After the Reserve Bank of Australia hiked unexpectedly on Tuesday, the Federal Reserve and the European Central Bank (ECB) made it a hat-trick of 25 basis points of rate hikes in the past 24 hours. Whilst the caution and pausing signals from the Fed were broadly anticipated, the admission of the negative impact of monetary policy tightening from the ECB is new. Markets are reacting.

- The Fed is now on pause but inflation remains a problem

- The ECB is tightening but admits it has concerns about tightening

- A weakening USD, gold is higher but equities also fall back

- A cautious ECB may now weigh on the EUR

A pause in tightening, but who will blink first, the markets or the Fed?

As the dust begins to settle on the FOMC decision, there are a few key points to consider.

- The Fed is on pause, but in reality, is done hiking

All signals that can be taken from the FOMC statement and Powell’s press conference suggest that the Fed has finished its tightening in this cycle. The bit on “some additional policy tightening may be appropriate” was removed from the statement. However, this was the main bit that reflected the caution:

“…the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

- Powell says that he is still worried about inflation

However, this does not mean rate cuts are happening. Or at least this is what Powell wants markets to buy into. He said a couple of things in the press conference that certainly suggested that the FOMC was not going to pre-commit to rate cuts.

“We on the committee have a view that inflation is going to come down—not so quickly, it will take some time.”

He went on to add:

“In that world, if that forecast is broadly right, it would not be appropriate to cut rates.”

The FOMC is worried about inflation. However, inflation is tracking decisively lower in the US, perhaps not as quickly as ideally hoped, but it is reducing. It would suggest that inflation would need to fall more rapidly in the coming months for the Fed to cut rates in the next few meetings.

This part of the press conference had more of a feel of Powell trying to tough talk on inflation. Well, with core CPI inflation ticking up to 5.6% recently and holding decisively above the Fed Funds rate, this is what he had to do. Even if the Fed is more cautious about the economy now.

Furthermore, history tells us that on average the Fed cuts around six months after the last hike. But that is not when there is a banking crisis rumbling on and a developing recession. I prefer to follow the market positioning here.

- This leaves a Mexican stand-off with markets pricing for cuts

This tough talk on inflation is arguably what accounted for the sharp fall back on US equity markets last night (see below). However, it leaves the FOMC at odds with where the market sees the situation. They are now in a bit of a Mexican stand-off.

Interest futures are taking a pause and running away with rate cuts this year. Fed funds futures are pricing more than -50 basis points of cuts before the year end, with the first rate cut potentially as soon as September.

This leaves the message in the June meeting (and the dot plots) as being potentially significant market-moving factors.

- The key takeaway: Powell is talking a good game on inflation but cuts are coming. This will continue to subdue the USD.

ECB also looks more cautious about the impact of tightening

Turning to today’s ECB meeting we also see a central bank tightening rates but starting to sound far more cautious. A +25bps rate hike to the rates corridor means the Deposit Rate is now up to 3.25%. However, there were also hints of a blink from the ECB too.

In the ECB statement, there was a new section:

“At the same time, the past rate increases are being transmitted forcefully to euro area financing and monetary conditions, while the lags and strength of transmission to the real economy remain uncertain.”

That word “forcefully” is pretty strong. Also the uncertainty of the lags and strength of transmission. The ECB may have arrived slightly late to the tightening party, but it has still been aggressive. However, it is now starting to see the impact of this on the Eurozone economy. Lagarde noted that corporate demand for loans was “really, really down”. The tightening is certainly having an impact.

However, in her press conference, ECB President Lagarde said:

“We are not pausing”

No they are not, but this will cause markets to have a rethink about just how many further hikes may be seen. The ECB’s Desposit Rate is at 3.25% now, a hike to 4.00% looks increasingly unlikely.

In tackling the issue of unanimity of the decision she retorted:

“General, very strong consensus”

I would take it that in other words, the divisions are growing. There is probably a significant variance in opinion on the Governing Council forming.

- The key takeaway: It could now be that whilst there are more hikes to come, the EUR may begin to lose some of its outperformance from the tightening.

USD remains weak, Gold supported, Equities weakening

Markets are moving on the announcements of the two big central banks. Here is what I am seeing:

- The continuation of a weaker USD, but also potentially the build-up of resistance to further gains on the EUR

- Gold has upside potential, with weakness seen as a chance to buy

- Equities are in profit-taking mode now with a correction developing

Let’s have a look at a few charts and some quick technical analysis.

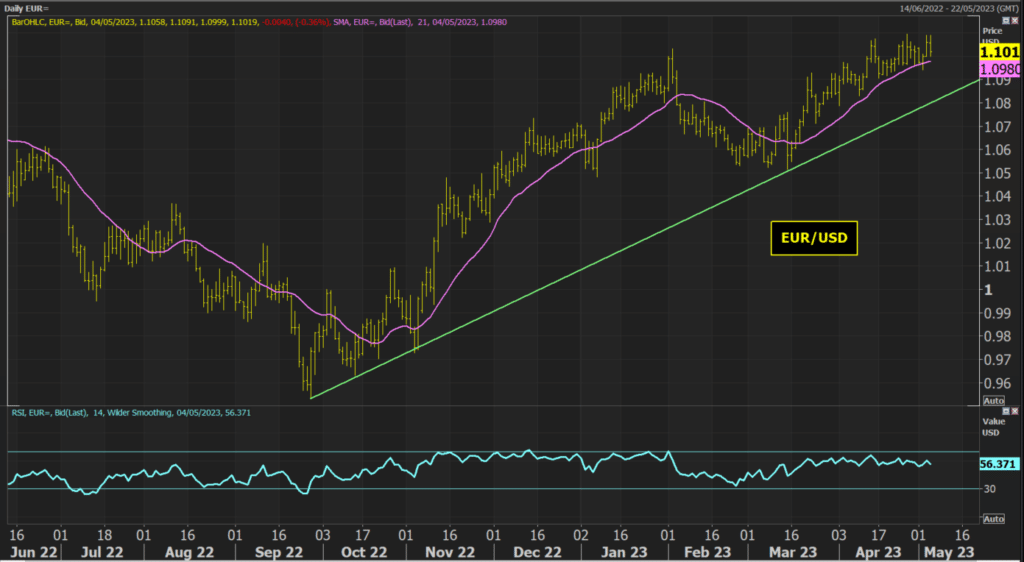

USD is still weak, but EUR may be hitting the buffers for now

Understandably, the chart of EUR/USD is the choppy market on these decisions. The market is losing the upside momentum of the bull run since March, whilst resistance at 1.1075/1.1095 is strengthening since the ECB decision today.

Technical indicators are still positive, but the move looks to be starting to run out of steam a bit. I would be more comfortable initiating long positions around the support of the seven-month uptrend (around 1.0810 currently).

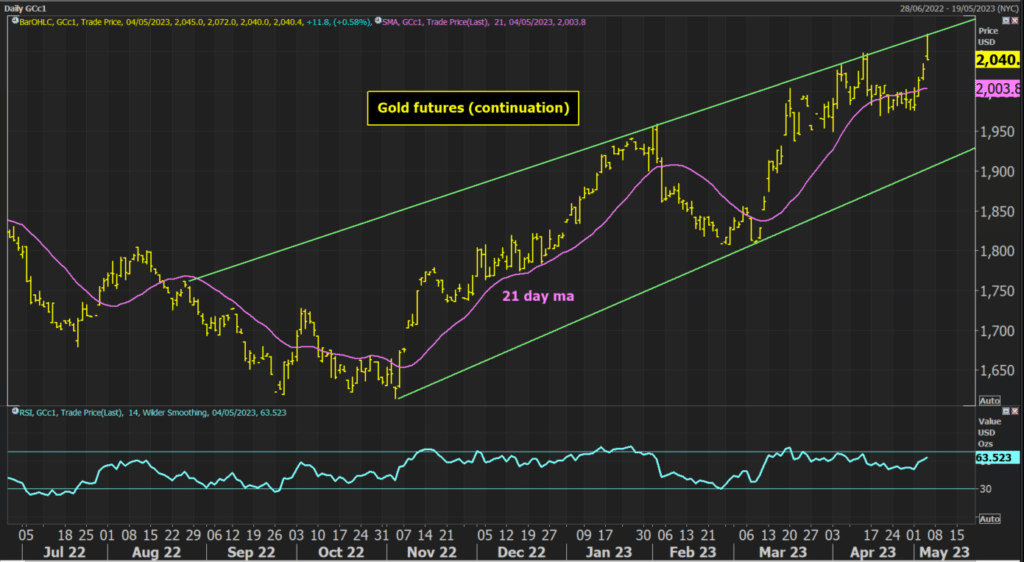

Gold futures can still retest the highs again

Gold futures hit the top of the uptrend channel again earlier today. This was bang on the all-time high from March 2022. Despite an intraday pullback, I continue to see weakness as a chance to buy.

The prospect of recession in the US, lower US interest rates and slowly falling inflation supports further gains. There is good support for a pullback towards $2000/$2005 (also the 21-day moving average).

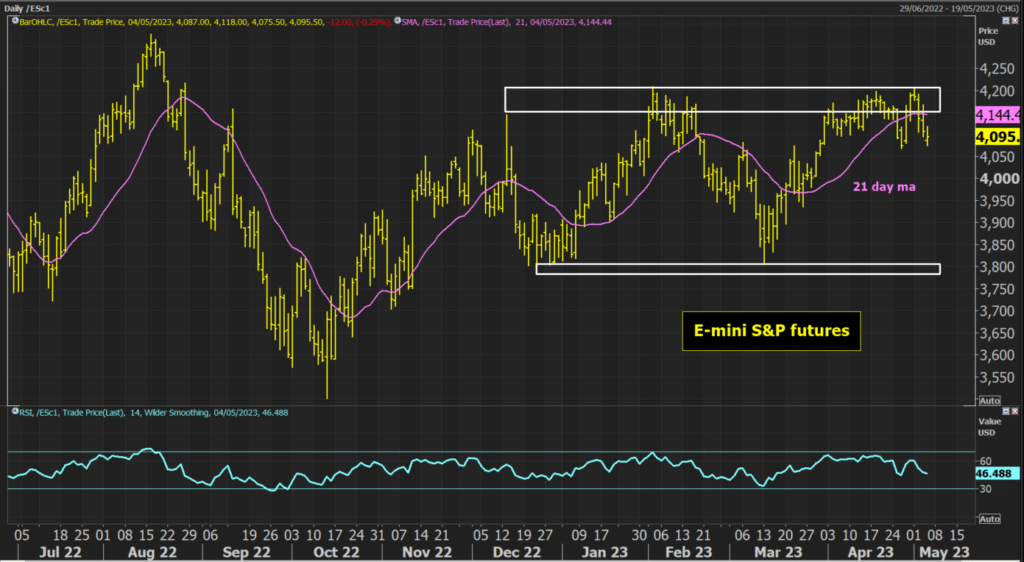

E-mini S&P 500 futures ready to pull lower

The rally on the E-mini S&P 500 futures has faltered since the Fed decision. Reaction to the key support at 4068.75 will be key.

However, with the RSI again faltering under 50 and the 21-day moving average also rolling over within the range, it seems that futures are set for another pullback within the multi-month trading range. A close below 4068.75 implies a target of the late March reaction low at 3937.