Macroeconomic/ geopolitical developments

- In various speaking engagements this past week Fed Chairman Jerome Powell has reiterated the US Central Bank’s dovish stance.

- This saw US yields (and global bonds) move back modestly to lower yield territory (from recent high yield extremes).

- The German Ifo business climate index for March posted at to 96.6 from 92.7 in February, beating analyst expectations

- The European vaccination program has resumed after some questioning of the Astra Zeneca vaccine, but continues to lag behind the rollouts in the US and the UK.

- The UK and EU seemed to have reached some agreement regarding vaccine exports and imports.

- The number of hospitalisations and deaths in the UK continues to fall, though the fall in the number of new cases seems to have bottomed.

- However, cases in some parts of Europe are still on the rise, which has seen France and Italy move to lockdowns and further restrictions in Germany.

Global financial market developments

- The global bond market sell off led by US bond markets eased last week with a move back to higher yields from multi-year yield highs.

- However, US lower yield moves are seen as corrective, whilst global yield differentials have continued to widen versus the US, seeing global bond yields moving notably lower compared to the US.

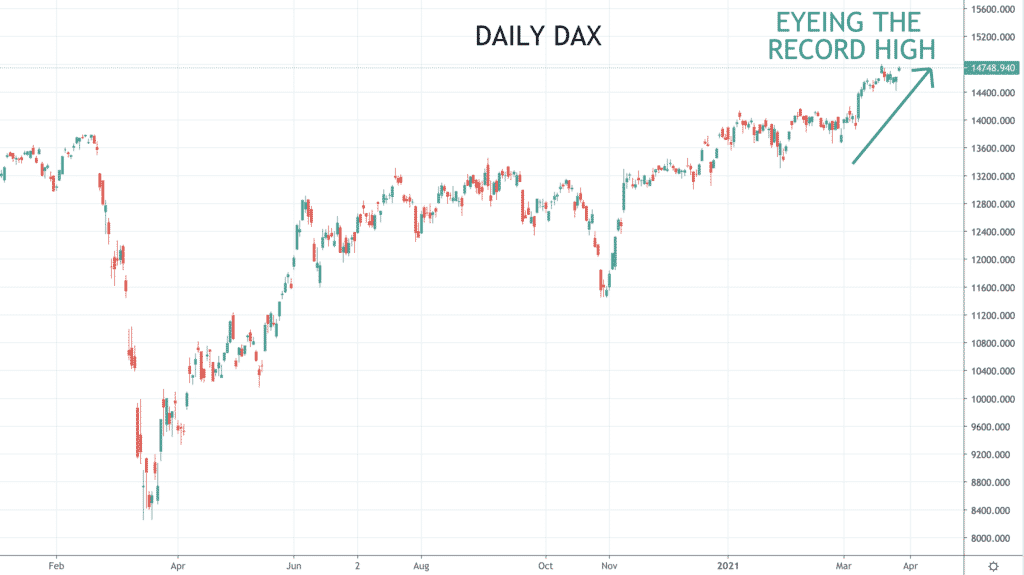

- Major global stock indices posted strong rebounds with European averages leading the way back close to record and multi-month highs (notably the DAX).

- US indices have seen a broad rally particularly at the very end of the week, with the Dow Jones Industrial Average and the S&P 500 close to new record highs.

- The Nasdaq 100 and Composite averages have tried to rebound, to try to ease the more negative themes evident through March.

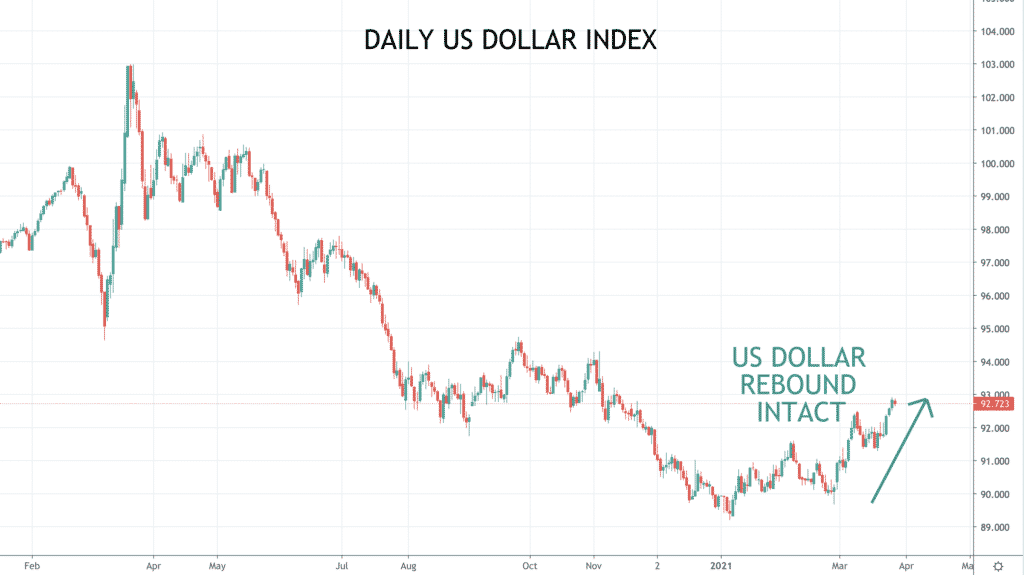

- The US Dollar has recovered after initially setting back immediately after March’s Fed announcement, renewing the positive US Dollar trend evident in 2021

- EURUSD has extended its bear theme and GBPUSD pushed lower, further correcting the 2021 bull move.

- The “risk currencies” plunged lower and then rebounded with the Australian, New Zealand and Canadian Dollars all vulnerable versus the US Dollar.

- Oil was choppy and sideways last week after the prior week saw a significant sell off, damaging the underlying theme is bullish.

- Copper has been sideways since its negative correction from a multi-year high.

- Gold has been sideway since its earlier March rebound but remains vulnerable as the US Dollar retains an underlying bull tone.

Key this week

- Geopolitics:

- Europe and the UK have switched this past weekend to Daylight Savings Time, which means the time between New York (EST) and the UK (BST) is back to 5 hours.

- Good Friday is on 2nd April 2021 with most global markets closed for the Easter holiday.

- Watching COVID-19 cases, hospitalisations and deaths globally (notably in Europe).

- Monitoring for possible new lockdown restrictions, particularly in Europe.

- Central Bank Watch:

- No Central Bank activity of note

- Macroeconomic data: Key this week will be the global Markit and US Institute of Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) reports out on Thursday and Friday’s release of the US Employment report.

| Date | Key Macroeconomic Events |

| 29/03/21 | Nothing of note |

| 30/03/21 | Japanese Employment report |

| 31/03/21 | Chinese PMI; UK Gross Domestic Product (GDP); German Employment report; EU Consumer Price Index (CPI); US ADP Employment change |

| 01/04/21 | Global Markit Manufacturing PMI; German Retail Sales; US ISM Manufacturing PMI |

| 02/04/21 | Global Good Friday holiday; US Employment report |