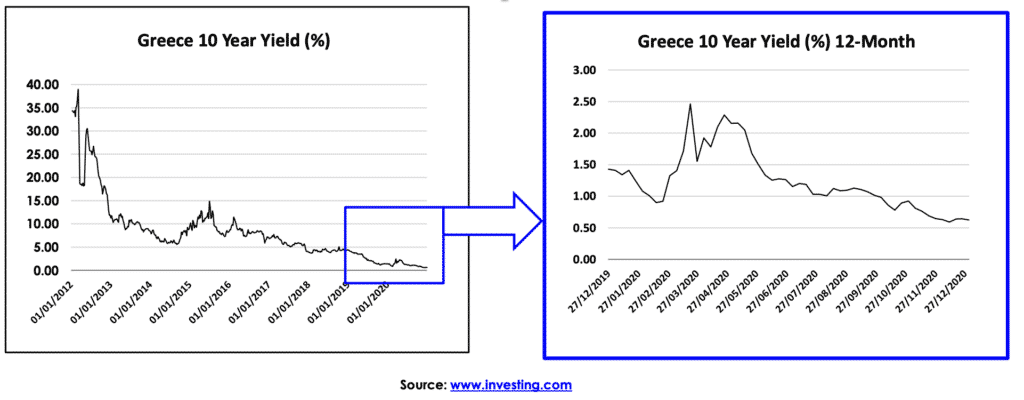

Eurozone ~ Greece; problem overlooked:

- Relief from EU/EZ budget demands aids attempts to recover lost growth

- Large fiscal gap and Debt:GDP at 176.6%, however, GGB10 YTM 0.630%

- Consumer Confidence decreased to -48.30 points in November

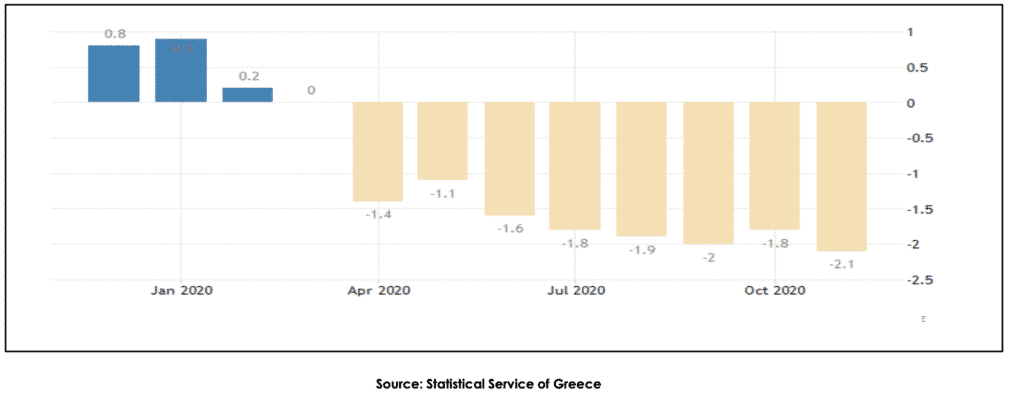

Eurozone ~ Greek inflation collapses

- Consumer prices in Greece decreased 2.1% YoY in November of 2020

- It is the eighth straight month of deflation

- Structural issues not resolved, with youth unemployment at 33%

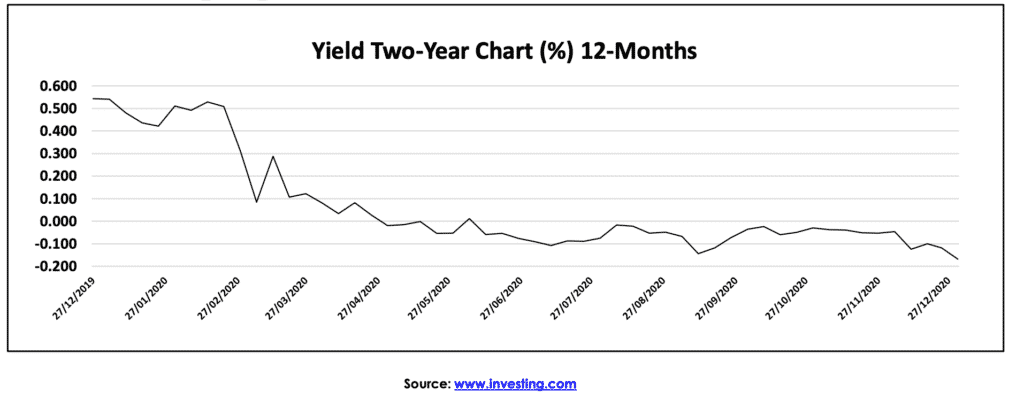

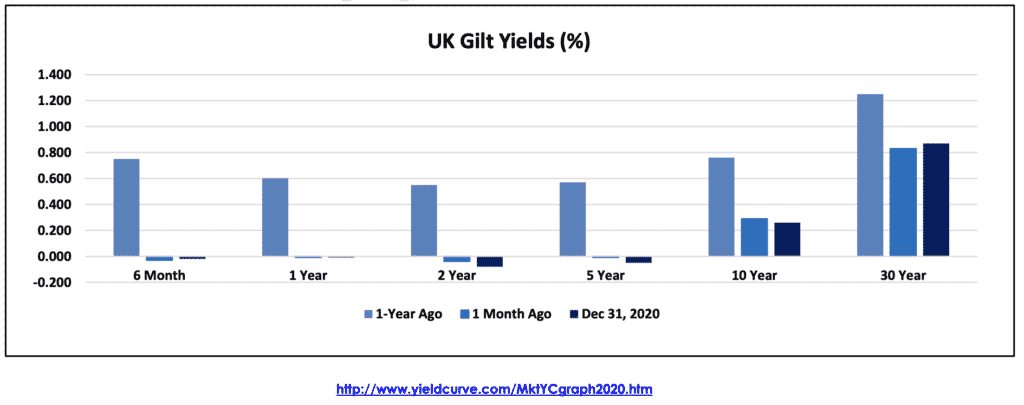

UK Gilts (%):

- UK front end has broken into a declining channel during 2020

- BoE kept rates at 0.1%; may go negative, bond buying still £875 Billion

- Trade deal with EU will stabilise UK GDP growth; COVID-19 still impedes

UK Gilt Yields (%):

- Negative yields out to the 5-Year as 48% of all issuance yields < 0%

- That means £1.25 Trillion ($1.71 Trillion) is a cost to investors to hold

- 2-Year ended at an all-time high, booking best price gain since 2011

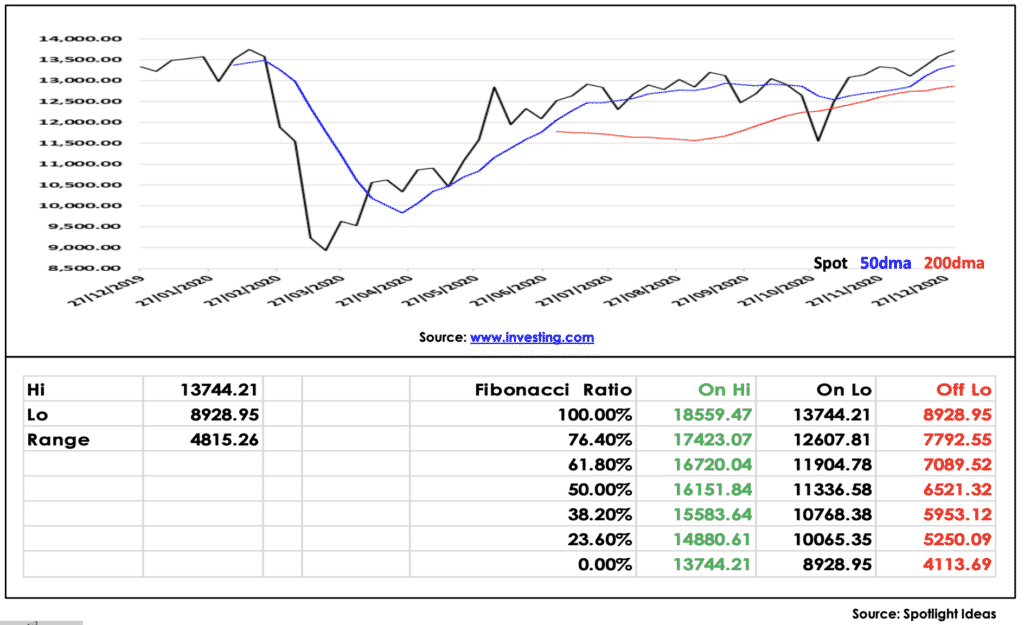

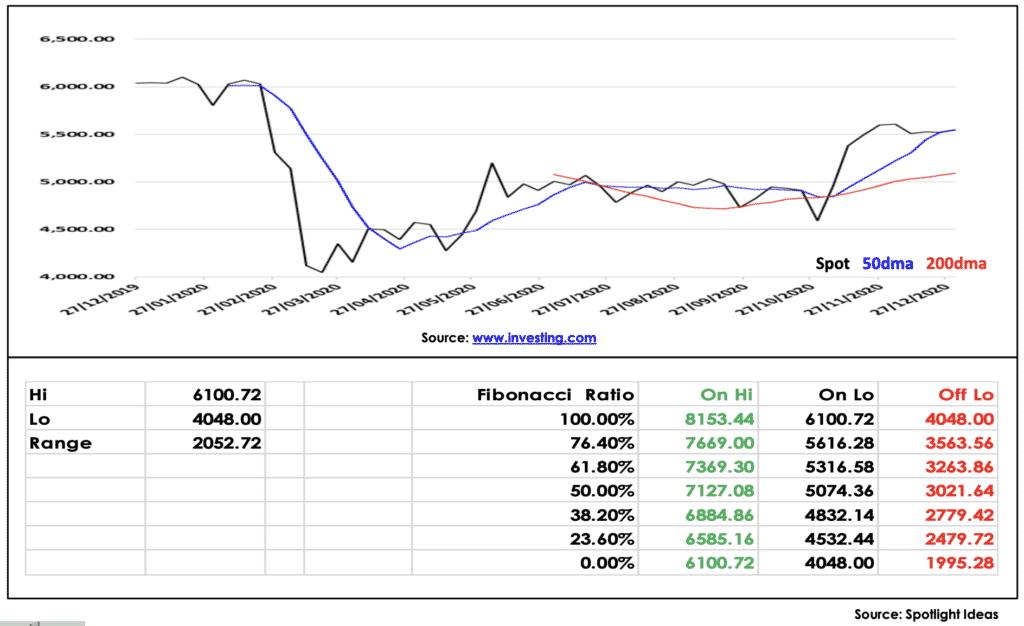

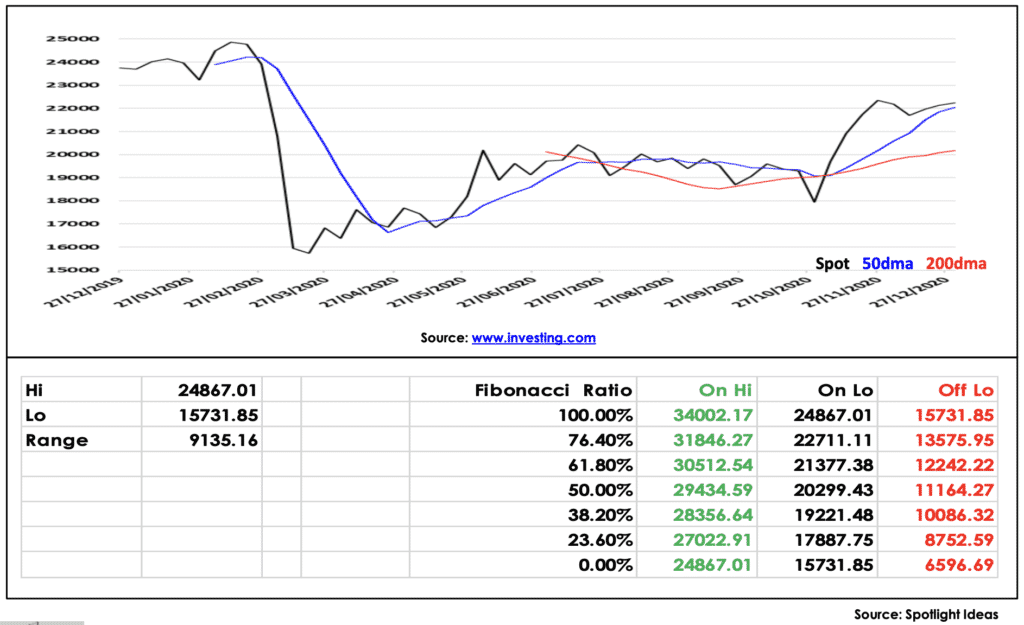

US, European and Chinese Equities

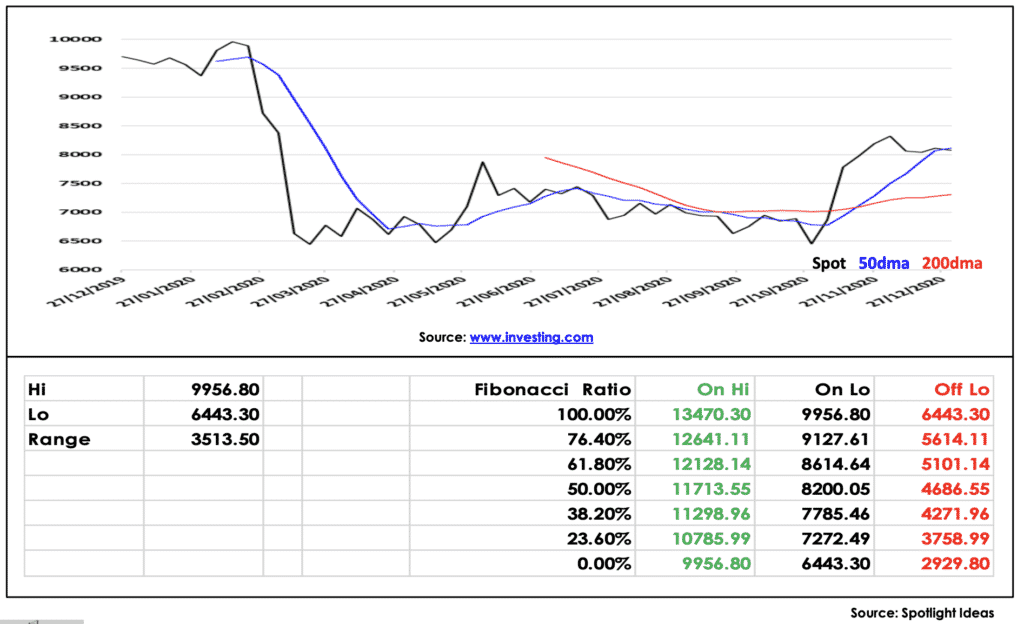

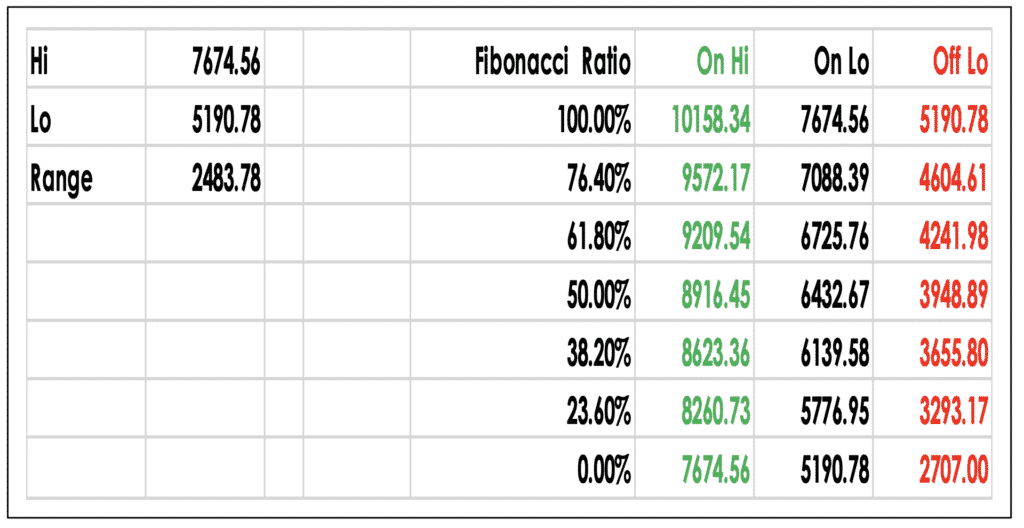

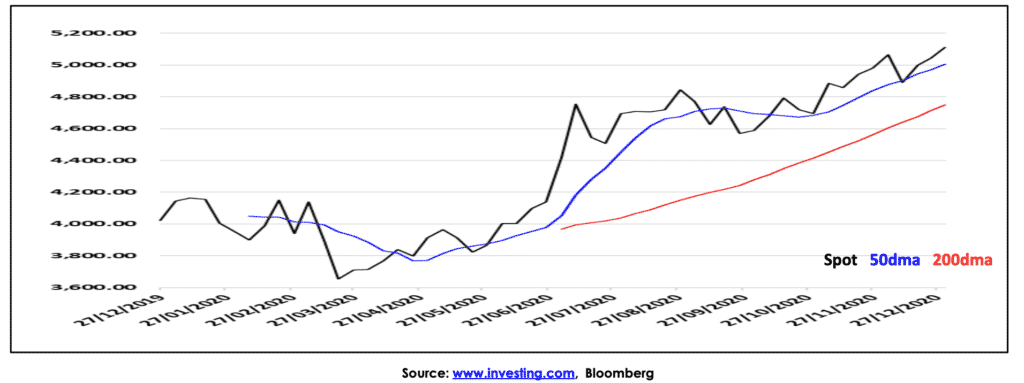

Technical analysis in each chart is over the 12-Month trading range

Given extreme volatility we have shown 50 and 200 day moving averages for 2020

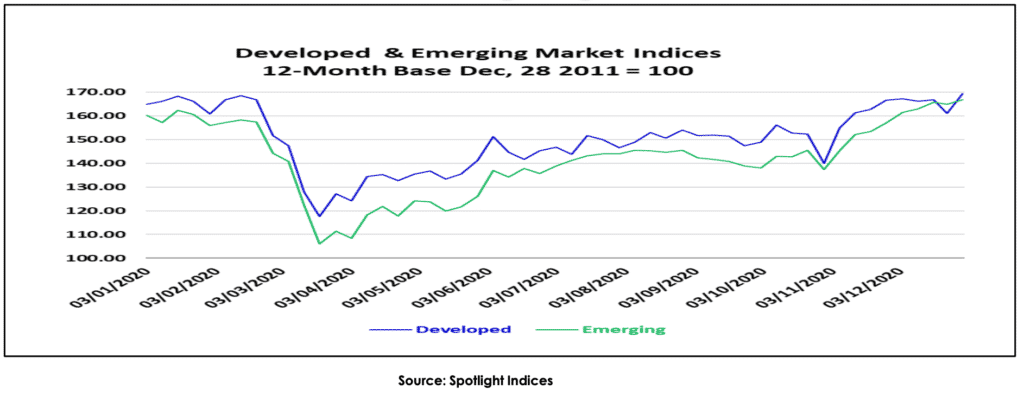

Developed cf. Emerging Market Equities:

- Post March/April collapse developed and emerging equities rebound

- Emerging equities have closed the gap and more sought than EM debt

- Expectation of good cash flow from domestic demand recovery

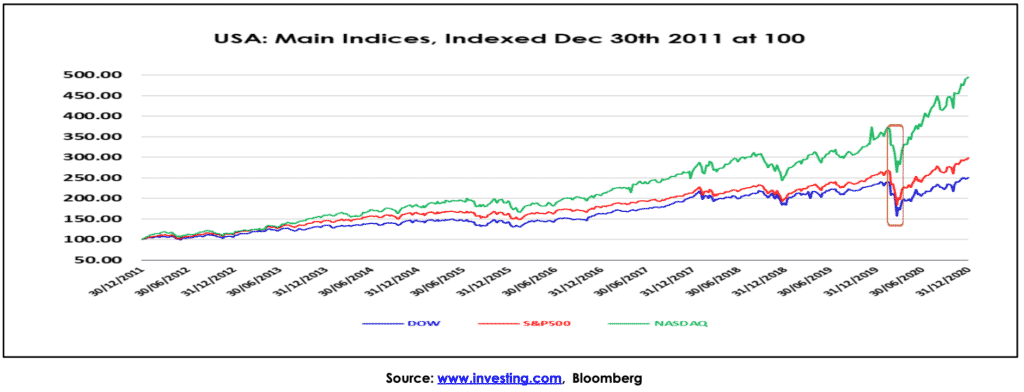

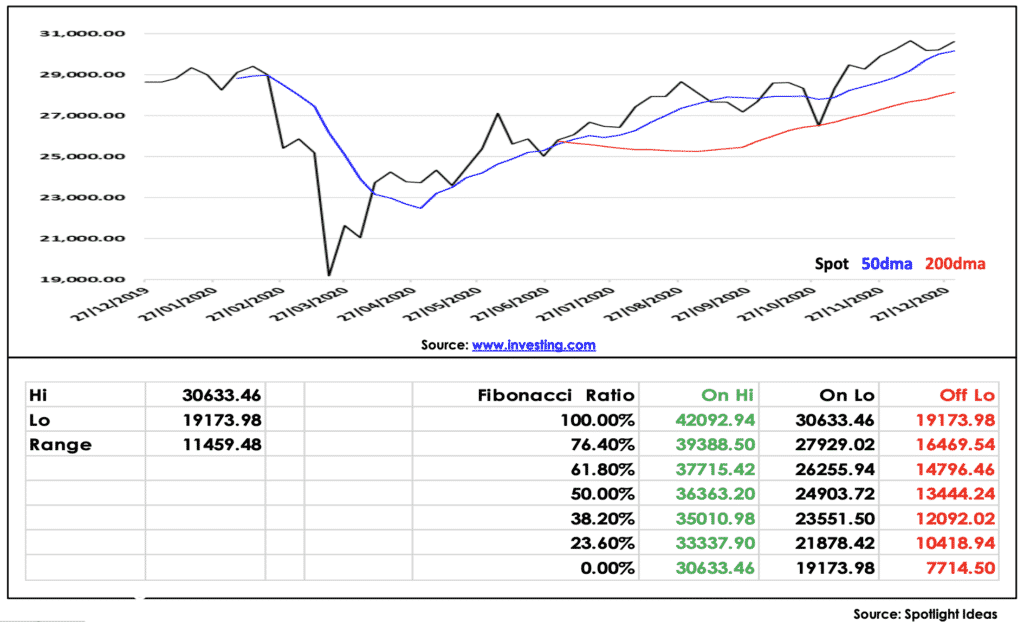

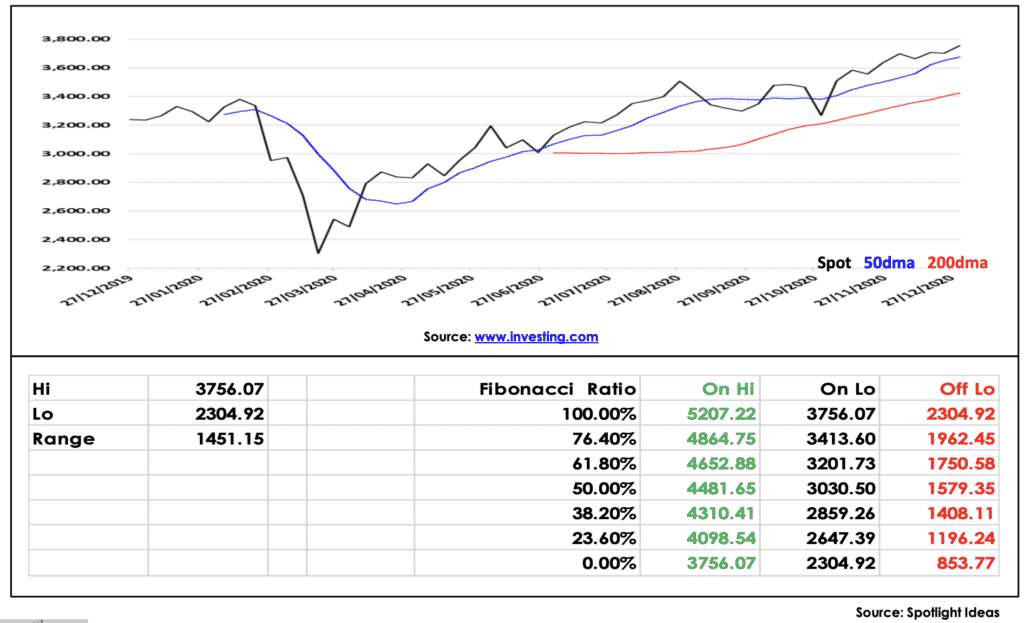

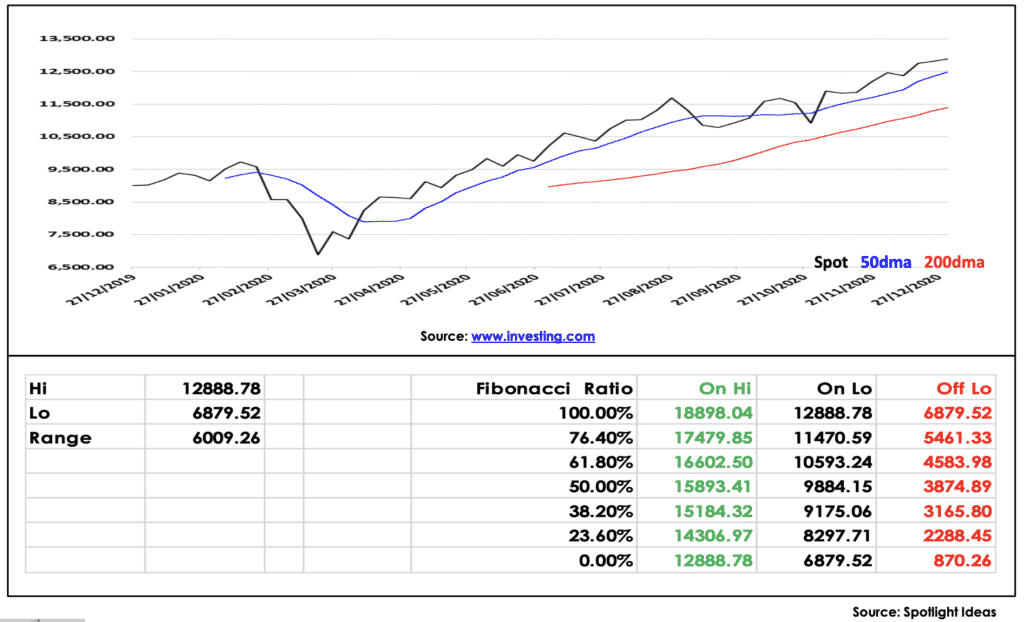

US Equities:

- Main US equity indices enjoyed a steady expansion since March

- There will still highly volatile sessions as COVID-19 rampages

- Markets still optimistic about “Biden Boost” via infrastructure; stay bullish

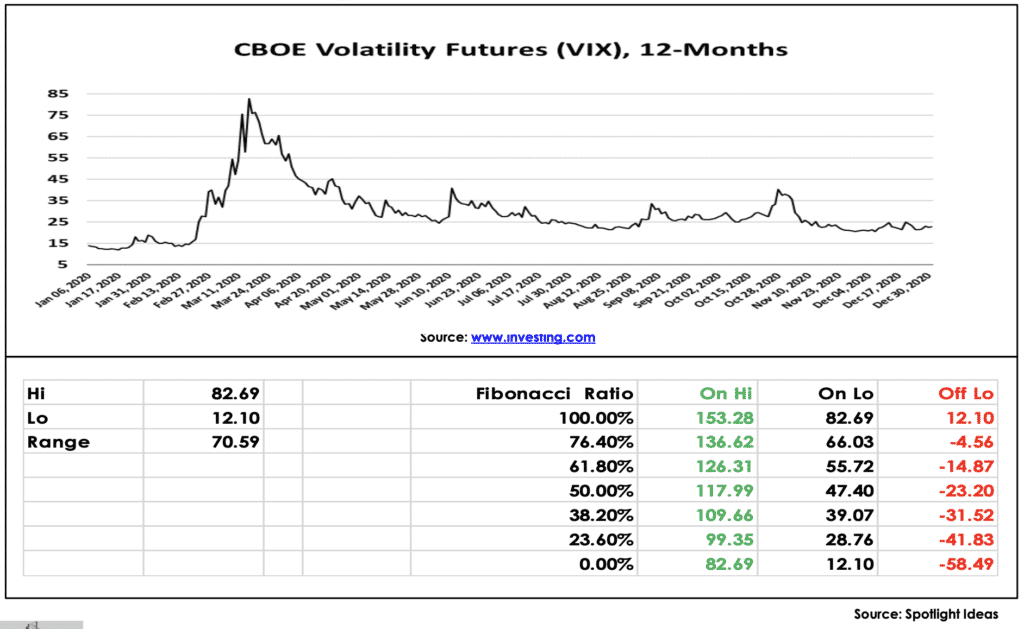

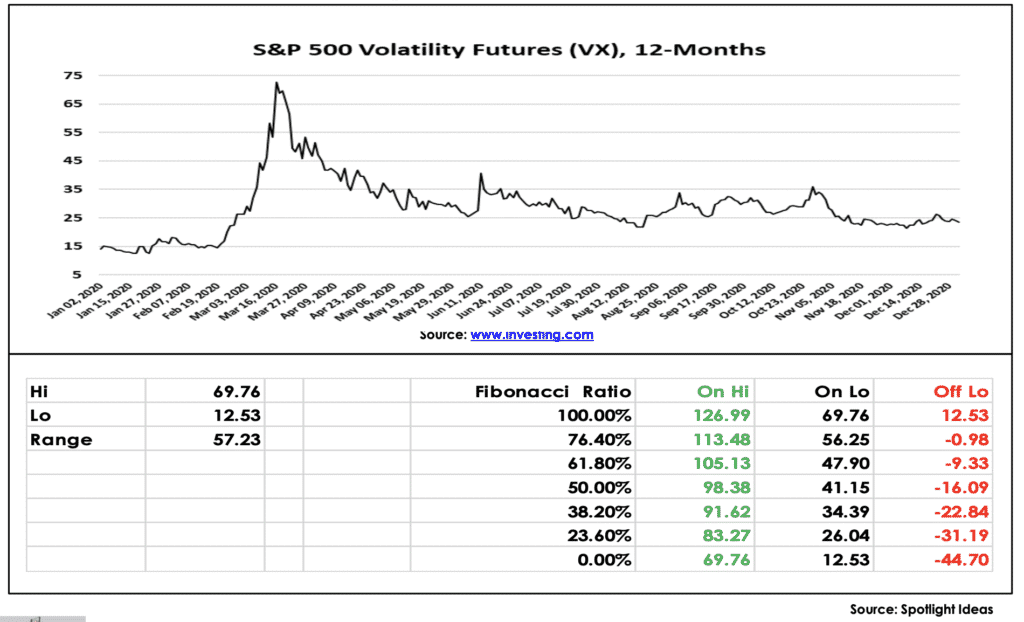

CBOE Volatility VIX:

S&P 500 Volatility Index:

Dow Industrials 12 – Month & Fibonacci

S&P 500 12 – Month & Fibonacci:

NASDAQ 12-Month & Fibonacci:

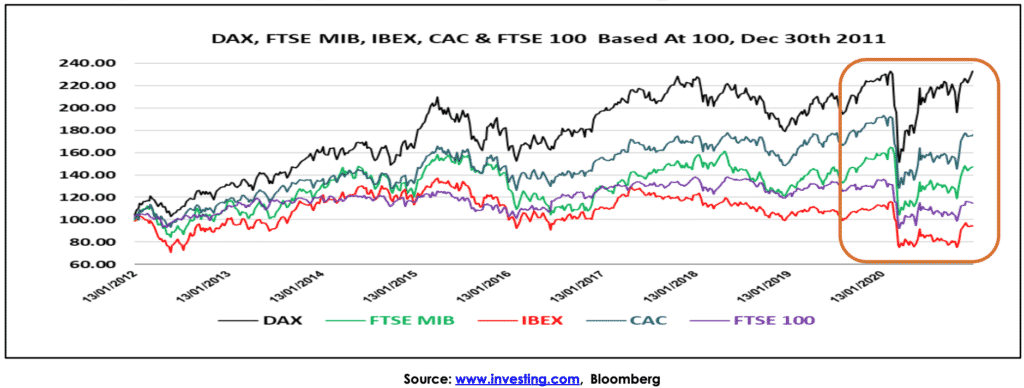

European Equities, leading markets

- All recovered after suffering a setback on COVID-19 worries

- DAX is the most secure investment; indeed it is pulling away from the rest

- IBEX 35 has underachieved with respect to its peer group

DAX 12-Month & Fibonacci:

CAC 40 12-Month & Fibonacci:

FTSE MIB 12 – Month & Fibonacci:

IBEX 35 Fibonacci:

FTSE 100, the key “Non-Euro” European:

- FTSE 100 has found breaking back above the 7000 level difficult

- “Brexit” is over…at least in the main, FTSE to rise on vaccine hopes

- FTSE 100 will press ahead in 2021 as private sector recovers

FTSE 100 Fibonacci:

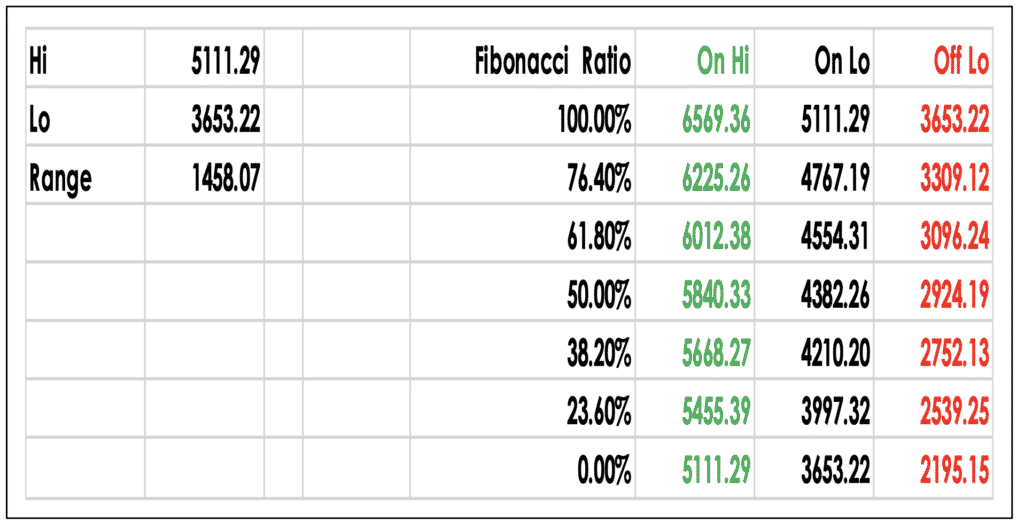

CSI 300 12 – Month:

- CSI 300 extends gains to make new 5 1⁄2 -year highs

- Driven by consumer stocks as consumer confidence seeking new record

- Investors hope for more measures to spur the country’s consumption

CSI 300 Fibonacci:

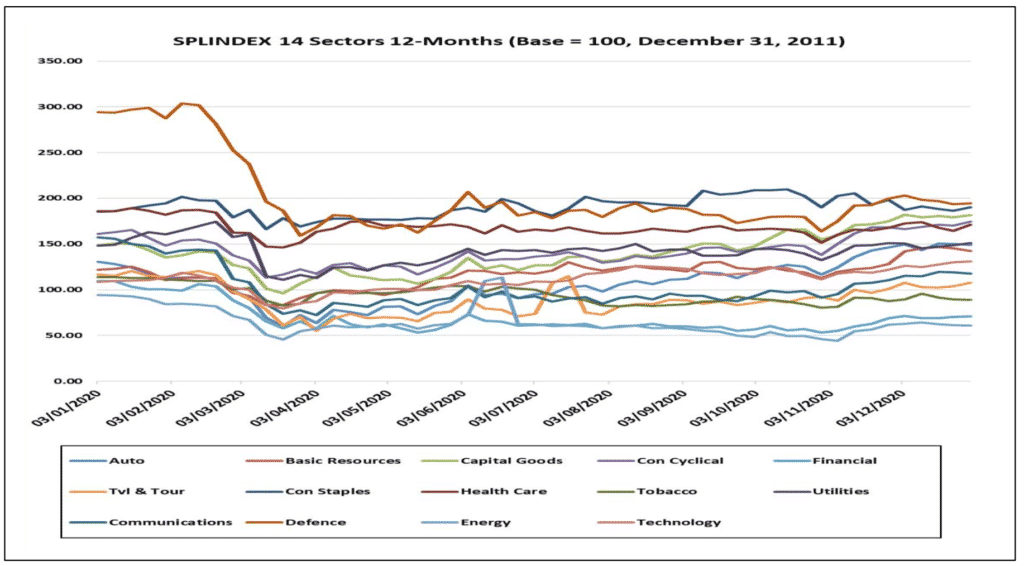

Spotlight Indices: 14 Equity Sectors:

- Cyclical…

- Auto…Basic Resources…Capital Goods…Consumer Cyclical… Financial…Travel & Tourism

- Defensive…

- Consumer Staples…Health Care…Tobacco…Utilities

- Sensitive…

- Communications…Defence…Energy…Technology

We asses on a modified traffic light scale:

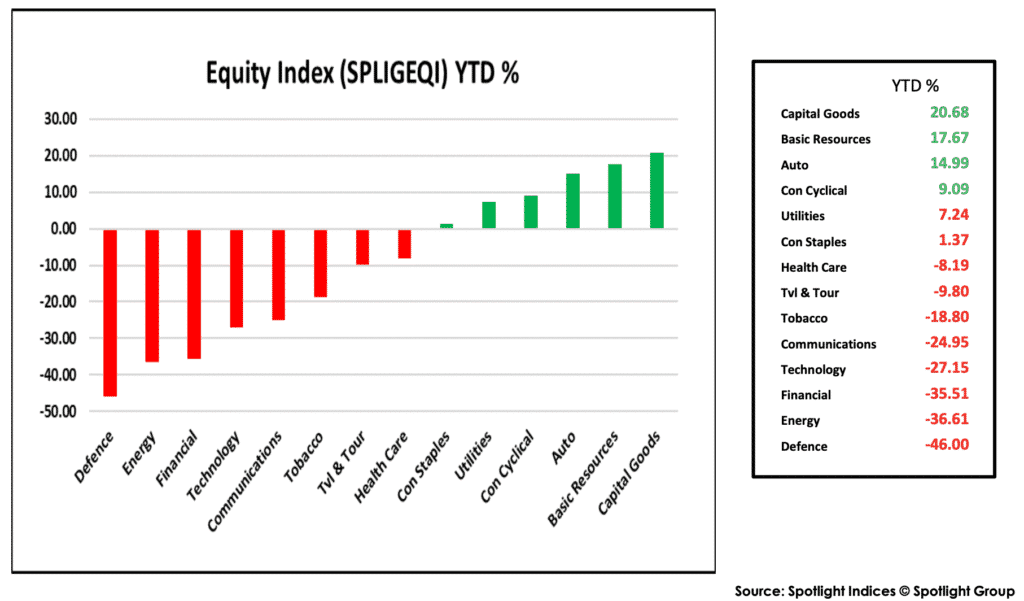

Equity Sector 2020 Performance:

Equity Sector 2020 Performance:

Auto:

- Global light vehicle production fell to 69.3 million units

- Sales in 202 were seen at 69.6 million, -18.0%

- The pandemic remains a clear and present danger to the autos sector

- High levels of accommodation have boosted shares

- New car sales will rise by 15% in 2021

- Commercial-vehicle sales will increase by 16% in 2021 mirroring the collapse in 2020

- Automakers forced to review global operations

- This will result in plant closures and job losses

- Therefore, the industry will consolidate

- Electric vehicle sales are set to rise from 2.5 million in 2020 to 3.4 million this year, mostly in Europe

Basic Resources:

- Mining firms had over produced before COVID-19 hit

- Major players to book productivity gains

- That can be boosted by commodity price rises in 2021

- Much depends on Bidens’s infrastructure plans

- China will be a big spender on domestic infrastructure

- It will, however, pare back the Belt & Road activities

- The ongoing labour disputes in Latin America may well boost copper

- We will see a reduction in tariffs

Capital Goods:

- Q3 return better than expected after a weak H1 2020

- Expect good activity in Q3 and into 20201

- In 2021 aggregate sector revenues to increase by 5% after a more than 8% drop in 2020

- Driven by economic growth and increased industrial investment in most end markets

- Customer activity is linked to the economic cycle

- Best share performance to be seen in APAC region

- However, do not miss a N. America and European bounce

Consumer Cyclical:

PowerPoint Presentation

- Retail sales declined by 5% in 2020

- Investors are looking for an earning recovery

- They will gain 4% in 2021; it will not be even

- ❖ Africa 1% ~ 3%

- ❖ Asia 5% ~ 7%

- ❖ Europe 1% ~ 3%

- ❖ North America 4%~6%

- ❖ South America 2% ~ 4%

- COVID-19 accelerated the questions over a bricks and mortar retail approach

- Consumers will increase migration to online

- This will require sellers invest in sophisticated order and delivery systems

- High end luxury will thrive

- There will be more bankruptcies among once famous names

Financials:

- Financial services successfully migrated online

- Banks were crucial in stabilising the economy

- Transmitted government stimulus and relief programs

- Consequences of COVID-19 not on the same scale as those during the Global Financial Crisis of 2008–10

- There will, however, be a new competitive landscape

- Branches will close amid increased digitalisation

- COVID-19 has shown only competent digital banks will survive…

- …Focus on social distancing, personal safety etc.

- Progress fettered as deep provision for NPL’s is made

- In the US, Average ROE fell to 5.6% in 2020, this year will be 8.0% but in 2022 it will bounce to 11.6%

Travel & Tourism:

- Last year really dealt the sector a severe blow … -54.2% by April

- United Nations World Tourism Organisation (UNWTO) show that international tourist arrivals declined 70% in the first eight months of 2020 cf. 2019

- Amounts to 800 million fewer international arrivals year-to-date for 2020, and a loss of S$730 billion in tourism revenues

- There have been signs of tourism demand shifting to domestic travel in China

- Once vaccines are widely adopted Europe and America’s can follow

- 80% of industry experts expect a recovery to begin in travel during 2021…

- …However, the industry will not be at pre COVID-19 levels until 2023

Consumer Staples:

- Consumer Staples 6th best sector in 2020

- e-Retailing continues to surge

- Over 50% of e-commerce in 2018 will be in China

- The recovery reversed in October because money has moved to cyclicals

- In retailing the timing and trajectory of the recovery back to pre-pandemic norms is up for debate

- Until there is a full return to the workplace the market dynamic for “Staples” looks favourable for online sales

- There will be a greater presence for the “disruptors”

- Store chains with heavy value of “Bricks and Mortar” assets are set to struggle

- Increase in M&A as bottom line is squeezed

- With over 260 sub groups it is often hard to be in the right area of a key defensive sector

Health Care:

- National health services under budget strain, globally

- However, state budgets will rise by 6% as public will demand greater resources post COVID-19

- State systems cannot have a blank cheque, they have to be accountable

- Can health services smoothly deliver the vaccine?

- There will be a struggle to recover lost ground in non COVID-19 care

- Can Biden afford to reverse light touch to US regulation

- Biotech firms to work even closer with “Big Pharma”

- Expanded use of smart computer modelling for trials

- This is an industry where R&D will garner high levels of investment attention

Tobacco:

- Sales declined in 2020, however, operating profit is set to rebound 5% ~ 10% (Moody’s)

- Long-term impact of COVID-19 on consumption too early to gauge

- Traditional tobacco sales will decline5% as consumers switch to lower priced products

- This hasten the move to alternative products although this will see tighter regulation

- The curiosity is the regulation will prove a barrier to entry and so protect profits of existing key players

- Leverage ratios will continue to improve despite high dividend payments

- Free cash flow and available cash balances will be used to repay pending debt maturities

Utilities:

PowerPoint Presentation

- Global utilities face 2021 with issues of how supplies are provided front and centre for the industry

- Competition authorities will investigate the excess of “Monopoly Power”

- Therefore, can the leading incumbents retain their level of market share?

- Challenge is delivering for customers and shareholders at a time of transformation

- Internet of Things (IoT) will drive the “Smart Home”

- This will drive a world of Demand Side Response (DSR)

- Major hurdles to overcome are: ❖ Decarbonisation with 2030 and 2050 targets ❖ Security of supply – especially for water

❖ Affordability of supply

• Are utilities sufficiently resilient to the pressures of changing demographics and climate?

Communications & Media

- Delays to events such as the Tokyo Olympics, European Football Championships and the latest James Bond movie hit revenues

- Advertising revenue fell 7% in 2020; it will rebound 6% in 2021 to $573 Billion (Magna Research)

- Advertising in APAC will grow the fastest

- US will be slowest after the 2020 election $ splurge

- The shift in advertising to online will continue

- Thus, print advertising will retreat further

- TV advertising will rise 2% (Zenith Media) and radio by 1%

- Cinema badly needs a return of customers, however, they may only make money on blockbusters

- On demand and streaming will rise dramatically as many movies will go straight to Amazon, Netflix etc

Defence:

- Delays to full capacity commercial travel means defence contractors will outperform civilian plane manufacturers

- Countries will spend on strengthening their military forces as geopolitical tensions intensify

- Global defence spending is expected to grow 2.8% in 2021, so exceeding $2 Trillion mark

- Under Biden defence spending in the US is likely to remain flat in 2021

- As funding continues to increase and costs decline, the space industry will experience increased opportunities

- Look for growth in secure satellite broadband

- Space will increasingly become a military domain and so space launch services are also expected to record strong growth of 15% YoY in 2021 (Deloitte)

Energy:

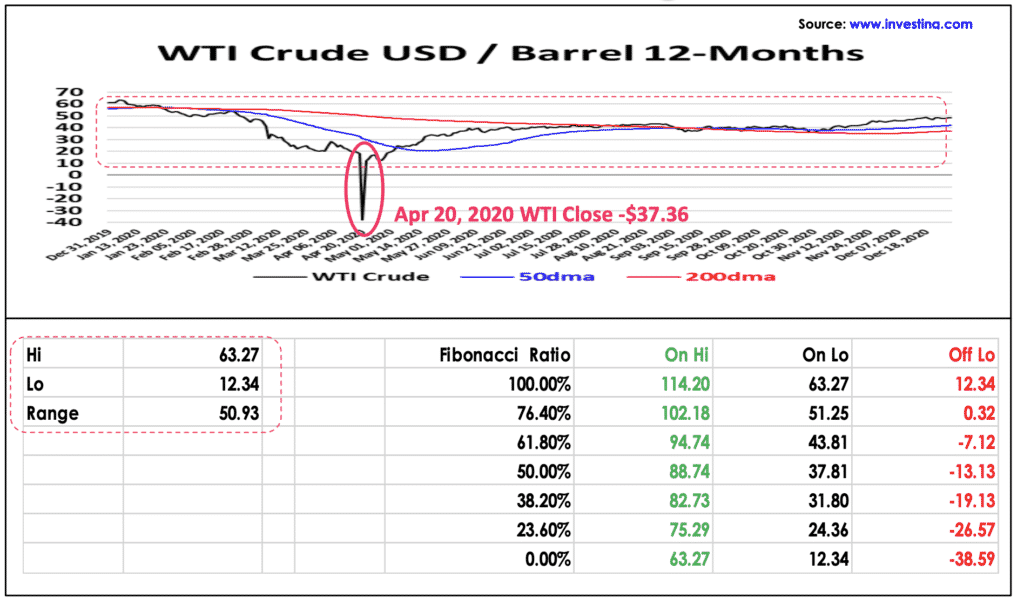

- Demand for energy collapsed during the pandemic

- On April 20, 2020 WTI closed at -$37.63/barrel

- Since then crude oil volatility as barely flickered

- Little improvement seen in the market in H1 2021

- The long-term, H2 2021 and 2022 one can be optimistic about a rebound of oil demand

- OPEC+ will be the dominant factor for 2021 oil supply

- Under Biden we may see oil flows from Iran and Venezuela

- Prices will slowly rise in H2 2021, however, caution is advised, given uncertainties regarding OPEC spare capacity and COVID-19 vaccine deployment

- Renewables, nuclear, and renewable fuel growth to accelerate and further challenge fossil fuels

Technology:

PowerPoint Presentation

- The outlook for technology is stable

- It is supported by declining macro uncertainties and reduced supply chain disruption

- Industry volatility will reduce

- Secular growth supported by technology adoption across various industries will reduce the industry’s reliance on IT demand

- We look for single-digit overall technology hardware spending growth in 2021 driven by

- ❖ Data centre capacity expansion

- ❖ 5G buildout

- ❖ Increasing content in auto and industrial functions

• M&A to continue fuelled by

- ❖ Investor confidence

- ❖ Innovation stream

- ❖ Cheap capital

- ❖ Push to create earnings growth by acquisitions

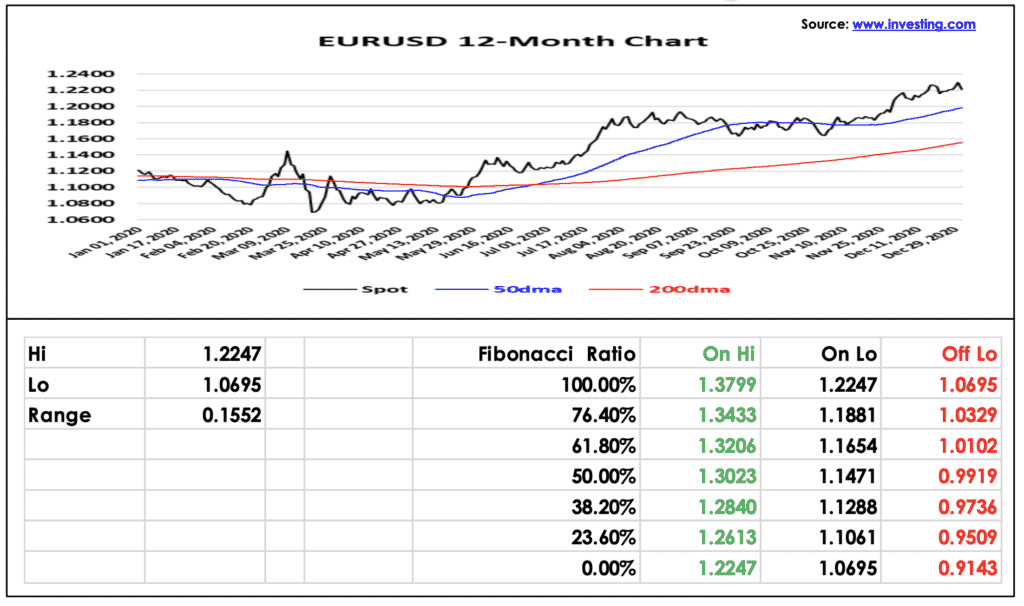

Foreign Exchange Rates

Technical analysis in each chart is over the 12-Month trading range

EURUSD: In 2021; $ will make gains

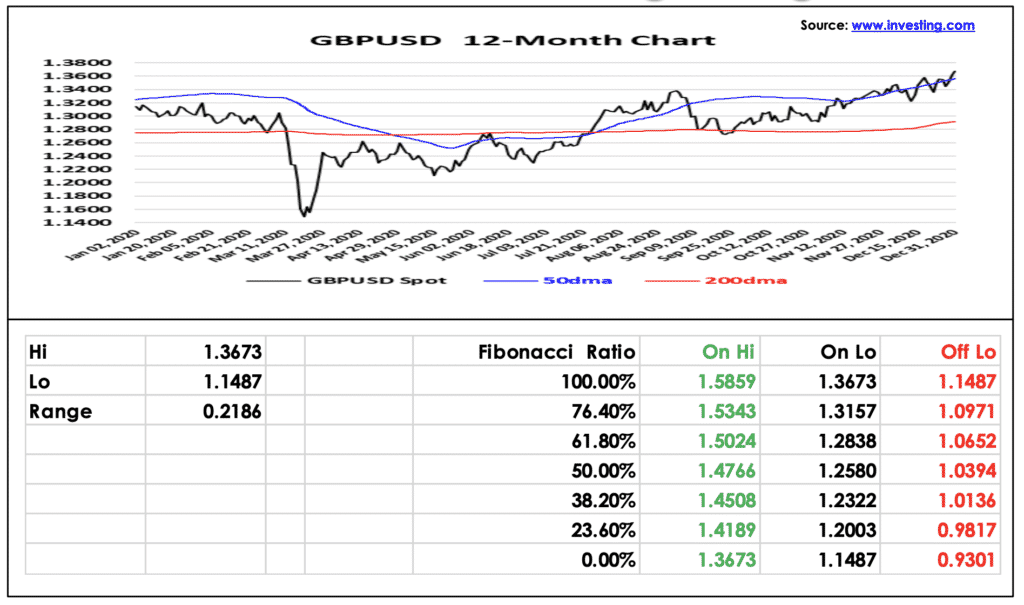

GBPUSD: £ to fade as BoE go negative

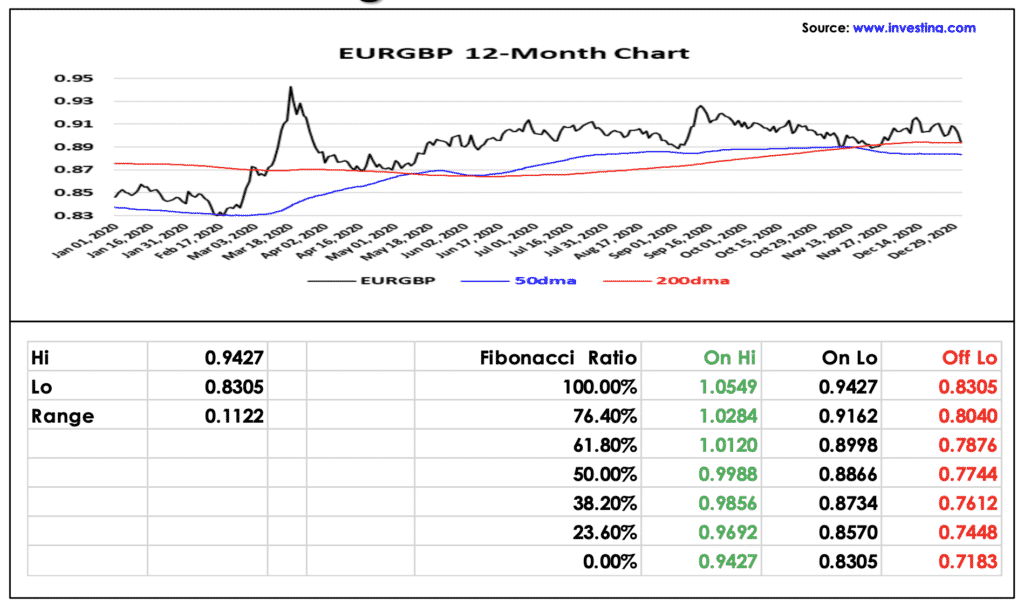

EURGBP: € will gain as Brexit bites

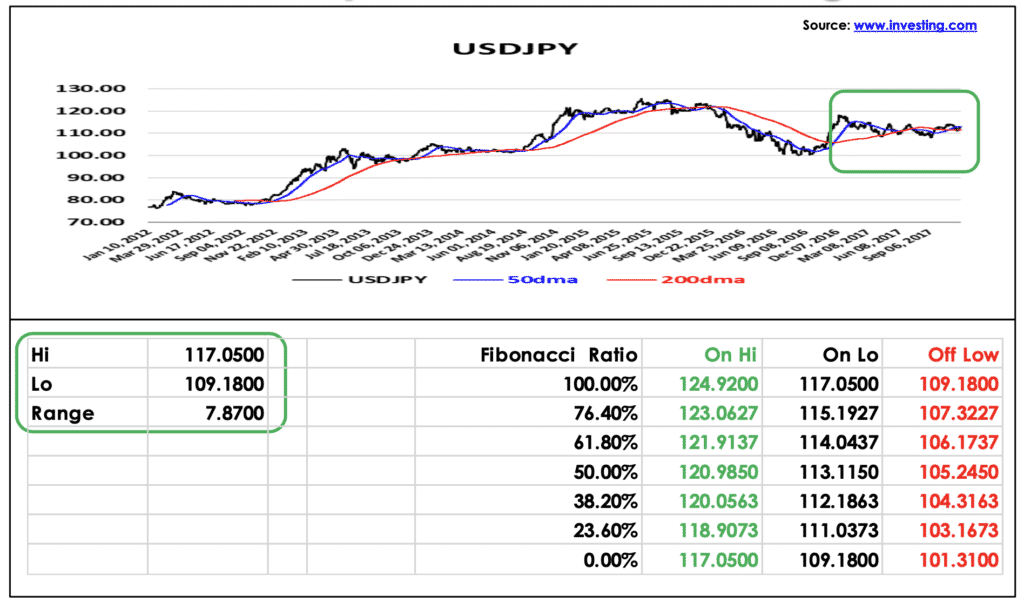

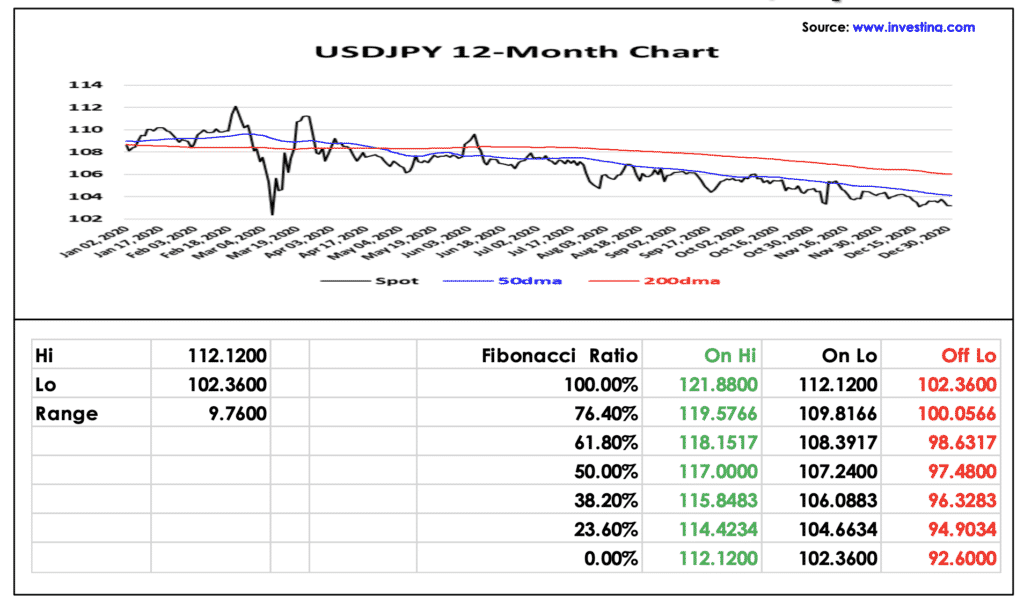

USDJPY: Ready to breakout for $ gains

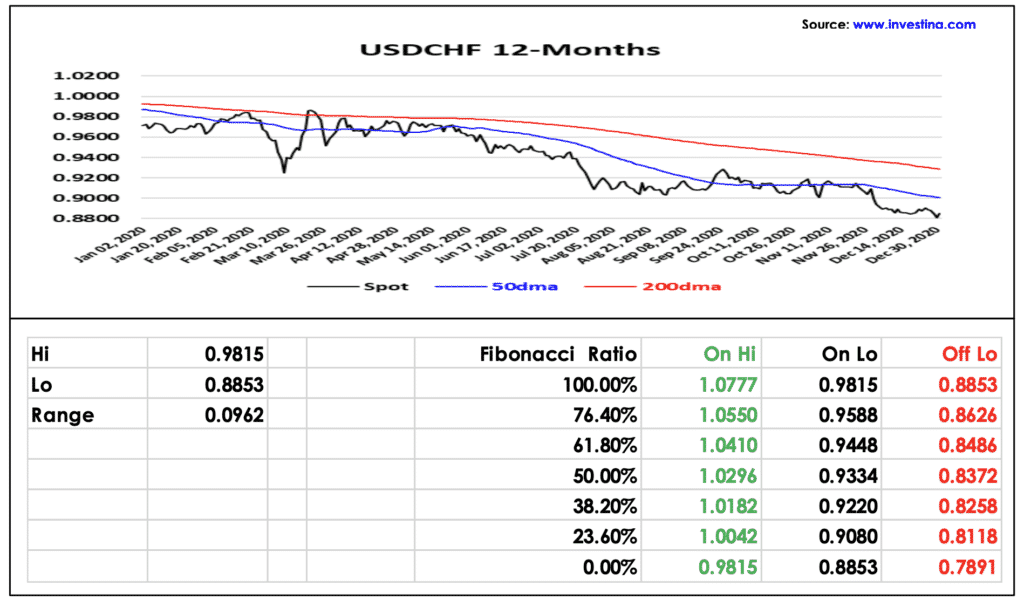

USDCHF: Bear trend will reverse at 0.8372

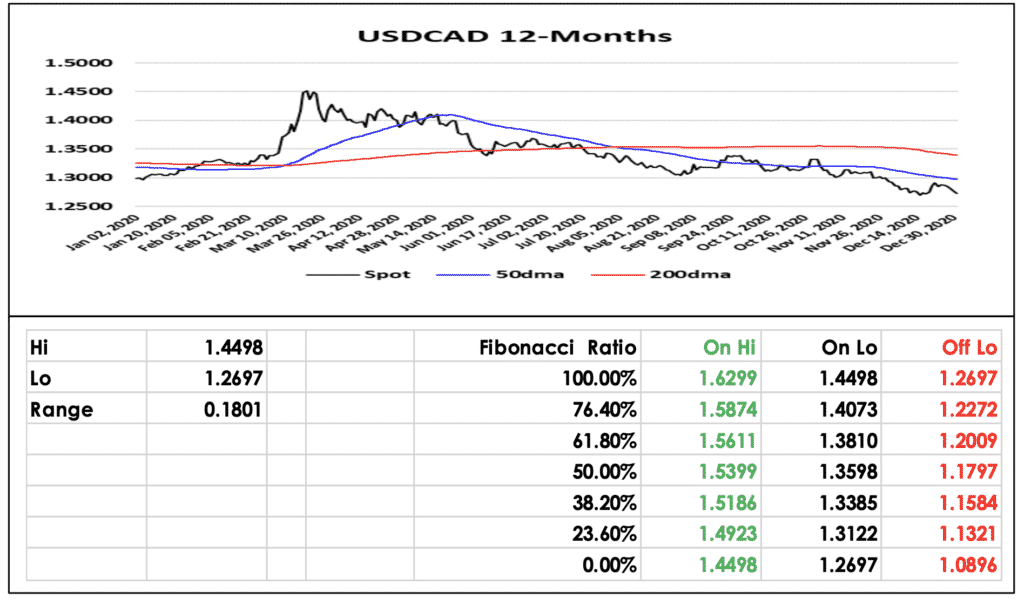

USDCAD: 1.2971 is key to US gains

USDJPY: Break 104.66; heralds $ upside

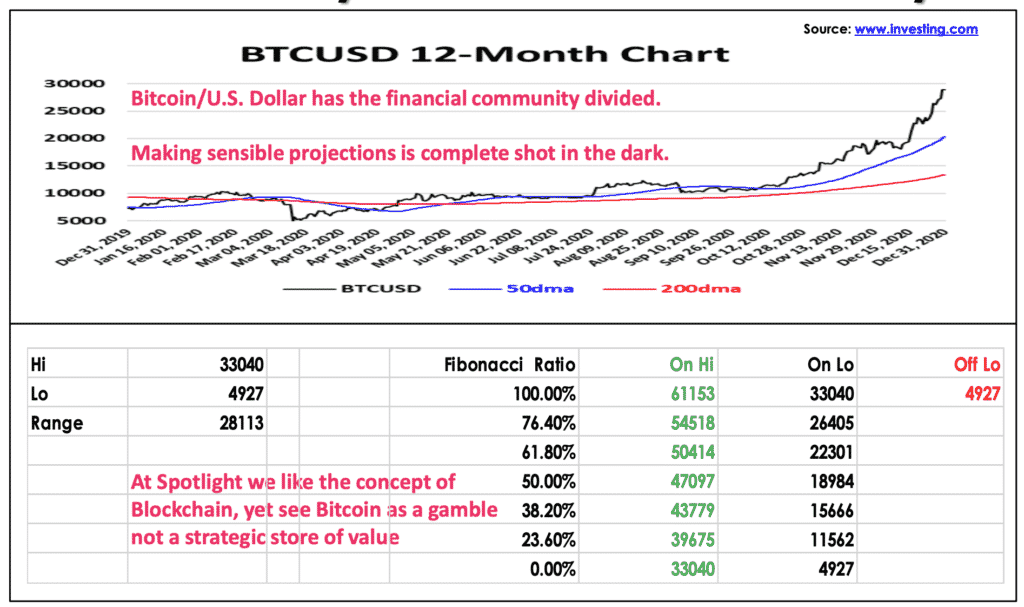

BTCUSD: Can you handle the volatility?

Commodities Energy, Metals Food Products

Technical analysis in each chart is over the 12-Month trading range

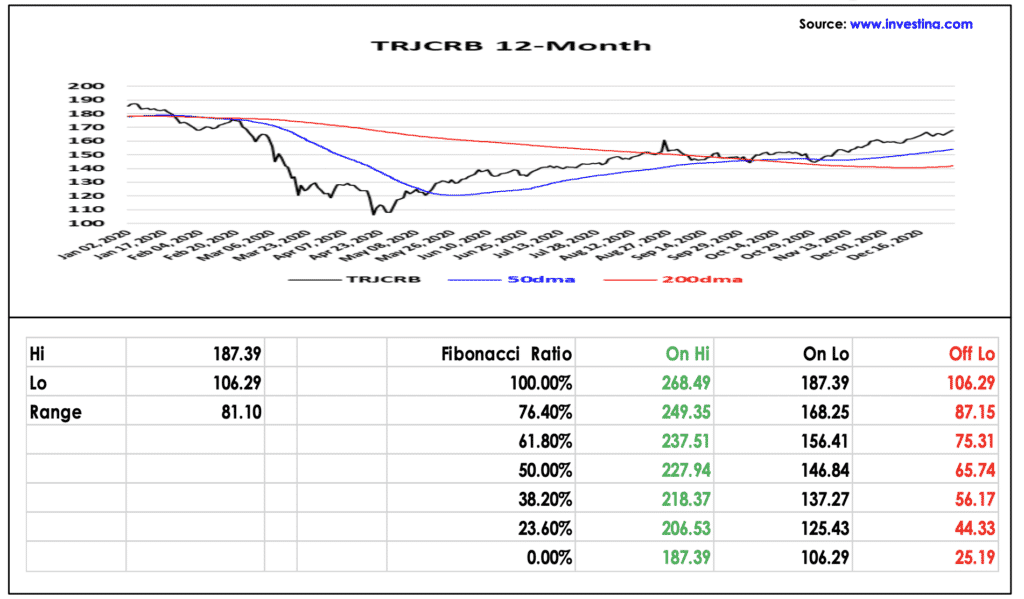

Thomson Reuters/Core Commodity CRB

Crude Oil WTI USD/Barrel: Ignore the – ve

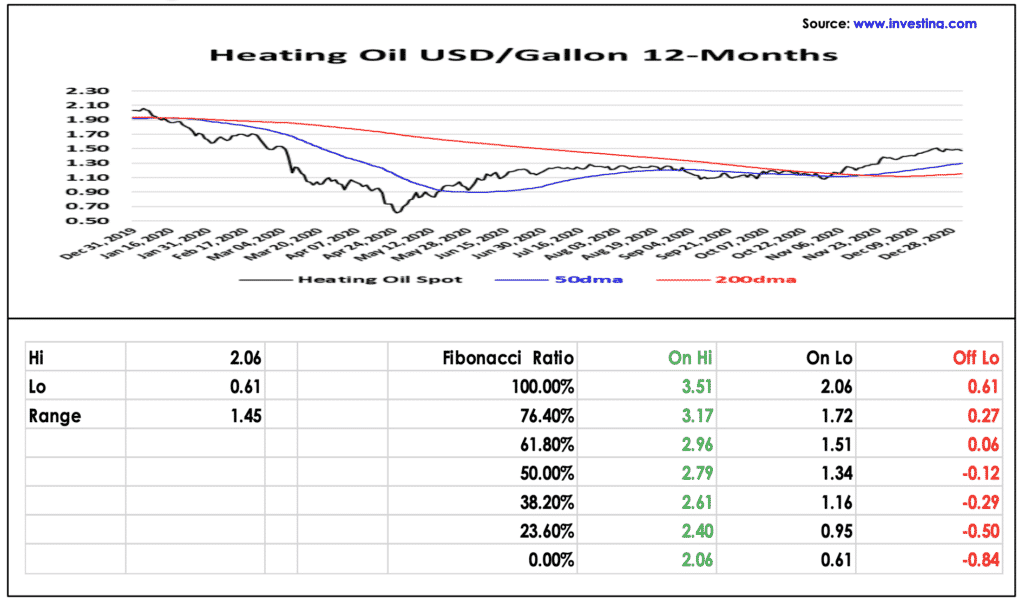

Heating Oil USD/Gallon:

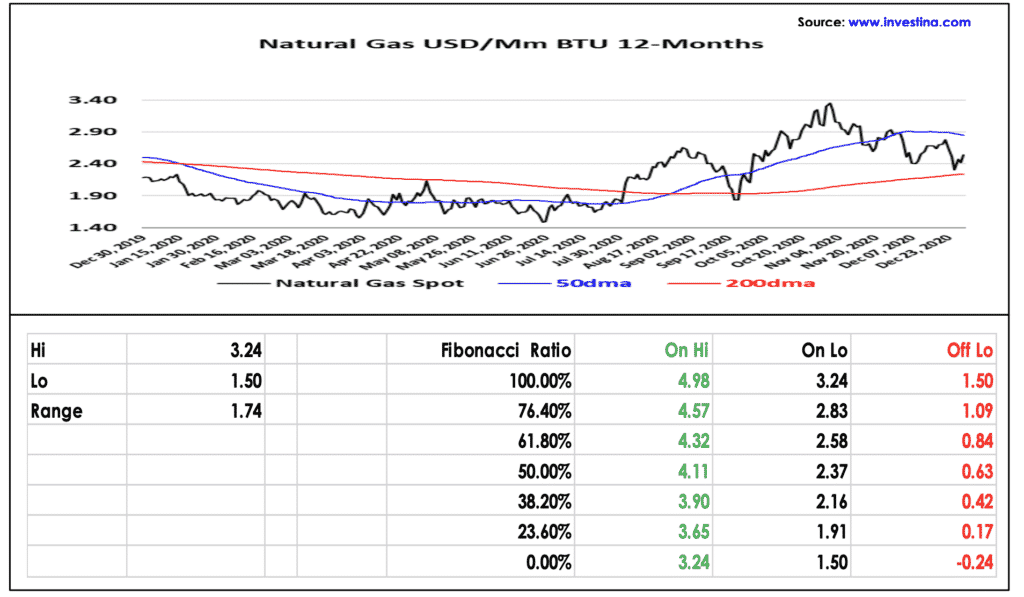

Natural Gas USD/Mm BTU:

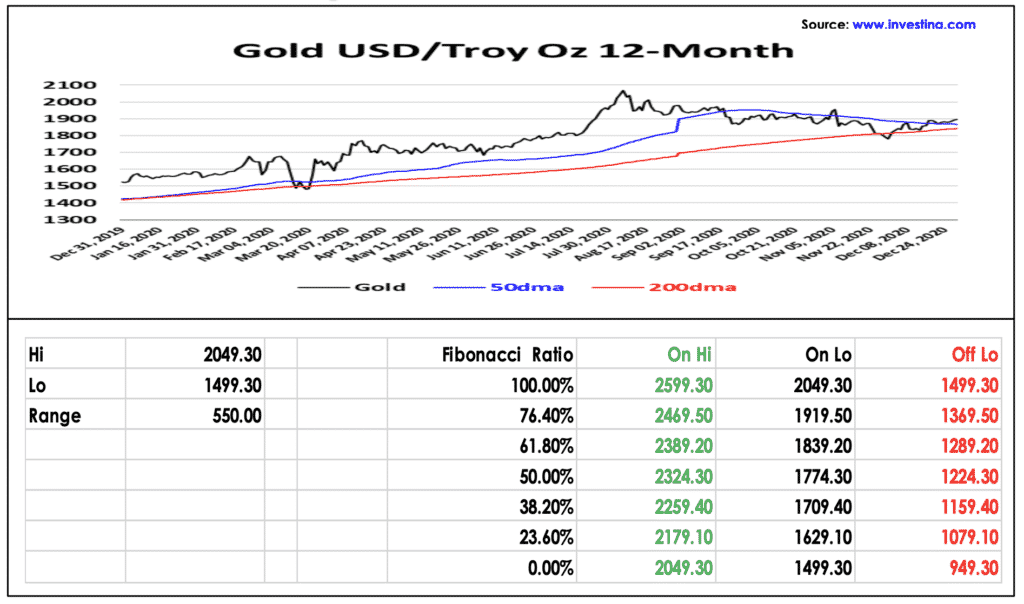

Gold USD/Troy Oz:

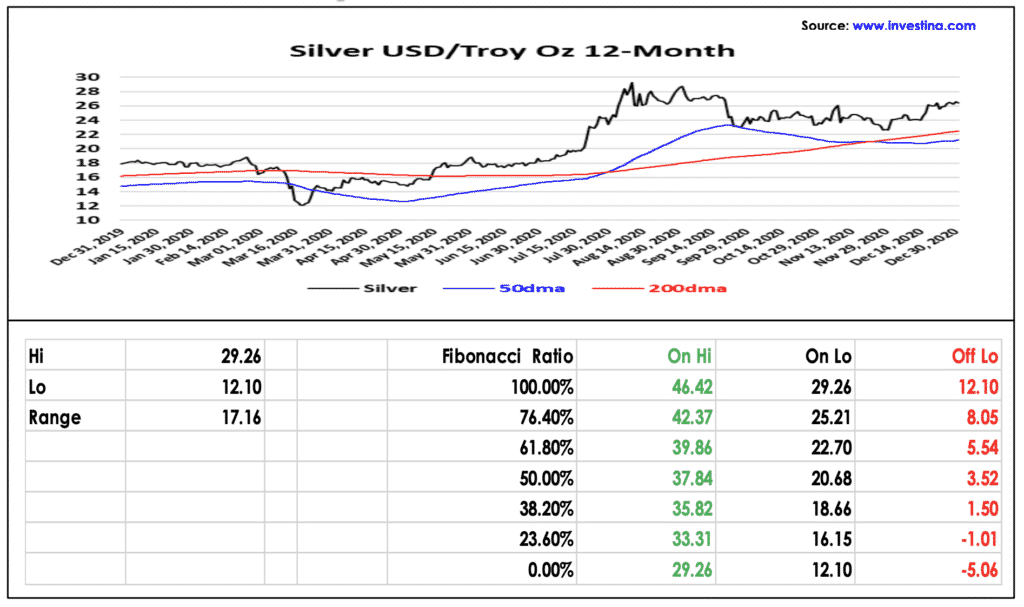

Silver USD/Troy Oz:

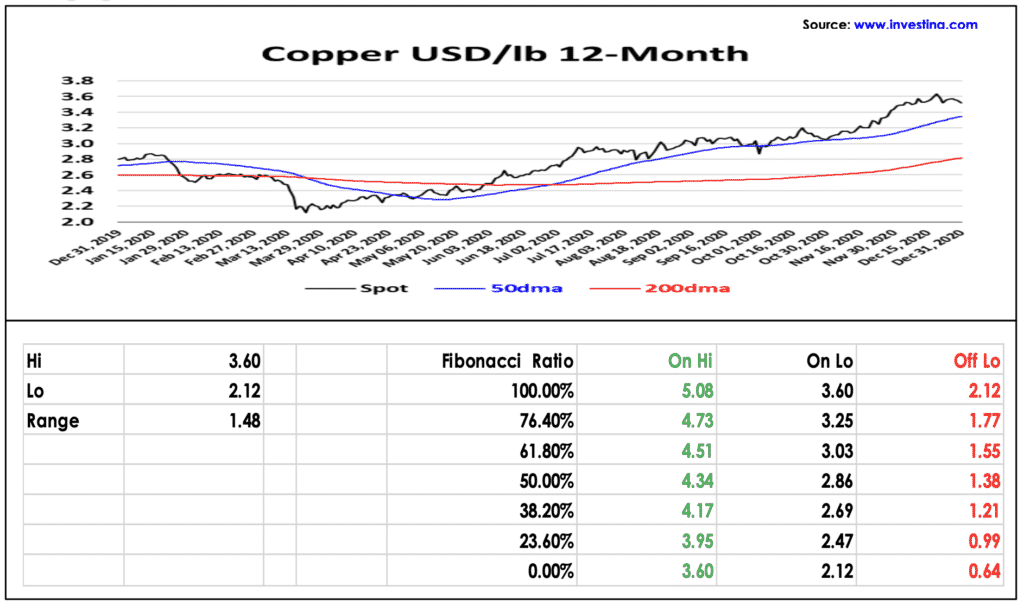

Copper USD/lb:

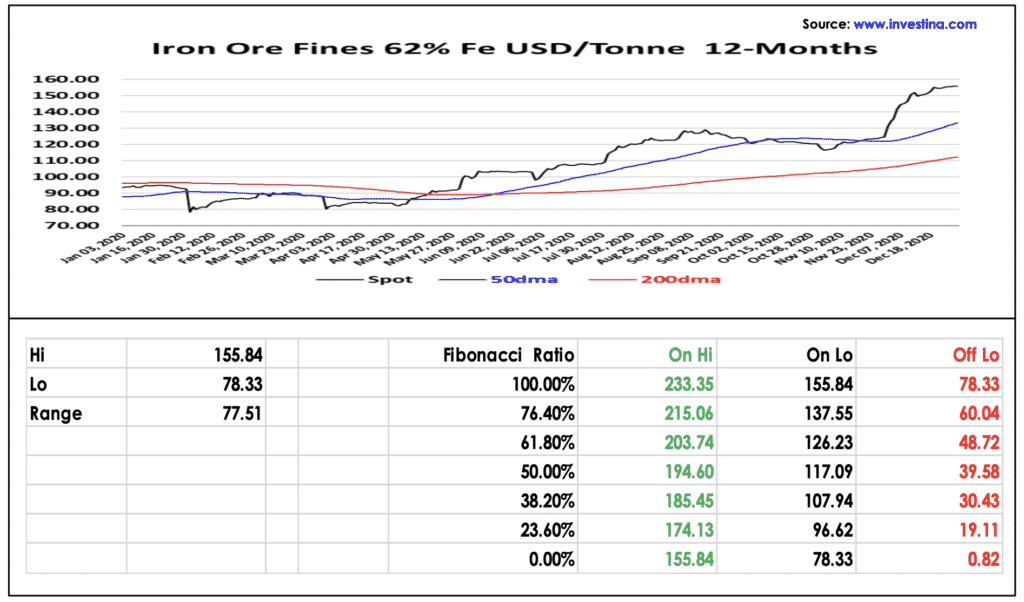

Iron Ore Fines 62% Fe USD/Tonne:

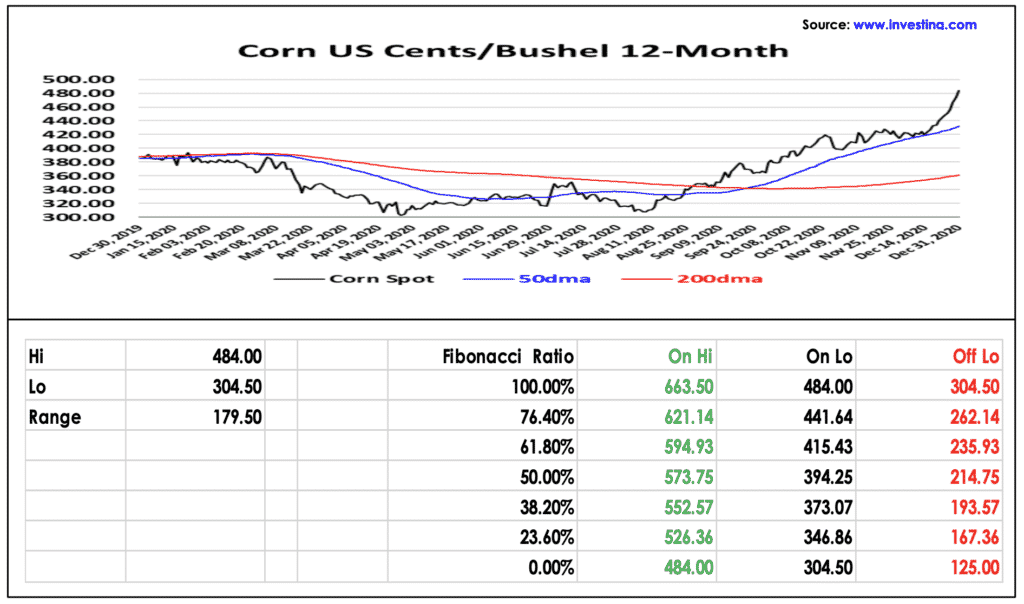

Grains…Corn USD/Bushel:

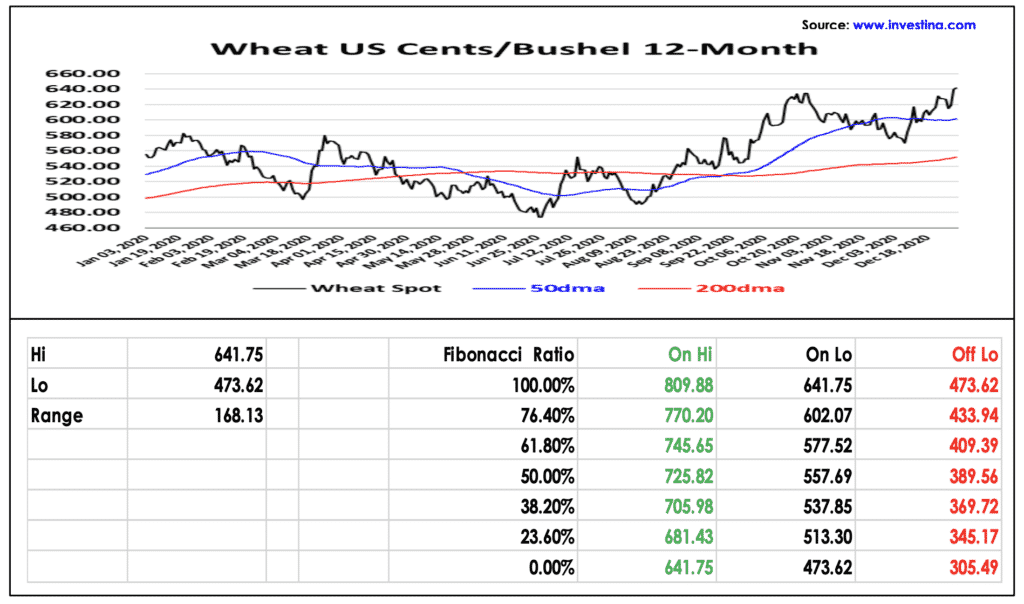

Grains…Wheat USD/Bushel:

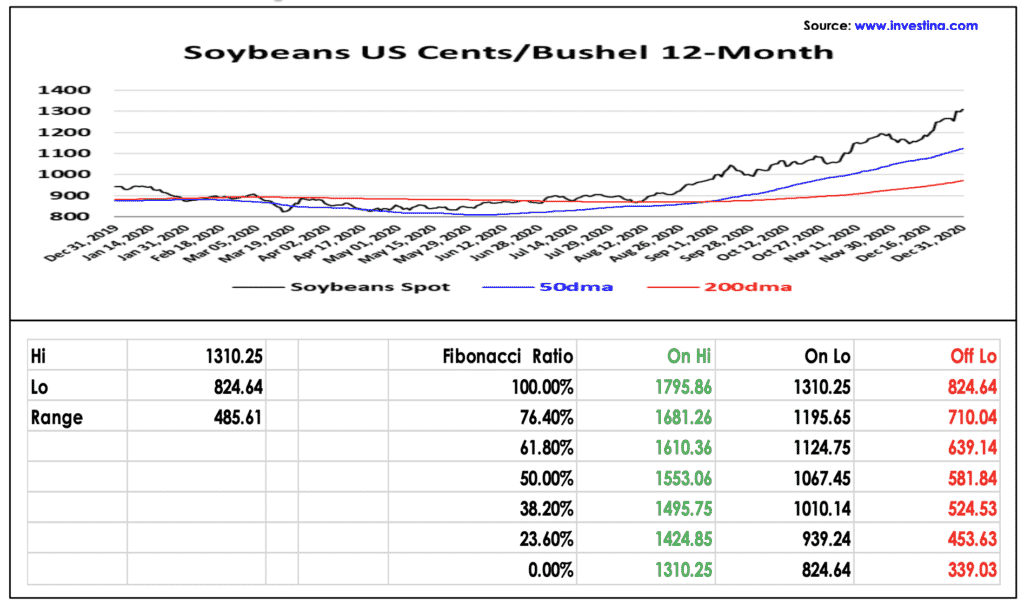

Grains…Soybeans USD/Bushel:

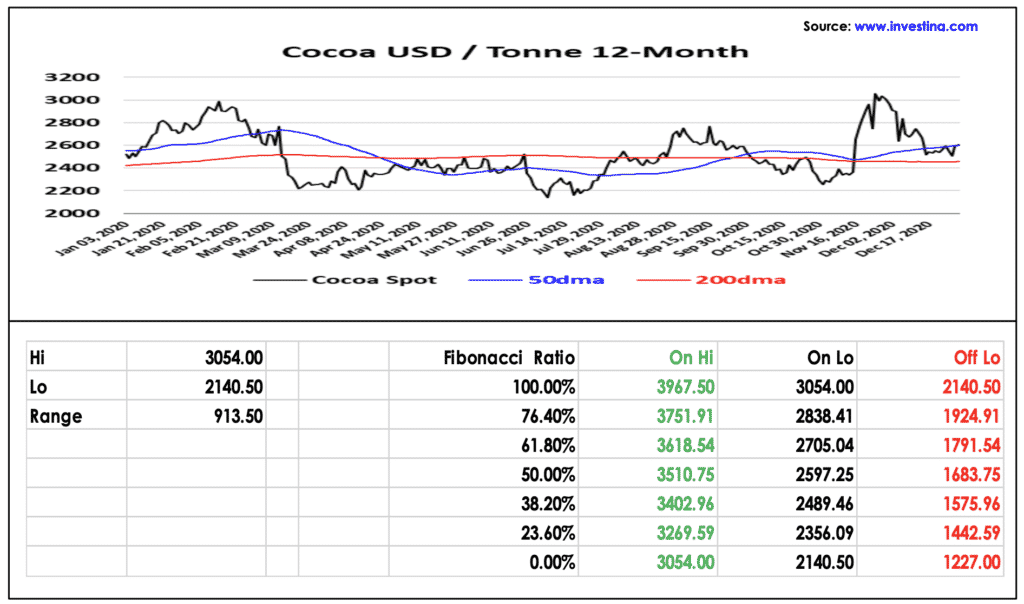

Soft…Cocoa USD/Tonne:

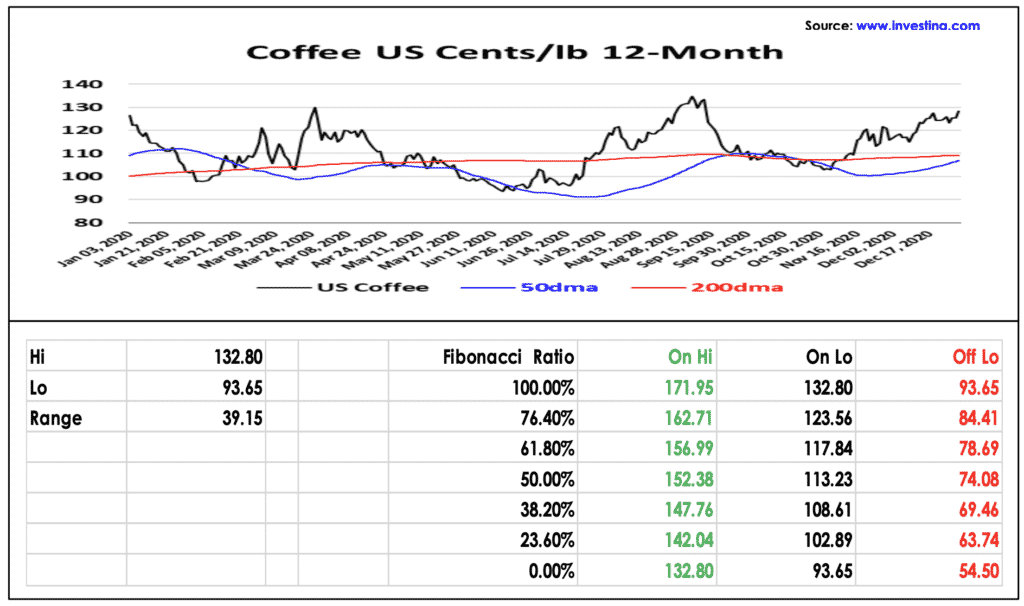

Soft…Coffee USD/lb:

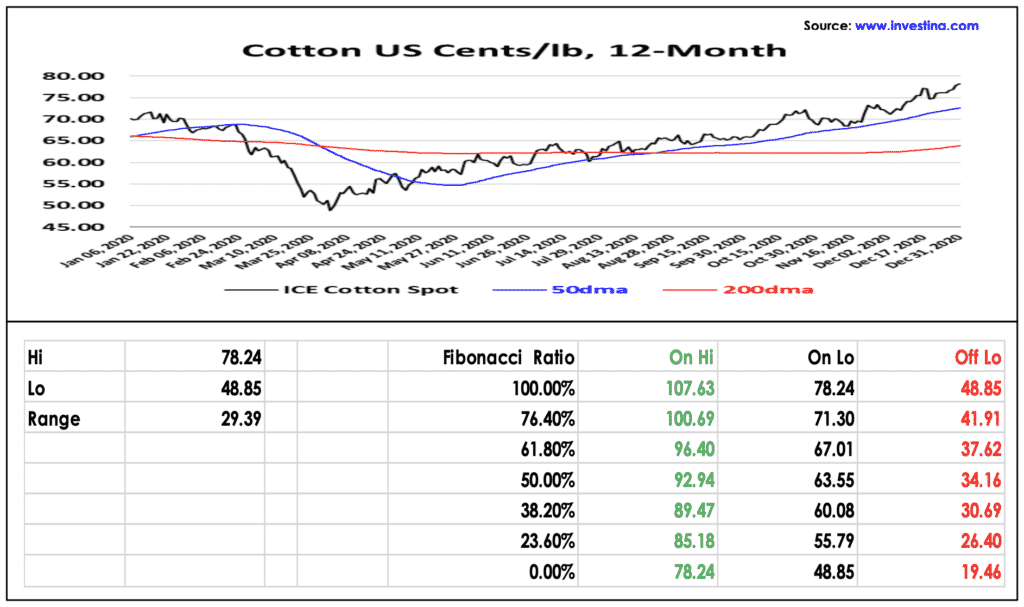

Soft…Cotton USD/lb:

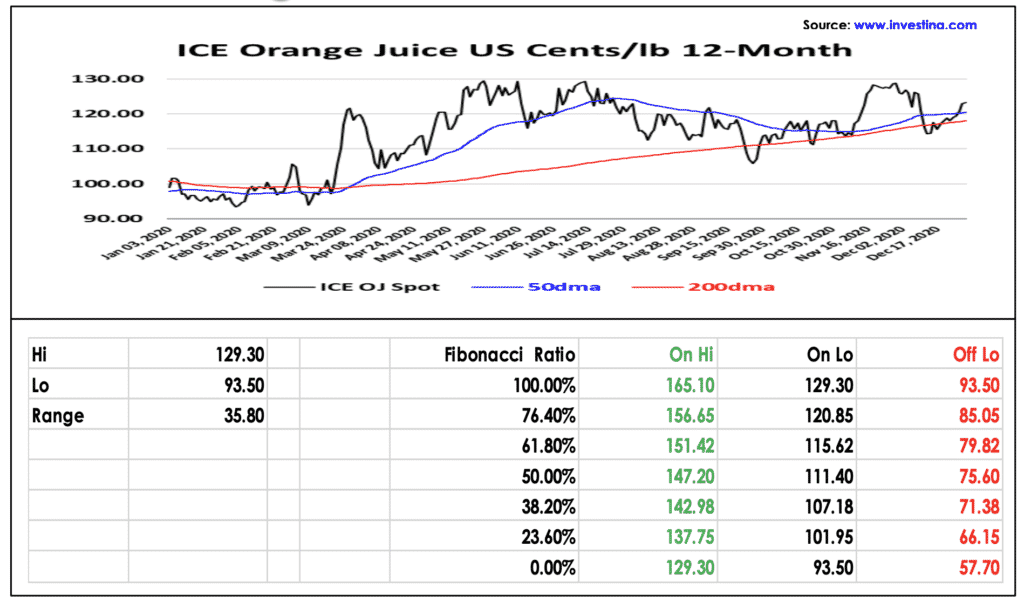

Soft…Orange Juice Concentrate USD/lb:

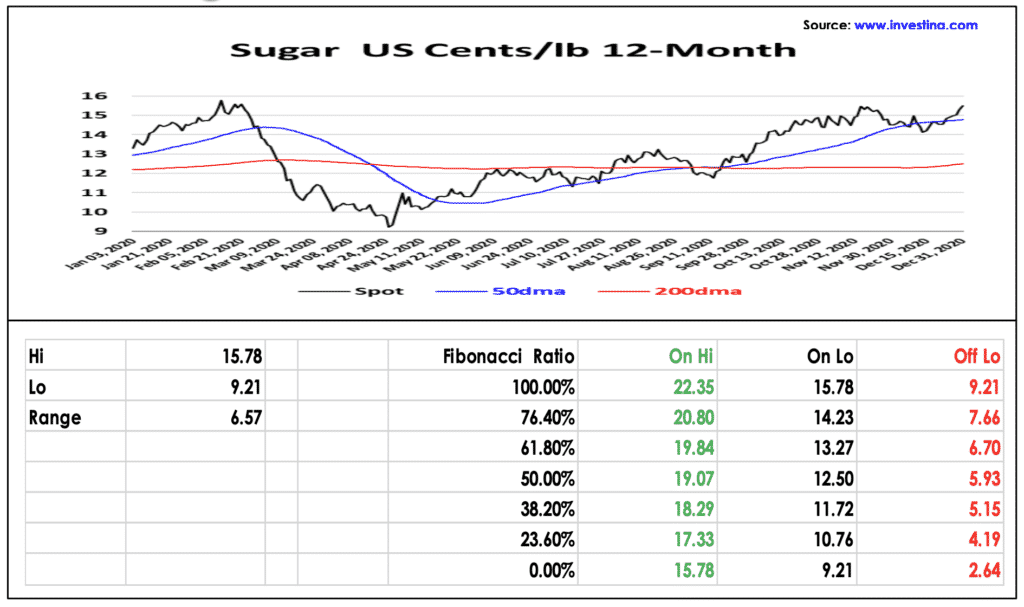

Soft…Sugar USD/lb:

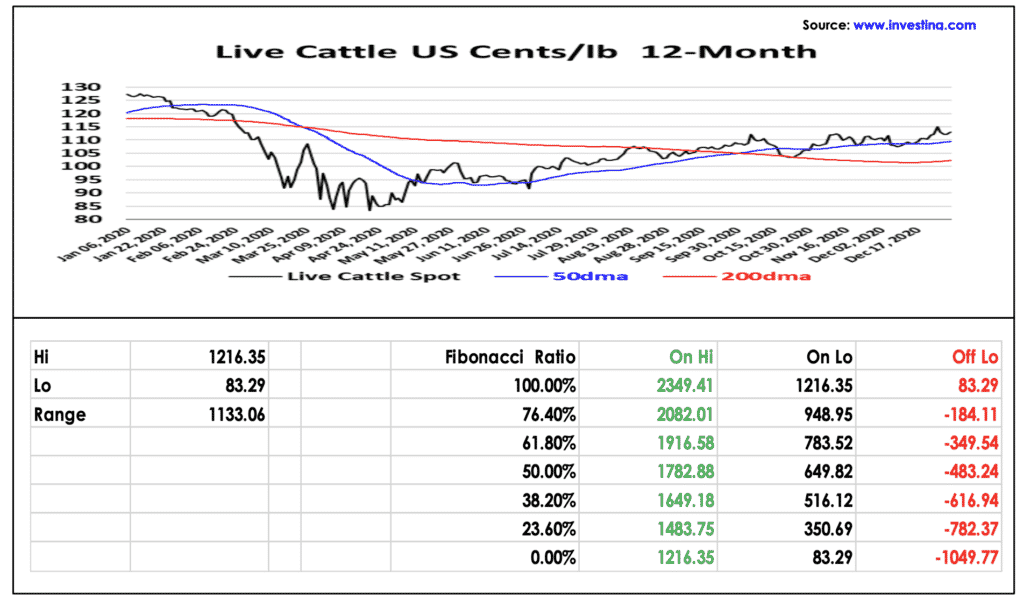

Meat…Live Cattle USD/lb: