Anyone long of EUR has had a bit of a rough ride since the European Central Bank meeting at the end of July. Christine Lagarde shifted from a decisively hawkish position in the previous meeting to one of considerable uncertainty. The EUR was hit hard on its major crosses. However, with an unexpected upside surprise in flash GDP and inflation still stubborn, I’m looking at whether or not the recent weakness might represent an opportunity.

- A dovish shift in stance by the ECB

- Although Q2 Flash GDP and stubborn inflation will likely lead to another ECB hike in September

- EUR is finding some respite on its crosses but is struggling against a resurgent USD

A dovish shift from the ECB

As central banks move towards the end of their monetary policy tightening cycles, it is natural that they should become more mindful of the data. Fed Chair Powell stressed the need for data dependence at the FOMC meeting last week. Less than a day later, ECB President Christine Lagarde showed that the Governing Council is not simply on auto-pilot anymore.

With the Eurozone suffering from weakening activity data, Lagarde said:

“The September meeting will be deliberately data-dependent”

Rate hikes have been an absolute given until now. Moving into the July meeting, expectations had been for another two hikes, at least. Now, the potential is that the ECB could do anything in September. The ECB is still worried about inflation and still wants to see it lower, suggesting that there could yet be more hikes on the way. A pause in September is possible, but one more hike before the end of the year is also still likely. However, a sense of uncertainty has now taken over ECB expectations. It means that the EUR is likely to be far more volatile around data releases now.

An upside surprise in flash GDP and stubborn inflation

The data this week will only add to the sense of uncertainty. Flash GDP for Q2 posted an upside surprise, with growth turning (marginally) positive again. This ends two quarters of negative (Q4 2022) or stagnant (Q1 2023) activity. Whilst the GDP figure of +0.3% beat expectations (of +0.2%) it masked a big disparity, with an outsized contribution from Ireland skewing the data somewhat.

The growth numbers do not hide the continued negative trends in the PMI surveys, which are in contraction. The Final Eurozone Manufacturing PMI has been confirmed as being in deep contraction at 42.7 along with a deteriorating services PMI too. The ECB will be looking at these numbers with considerable concern.

However, the ECB also needs to balance out this view with the continued stubbornly high inflation. Flash core inflation stayed at 5.5% in July which was a touch higher than the expected slip to 5.4%. The Governing Council will also be concerned that services inflation also continues to trend higher amid elevated wage costs. The ECB will be casting a concerning eye across the Channel to the impact that wage growth has had on keeping UK inflation high. This will keep the pressure on the ECB to hike once more. A September is still a distinct possibility even with a data-dependent ECB.

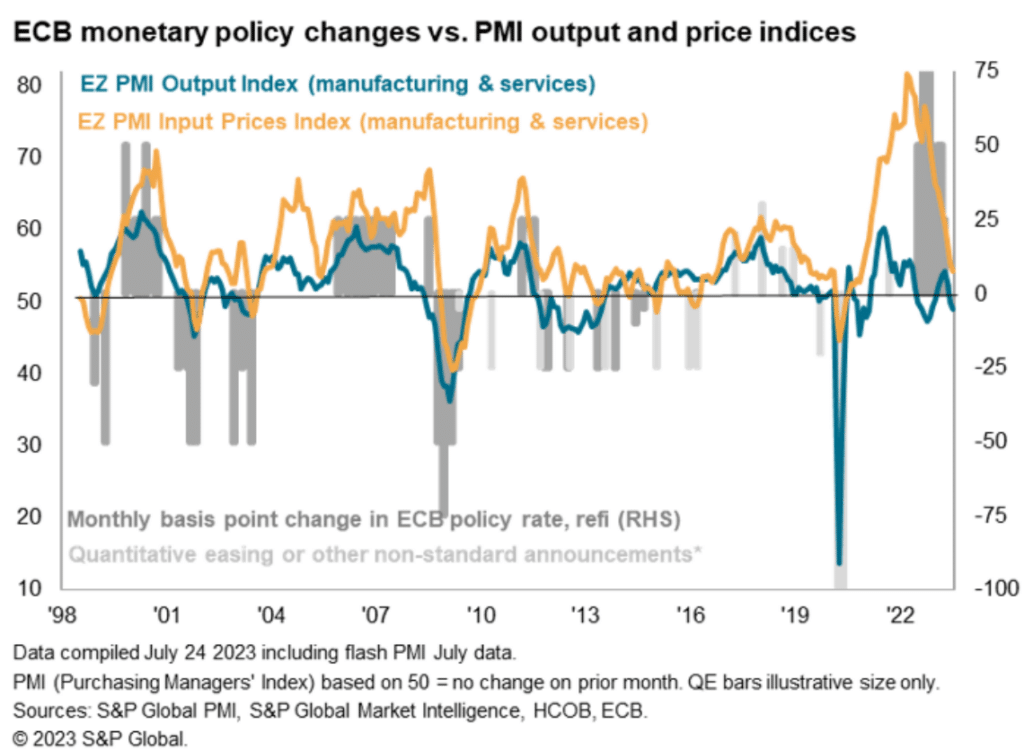

This chart from S&P Global shows how the rate hikes have helped to bring input prices lower, but also will be weighing on economic activity too. It is a fine balance that the ECB has to play now.

A choppy period for EUR crosses

The strong performance that the EUR found in the early weeks of July has been decisively unwound now. A resurgence in the USD has been a key factor behind this (other major currencies have also corrected) but the ECB meeting further weighed on the EUR. However, since then, the data this week has had a stabilising impact on EUR performance. Looking at the technical analysis of EUR major crosses, whilst the strengthening USD may still be a key factor, elsewhere there could be signs of support for the EUR again.

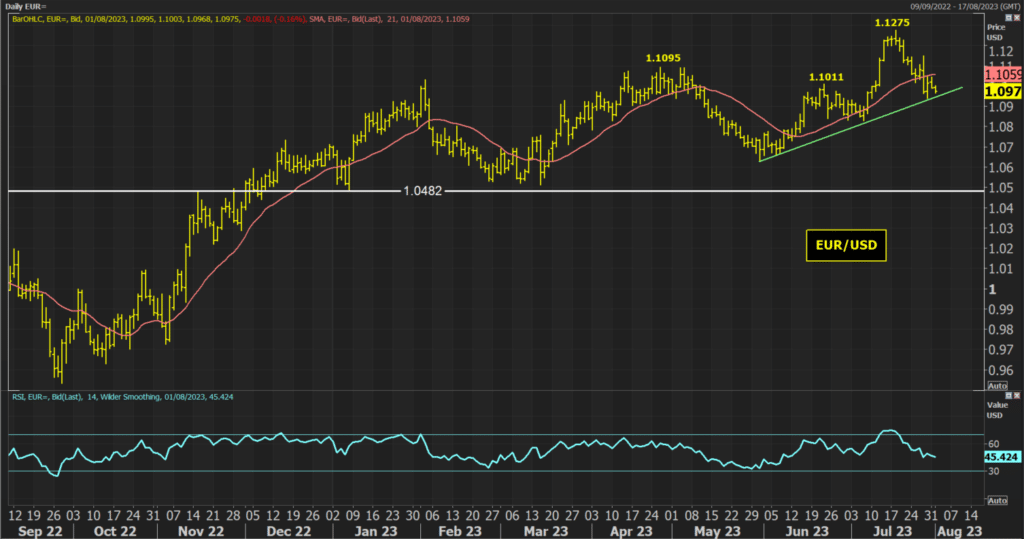

Starting with the chart of EUR/USD. There has been a decisive retracement in the past two weeks. This move has gone further than the bulls will have hoped in breaking back below 1.1011. The pair is now at a crucial moment. As the USD has strengthened once more today, as the price has dropped back a move below 1.0942 (last week’s low) would break a two-month uptrend and confirm that the pair is once more in a mixed outlook. Posting a lower high at 1.1149 has added downside pressure, as has the RSI dropping below 50. It seems that, for now, the USD rally could be set to continue dragging EUR/USD lower.

However, looking at other EUR crosses, the news is looking more encouraging. EUR/AUD is testing key resistance at 1.6515/1.6602, whilst EUR/JPY has also rebounded strongly in the past couple of sessions. However, I thought I would focus on developments in the EUR/GBP cross.

With EUR/GBP there is beginning to look a more encouraging picture. There has been a key floor that has developed in recent months. This floor is essentially a long-term trading range support, between 0.8500/0.8570. Although the market is currently in a downtrend channel, the range support has been firming in the past few weeks. The firming of this support comes also with improving momentum. No longer is the RSI pushing below 30, it is now holding lows around 35/40. This suggests there is a subtle shift in the mindset of traders.

With downside potential seemingly limited and a more neutral configuration forming in momentum, this suggests another mean reversion within the trading range. If so, there could be an opportunity to buy for another test of the 0.8701/0.8734 key mid-range resistance.