It was not meant to be like this. Inflation in other countries is falling, but not in the UK. Once more, the CPI data from the Office of National Statistics has come in hot. UK CPI has come in much higher than expected as headline inflation did not fall, whilst core inflation increased sharply. The problems are racking up for the hapless Bank of England, opening the door wide open for a 50bps hike in rates tomorrow. This is driving a counter-intuitive move on GBP, at least initially.

- UK May CPI comes in much higher than expected

- The pressure on the Bank of England grows

- GBP rally loses its way as EUR/GBP picks up

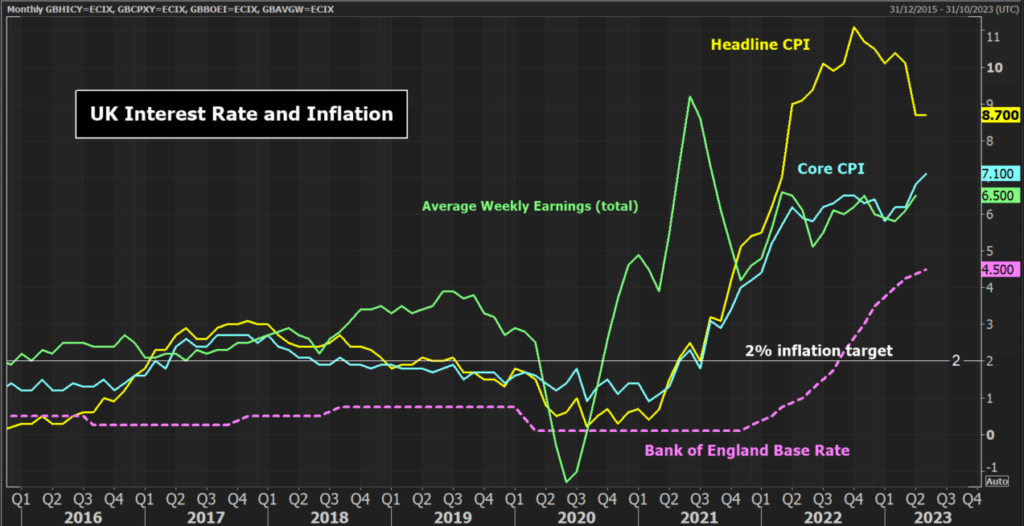

UK inflation continues to climb

As the summer months roll around, UK inflation is stubborn, sticky, and some might even say hot. Today’s CPI data makes for grim reading for the Bank of England, anyone that has a mortgage and, well, anyone that has to spend money to buy anything.

- UK CPI increased by +0.7% in May, meaning that year-on-year inflation is still where it was in April, at 8.7% (consensus had forecast a decline to 8.4%).

- UK Core CPI increased by +0.8% in May with year-on-year increasing to 7.1% (from 6.8% in April, versus a consensus of 6.8%).

Core inflation is at its highest level since May 1992, over 30 years ago!

According to the ONS, air travel recreational and cultural goods and services and second-hand cars contributed to the largest upward contributions. Services inflation remains a key problem, increasing from 6.9% in April to 7.4% in May. This will be a key concern for the Bank of England.

If there are any crumbs of comfort in the data today, they are very hard to find. Food inflation has dropped back a shade from 19.1% to 18.4% (I know, I am trying here). Also, headline inflation fell month on month to 0.7% from 1.2% in April. However, there is more encouraging news in the PPI data which has fallen more than expected today. This may begin to see through into lower goods inflation in the coming months but may take less time to affect services inflation.

Headline CPI inflation should fall next month, with strong comparatives of June 2022 dropping out. However, the concern is that monthly core inflation has been much stronger in the past five months than at any time in the past year. Core inflation has no favourable comparatives to help year-on-year inflation fall. Core CPI will remain very sticky and could perhaps even continue to rise in the coming months.

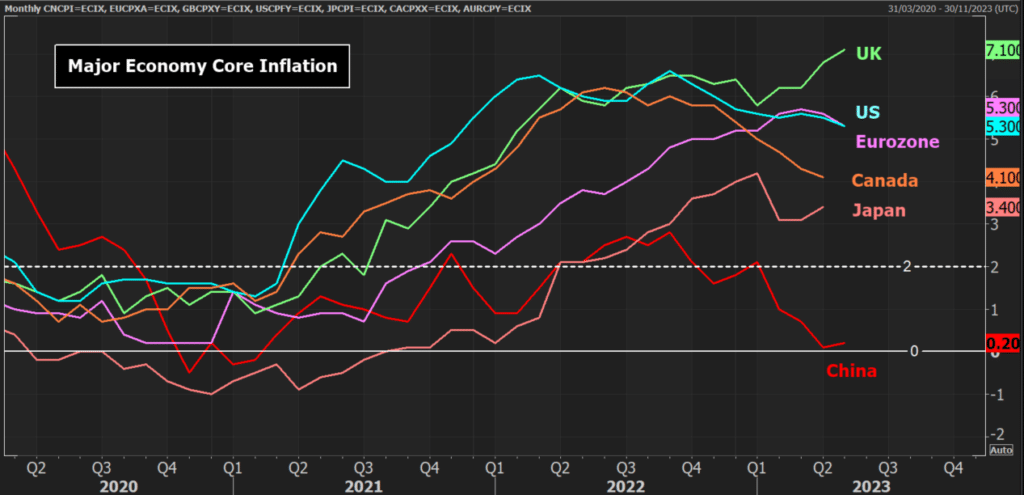

On 12-month data, around the turn of the year, it was looking as though inflation was beginning to fall away. However, the tide has turned again and year-on-year core inflation has not fallen now for four months. This comes at a time when other countries such as the US, Canada and the Eurozone are seeing trends lower in core inflation (even if the path is slightly more sticky than had been hoped).

Pressure ratchets up on the Bank of England

The Bank of England has been raising rates since December 2021. However, it has always seemed to be playing catch up on core inflation that had risen above the 2% target at least six months before then. The BoE has since been chasing its tail in hiking rates and has never managed to get on top of the inflation problem.

Inflation continues to come in hot and the Bank of England will need to continue to increase interest rates, perhaps far beyond where they are now. Interest rate futures are pricing for the Bank of England rates to be peaking above 6.00%, which is a full six more rate hikes from the current 4.50%. The consensus for tomorrow’s rate hike is for a 25bps hike, but given this is the second consecutive inflation print that has been much higher than expected, the risk is surely for a more aggressive 50bps hike.

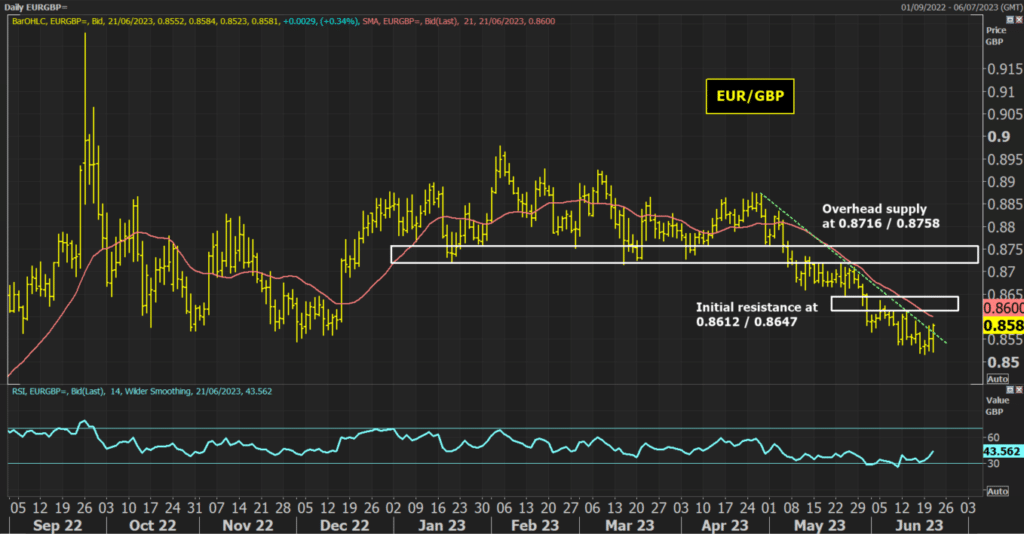

GBP wobbles see EUR/GBP moving higher

GBP has been a consistent outperformer on major forex for several months. However, the early reaction to this higher inflation has not driven the gains perhaps that would have been expected from the prospect of interest rates still with much higher to go.

Looking at the technical analysis, there has been a mixed reaction on GBP crosses. GBP/USD has dropped in a continuation of a minor USD rebound that has been seen across major currencies. However, GBP is also sliding against the EUR, with a rebound in the EUR/GBP pair. The only pair to see a GBP-positive move is against the perennial underperformer of the JPY.

From a technical perspective, I have been interested in the decline in EUR/GBP for a while, exacerbated by the recent strong UK wage growth. The trend lower over the past couple of months has been consistently breaking supports. However, this morning we have seen an intraday breach of a seven-week downtrend. For now, this may just be a minor unwind, with the Relative Strength Index still under 50, but with a closing break of the uptrend and still room for the unwind to take hold, this near-term move could progress.

The reaction to initial resistance at 0.8612/0.8647 will be an important gauge for the near to medium-term outlook. It will be interesting to see if this move against GBP holds. A bull failure around the resistance would once more encourage the EUR/GBP sellers to regain control and retest 0.8517.