Here we present the Hawk / Dove sheet, an explanation of the terminology as well as the implications on forex trading and how it is used in fundamental analysis.

Hawkish and Dovish

Hawkish

A Hawk is a term originally used in economics to describe economists or Central Bankers who are more concerned with potential recession from higher inflation,, than with economic growth. It is now more commonly used, however, to describe a view on interest rates, with a hawk favouring higher (or an increase in) interest rates.

The transition mechanism is that higher interest rates make borrowing less favourable or attractive for individuals and corporates. This then leads to a decrease in spending, lower demand and price stability.

Dovish

Conversely, a Dove was originally used to describe Central Bankers or economists who are less concerned with higher inflation rates, and more focused on stimulating economic growth. It is now commonly used to describe a view on interest rates, with a dove favouring lower (or a decrease in) interest rates.

Lower interest rates encourage borrowing by corporates and individuals, which in turn encourages an increase in spending and higher demand.

FX implications

Generally, a more hawkish view expressed by a Central Banker would highlight a potential for a higher interest rate environment for that country. This would then favour an appreciation (rise) in the currency.

A dovish view expressed by a Central Banker would point to a possible lowering of interest rates, and the a likely depreciation (fall) of the currency.

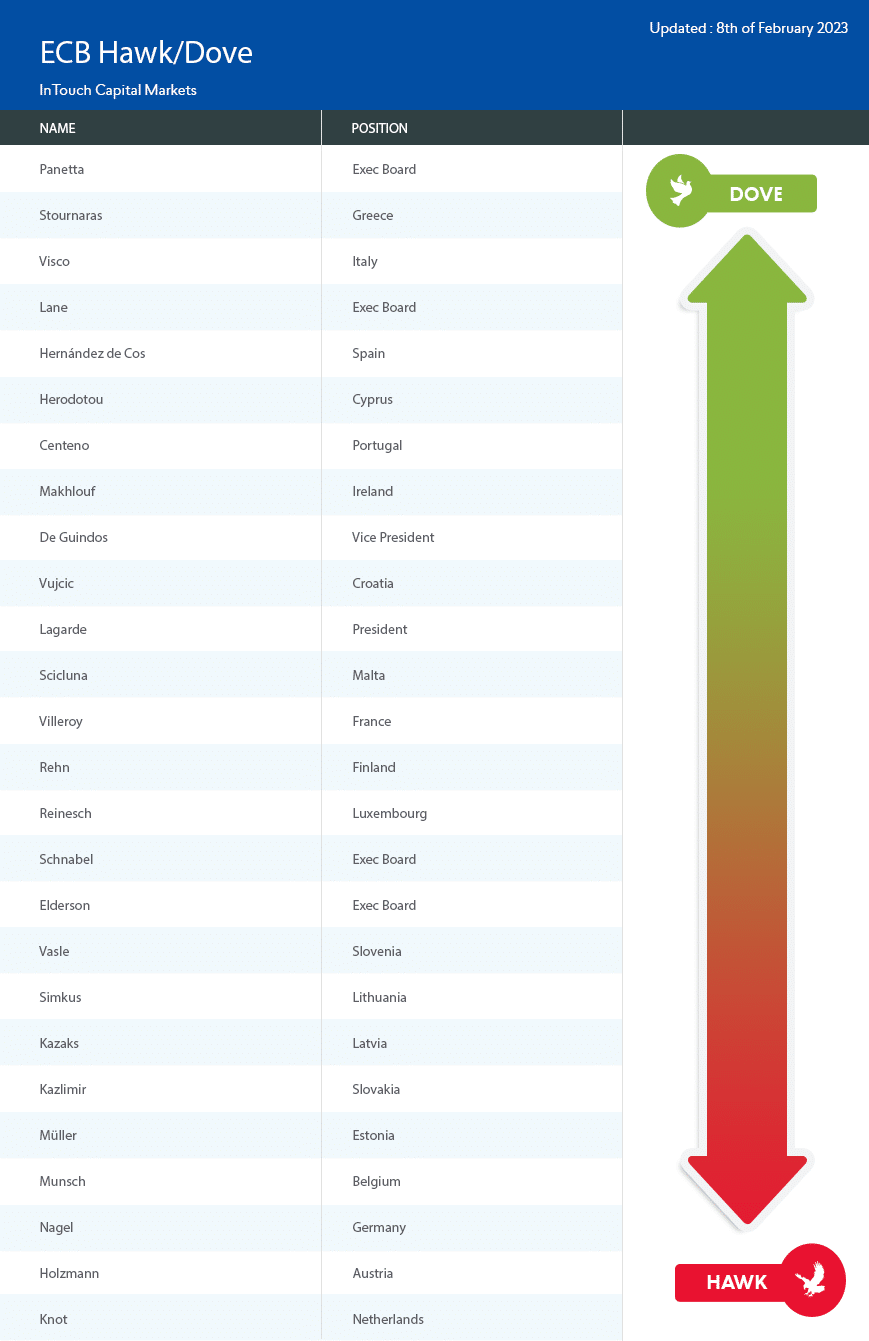

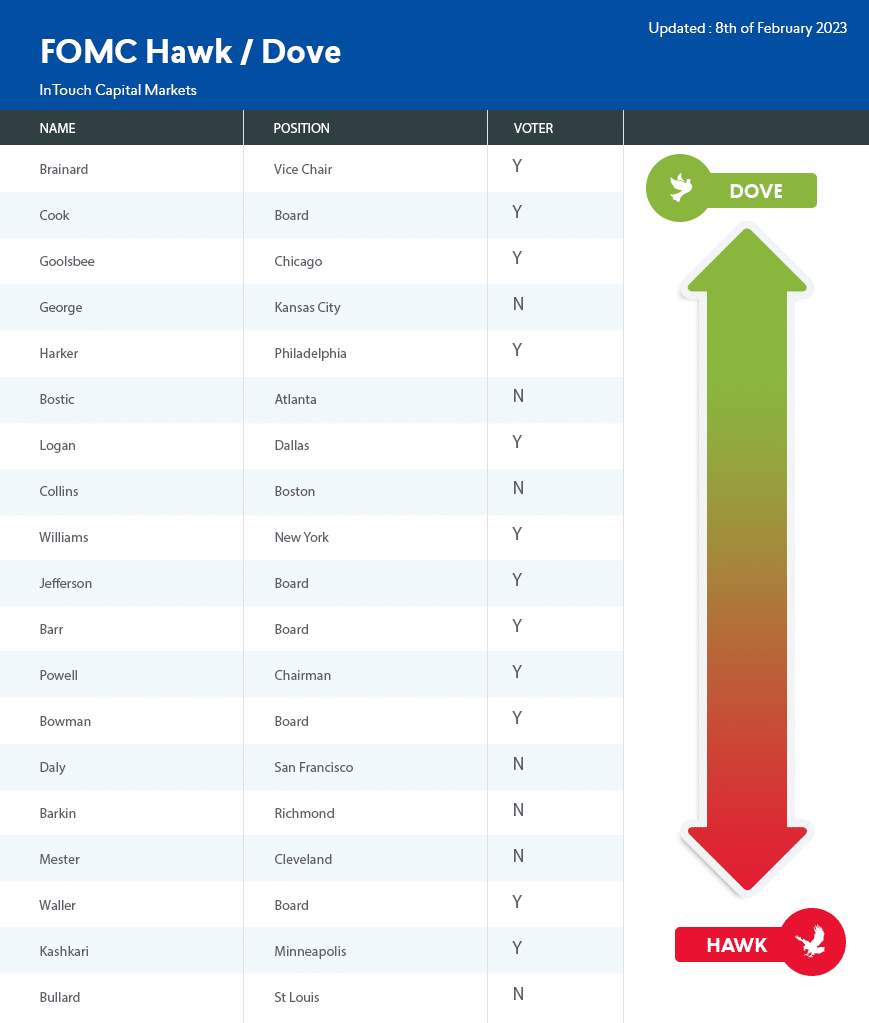

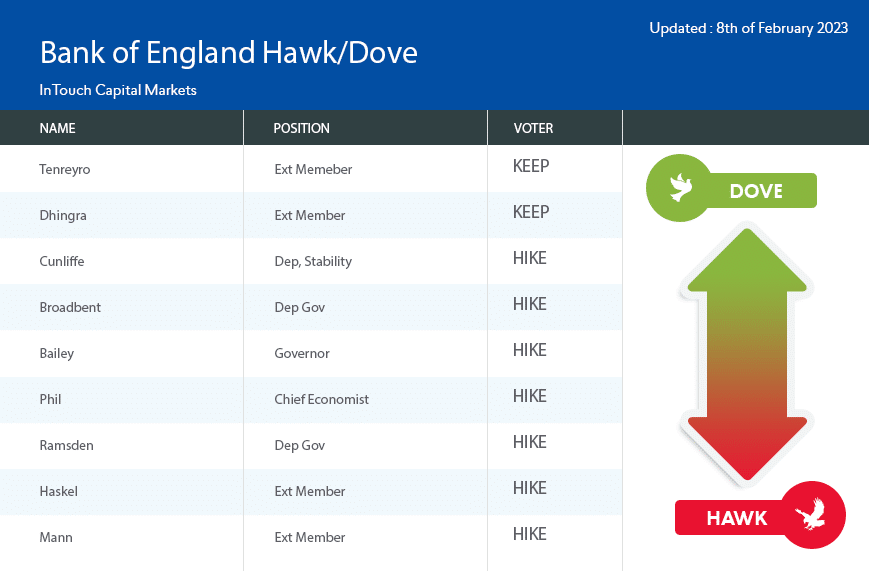

So the Hawkish or Dovish views of Central Bankers can have a direct effect on currency rates. Here we provide a guide to US, UK and European Central Bankers hawkish or dovish leanings, to provide an insight as to whether their expressed views are more or less hawkish or dovish than would be expected.

2022 big shift to hawkishness

Late 2021 marked the beginning of a shift across global central banks to a far more hawkish tone from central bankers, which then set the theme for 2022. Leading this shift to a more hawkish outlook has been the Federal Open Market Committee (FOMC) in the US, the interest rate and monetary policy committee of the US Federal Reserve, the US central bank. However, they have far from been alone in the shift to a more hawkish outlook in 2022, with the Bank of England (BoE) hiking rates throughout this year, and even the European Central Bank, amongst the more dovish of central banks, even increasing interest rates.

Surging inflation drive hawkish views

The hawkish shift experienced in 2022 has primarily been driven by surging inflation rates (which are increases in prices). One of the main drivers of these higher prices has been the war in Ukraine, which has sent energy prices rocketing higher and also seen large increases in the price of other commodities, particularly food. As well as the war in Ukraine, the high levels of global inflation have been intensified by the impact of supply chain bottlenecks as the global economy continued to emerge from the impact from the Covid-19 pandemic.

Hawk/ Dove outlook for 2023

The big question as we come towards the end of 2022 is, will this extreme hawkishness that has been seen across global central banks continue into 2023? With global inflation still at extremely elevated levels, the risk into year-end and then on into at least the first quarter and possibly the first half of 2023 remains for central bankers to continue to impose more stringent monetary policy, that is to say rising and higher interest rates, and continue with their hawkish rhetoric.

However, any signs of a curtailing of inflationary pressures will likely see central banks start to pivot away from a more intense hawkish tone and maybe start to express and more dovish outlook. This will be all the more likely if global growth rates and employment levels see significant falls and indicate potential for a protracted and/ or deep recession. Alongside the central bankers, traders should be intensely watching the global inflation data and the comments from central bankers!

Updated 2018-11-21

Federal Open Market Committee (FOMC)

Bank of England

ECB