Macroeconomic/ geopolitical developments

- Although the FOMC meeting minutes on Wednesday did indicate that bond purchase tapering is likely to begin before the end of 2021, the minutes also revealed that Fed officials are currently looking to keep interest rates at or near zero for the next couple of years.

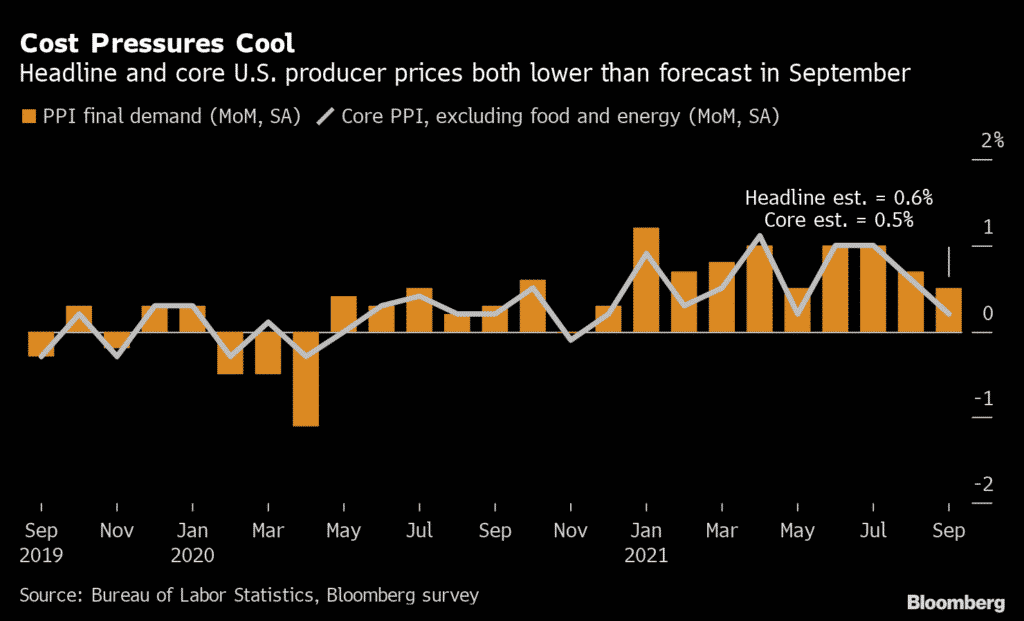

- Data has suggested that both supply pressures and inflation might be peaking, with the US PPI data coming in at less than consensus.

- In addition, the White House announced measures to relieve the congestion at ports.

- Earnings season kicked off in the US last week, with solid results from the financial sector, particularly JP Morgan, Bank of America, Wells Fargo, Morgan Stanley, Citigroup, and Goldman Sachs.

- This helped broader stock indices in the US and globally higher in the second half of the week.

- These factors above combined to reinforce the renewal of a “risk on” theme seen across global financial markets from the middle of last week, undoing much of the “risk off” sentiment seen in September.

Global financial market developments

- Global shares indices advance further into mid-October to undo the significant September sell off.

- US yields corrected lower last week but then reversed Friday towards higher yield territory, reinforcing higher yield moves evident since the September Federal Open Market Committee (FOMC) meeting.

- The US Dollar dipped lower last week but stays firm after gains seen since September with rising US yields.

- With the higher US yields and higher Oil price, USDJPY surged to its highest level since April 2019.

- EURUSD consolidated but remains vulnerable to further losses.

- GBPUSD posted a solid rebound and now indicates an upside bias

- Gold posted a recovery and a setback, leaving a broader sideways, range theme.

- Oil extended its strong advance from August, now comfortably above $80.

- Copper surged higher last week to its highest level since May, breaking out from the sideways range.

Key this week

- Geopolitics: Still watching Congressional discussions regarding raising the federal debt limit.

- Central Bank Watch: TheReserve Bank of Australia (RBA) Meeting Minutes meeting minutes are released on Tuesday.

- Macroeconomic data: The data standouts this week are Chinese GDP, plus Retail Sales from China and the UK, CPI data from Canada and the UK and probably of greatest significance the global Markit Flash PMIs, which are released on Friday.

- Microeconomic data: Earnings season continues in the US with J&J, Netflix, Tesla, ASML, PayPal, and Intel the standouts.

| Date | Key Macroeconomic Events |

| 18/10/21 | China GDP, Retail Sales and Industrial Production |

| 19/10/21 | RBA Meeting Minutes |

| 20/10/21 | UK inflation report (including CPI); Canadian CPI |

| 21/10/21 | US Jobless Claims |

| 22/10/21 | UK Retail Sales; global Markit Flash PMIs; Canadian Retail Sales |