There has been a shift in sentiment in recent weeks. After having rallied consistently for over four months, US index futures have turned lower. Previously, unwinding moves were seen as a chance to buy. However, we are increasingly now seeing rallies used as an opportunity to sell. The corrective forces are mounting, both fundamentally and technically.

- A souring of sentiment with China property woes and the Fed signalling that it is not finished hiking rates

- Bond yields are sharply higher

- Selling pressure is mounting on US index futures, especially in the e-mini NASDAQ 100 futures

Corrective forces are mounting

There has been mounting negative pressure on sentiment in recent weeks. There could be an element of thinned holiday markets at play here, but the negative pressure is dragging index futures lower.

There are growing fears about financial contagion in China. The shadown banking system is creaking as a property slump has spread across the housing market. Many of the funds are backed by real estate projects linked to struggling developers. Liquidity problems means that some wealth management companies are facing issues over missing bond payments and paying back maturing debt.

The People’s Bank of China surprised markets by cutting the one-year medium-term lending facility rate by -15 basis points to 2.50%. This reflects the concern that policymakers in China are now facing. Chinese equities have fallen by around -4% in August, with the Chinese yuan losing -2.7% of its value against the USD. However, it is the impact on broader market confidence. Treasury Secretary Yellen has said that the slowdown in China was a “risk factor” for the US economy.

The concerns that traders are having as they look towards China have also been added to the minutes of the July FOMC meeting. The minutes had a hawkish lean, as summed up by this.

“Most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy”

The risk that the Fed may still yet have another 25bps rate hike in the locker is impacting major markets. Interest rate futures are rising, whilst bond yields are also continuing to move decisively higher.

Higher yields are negative for sentiment

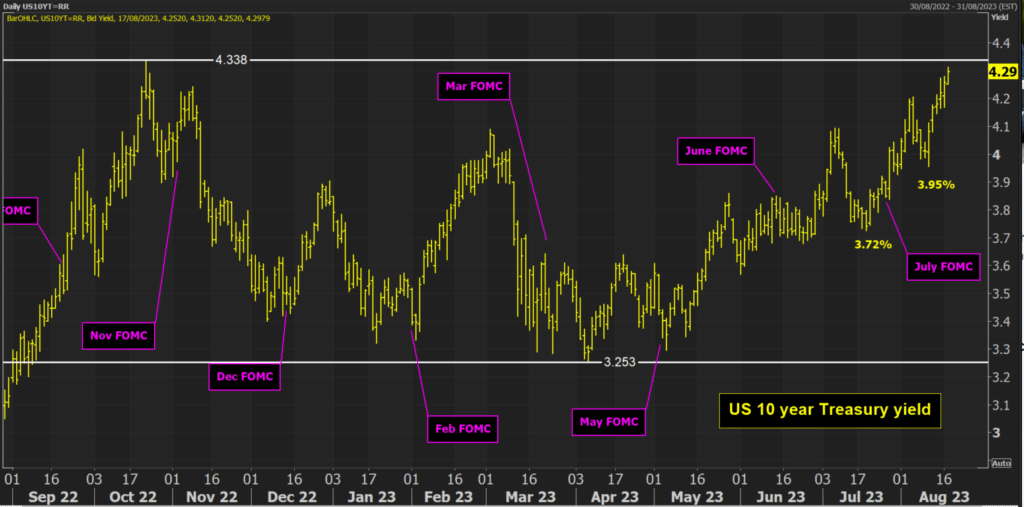

US bond yields are moving sharply higher. Whether it be due to the massive supply that the US Treasury is forcing on the market, or due to the Fed’s concerns over inflation, yields have risen decisively. However, it is a rout in longer-dated bonds that traders are concerned with. The yield on the 10-year Treasury has soared towards 4.30% in recent days. This is close to the 4.33% high from October which was the highest since 2007.

Now, it could be that this is a move towards the top of a broad trading range that the yield has been in for almost a year. However, it is also the speed of the move that will also be adding to the concern.

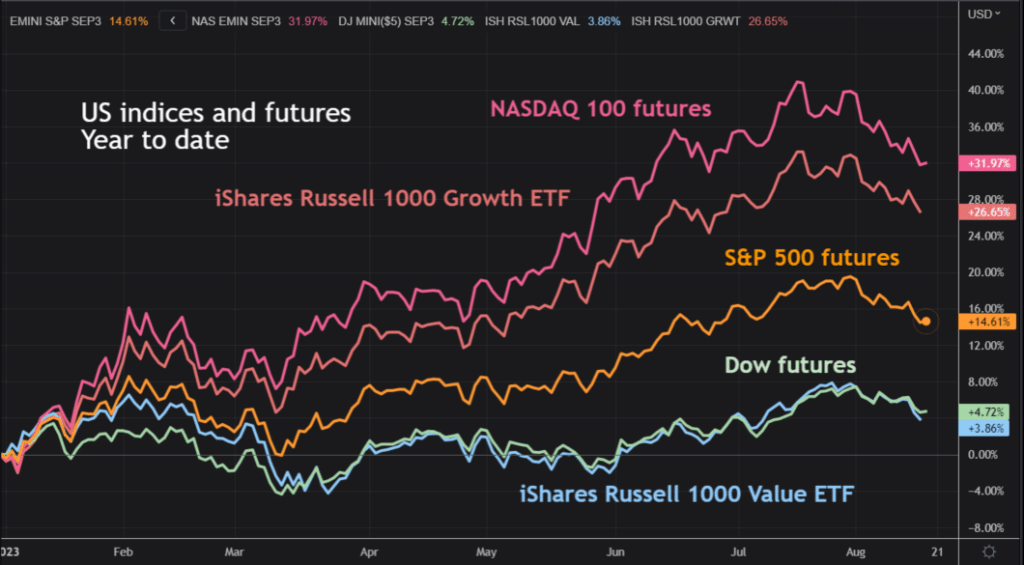

US earnings season failed to inspire buying pressure on index futures as traders have seemed to be more interested in the US data and the path of Federal Reserve interest rates. The FOMC minutes will likely mean that traders position for the prospect of rates being higher for longer, which is also a concern for equity markets. There has been a notable downturn in US equity markets over recent weeks. What is also notable is the acceleration lower in the growth segment of the market. The e-mini NASDAQ 100 futures have had a tremendous outperformance in 2023, but this is now starting to unwind fast.

Higher and rising yields tend to weigh far more on growth stocks than it does with value stocks. The Dow futures may not have experienced the pace of the rally that NASDAQ has done earlier in the year. However, Dow futures are now holding up relatively well in the face of the correction. This could be reflecting something of a sector rotation taking place amid the correction.

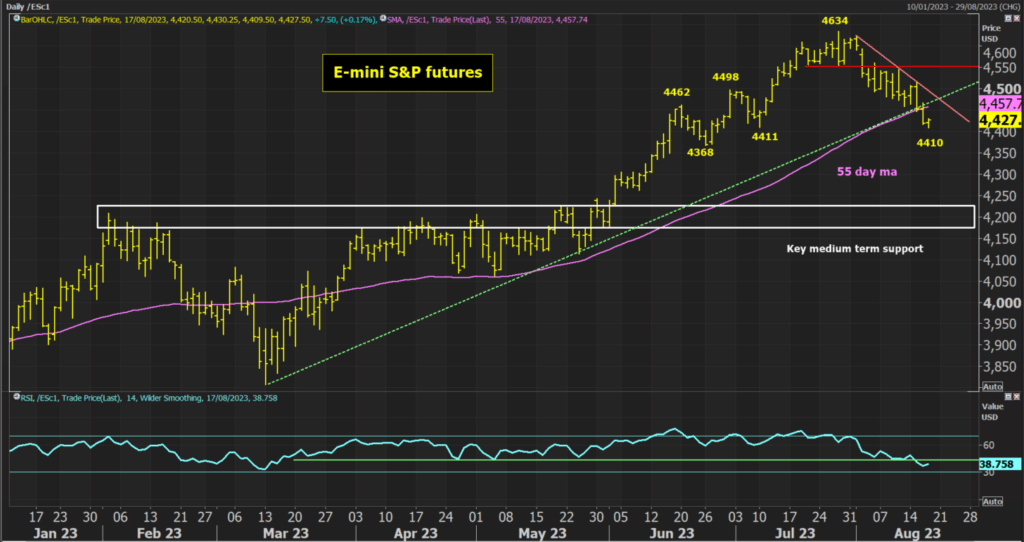

Technical indicators turn sour for e-mini S&P 500 futures

Looking at the technical analysis of the chart of the e-minis of S&P 500 futures, there is a decisive correction taking hold. If this was going to be a near-term unwind within the bull market, support would likely have formed by now. This move looks to be a much deeper correction.

The futures have now broken a five-month uptrend. The move is also below the 55-day moving average (a medium-term trend indicator). Furthermore, the daily RSI momentum indicator has moved below 40 (indicating a more corrective bias).

Breakout support at 4462/4498 has been breached and now if the futures move below the reaction lows at 4468 and 4411 it would signify the formation of a decisive new downtrend which is already starting to build.

The prospect of a deeper correction towards the key medium-term support at 4171/4227 is growing. Furthermore, the barriers to recovery are mounting, with lower highs and lower lows now forming. The first important resistance is at 4517.