- OECD has a gloomy economic outlook for 2019 and 2020

- The only inflation is in financial assets

- It is time to put all banks through a series of radical stress tests and let the weak fail

- The required reforms do not include nationalising the banking system

The Organisation for Economic Cooperation and Development (OECD) recently said in a report that the global economy may weaken to a pace not seen since the financial crisis a decade ago.

Global economic growth is likely to slow to 2.9% in 2019 and only just rise to 3.0% in 2020. The OECD cited the trade war between the U.S. and China as well as Brexit and tension in the Middle East as the key features that are placing future growth prospects in danger.

The unvarnished truth is that the global economy finds itself in a situation where all the ingredients for a new international financial crisis are falling into place. The worrying fact is that we do not when it will occur or what form it will take. However, one thing is for sure, the ripples will spread across the world.

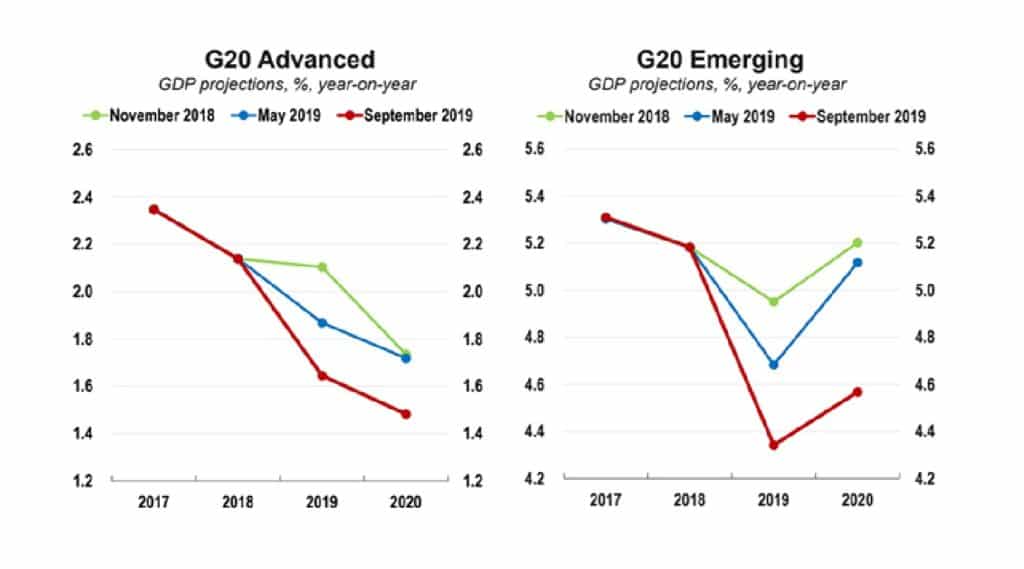

Indeed, if one divides the G20 economies into “Advanced” and “Developing”, the impact appears to be serious for both groups, Figure 1.

Figure 1: G20 Advanced and Developing Economic GDP Growth Projections. Source: OECD

What are the key reasons why the OECD have taken such a gloomy view?

They are quick to cite the increase in corporate private debt and the growing speculative bubble that is seen in financial instruments. Look at the returns in the equity, bond and real-estate sectors.

| Asset | December 31, 2018 | September 20, 2019 | Change |

| FTSE World Equity | 300.96 | 346.76 | +15.53% |

| U.S. Treasury 10-Year | 2.686% | 1.722% | -94.6 bps |

| German Bund 10-Year | 0.246% | -0.525% | -77.1 bps |

| FTSE U.S. 100 Real Estate | 4485.47 | 5238.90 | +16.80% |

Table 1: Asset Returns, Year-To-Date Source: www.investing.com

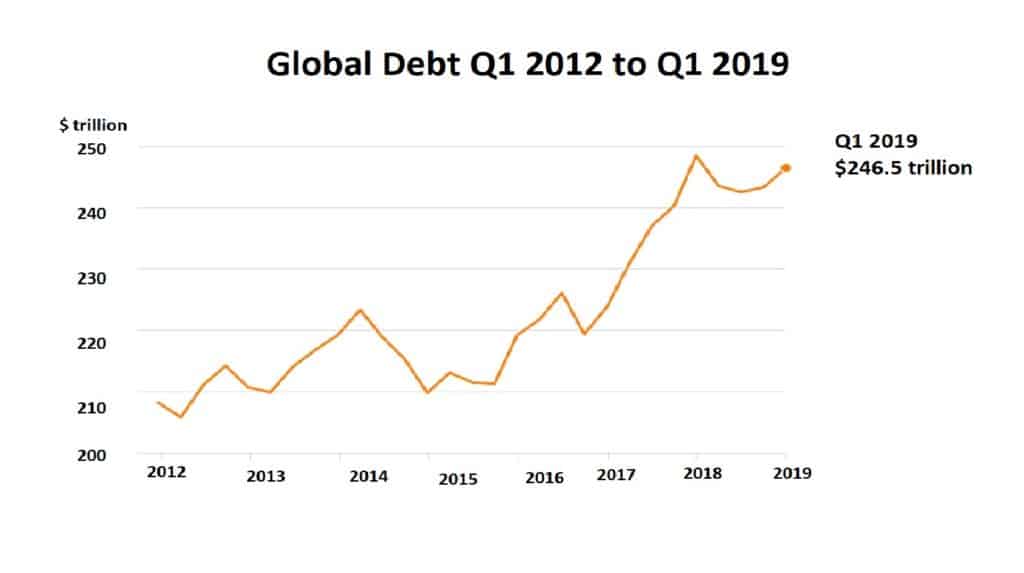

Another issue is the level of debt in the world which rose by $3 trillion in Q1 2019. This was an almost unprecedented increase that brought total global debt to $246.5 trillion.

This matters to global prospects as high levels of debt place nations, corporations and individuals in a vulnerable position in the event of a downturn, (just ask the Greeks) and could endanger the economic recovery. On this point the Institute of International Finance (IIF) fully concur with the OECD.

For all the complaints about austerity programmes, Emre Tiftik, IIF’s Deputy Director of Global Policy Initiatives said in general debt levels have grown. The slowdown in debt accumulation from 2018 to 2019 is looking more blip than trend, Figure 2.

Even private sector corporations that have vast amounts of cash at their disposal, e.g. Amazon and Apple are willing to issue large debts as they can take advantage of the low interest rates to lend the money they borrow to others. Apple is well known as seeking borrowings to lend, rather than to invest in production. Amazon, Apple etc. also borrow in order to buy its own stock on the market.

The mountain of debt, personal, corporate and government may well prove to be the root cause of the next financial crisis. However, I have grave concerns about the banking system at large.

Figure 2: Global Debt Q1 2012 to Q1 2019 Source: IIF

The rapid rise in asset prices as listed above could well be described as bubbles. As such they have drawn the eye of the world’s leading central banks namely; the Federal Reserve (Fed), the European Central Bank (ECB), the Bank of England (BOE). Indeed, whilst they have observed this phenomenon over the past decade the Bank of Japan (BOJ) has issued warnings since the real-estate bubble burst in the 1990’s.

They have collectively injected trillions of Dollars, Euros, Pounds and Yen into their respective monetary systems hoping the money multiplier would keep the system afloat. Critics of this “Quantitative Easing” or QE argue that the injections have not filtered down to the real economy, lifted productivity or wages. Instead, the only genuine sight of inflation is found in financial assets.

Left-wing leaning politicians in the U.S and Europe argue that the policy of QE demonstrates that central bank decisions are determined by short-term interests of the capitalist economy with no regard to the wider population.

The sad truth of the past decade is that a diminishing amount of retained earnings or borrowing is directed toward reinvesting in production. In contrast an increasing amount is devoted to dividends for shareholders, re-purchases of shares, and speculative investments.

No wonder the “Financial Times” author, Martin Wolf has felt compelled to write a critique of rentier capitalism. Whilst I loathe to look to the left for any economic solutions the Marxists define “Rentier Capitalism” as the belief in economic practices of monopolisation of access to any kind of property and gaining significant amounts of profit without contribution to society.

The fact that financial assets have risen amid a tepid backdrop of economic growth is leading to increases questions of can the free-market, capitalist economy and democracy survive?

Rentiers are widely considered to be damaging because they extract “unearned” value from the economy. They invest in unproductive assets, such as real estate, or reap excessive profits through the monopolistic control of property or infrastructure.

The intervention of the central banks has not allowed the system to be flushed of the weak and underperforming. In fact, the flow of ultra-cheap money has allowed the weakest elements to survive and decrease their ratio between equity i.e. the company’s capital and the debt taken on by the company.

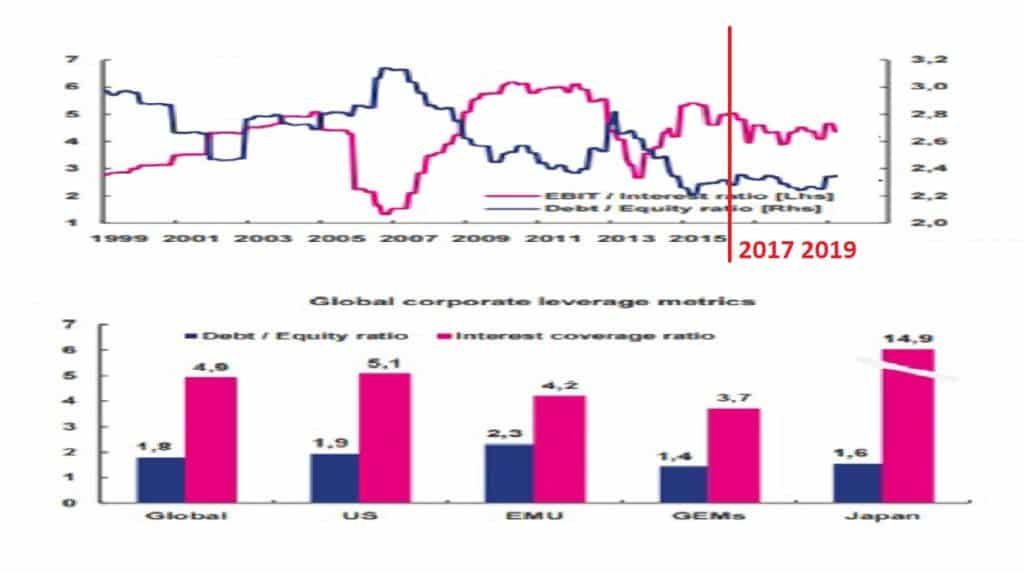

Across the U.S., Europe and Japan…why even in China the ratio is way too low, Figure 3.

Figure 3: Debt /Equity Ratios are falling Source: Bloomberg and Datastream

It is a figure that should instil confidence that the company could deal with the loss of value that would be caused by a fall in the price of stocks, bonds or other financial assets held. They have had it too easy as investing clients have queued up t buy debt that offers a hint of a positive return whereas much sovereign debt yields very little to negative returns.

Continued QE by the ECB and the Fed is supposed to help the economy, but it is increasing looking like the return visits to the QE well off a diminishing return to scale.

Critics say the Fed has not followed through on the pledge to sell off toxic private debt securities and at the end of Q1 2019 it had $1.6 trillion in Mortgage Backed Securities (MBS) on its books that were first acquired in 2008-2009 from the big banks in order to bail them out. Let’s put on a hat of common sense here. It is just market wise not to sell too much too quickly. If they did the price would plunge and the collapse could easy shake confidence so badly as to drag down the entire U.S. bond market.

The ECB continues lending cash to banks at 0% interest and has just promised them not to increase that rate before 2020. However, before Mario Draghi signs off he has ruled that the ECB is going to grant the private banks a new wave of large-scale middle and long-term maturity loans. These are known as Targeted Longer-Term Refinancing Operations (TLTRO’s).

It is principally the Italian and Spanish banks who are in dire need of this this credit line and they will most likely account for 60% of the total of new TLTRO issuance. This money is not used to cleanse the balance sheet. Oh no! It is part of the great Eurozone game of money illusion. European banks use the facilities extended by the ECB to buy government debt issued by their own and other nations…and then when the ECB announces a new round of QE, the banks will sell the ECB the bonds they bought with ECB money.

The profits they make will go toward squaring their debt with the ECB. It is nothing more than a game of passing the Euro’s around so that very few banks will ever have to go bust. They do not care about buying debt with a negative yield as they can sell their holdings for a profit to the buyer of last resort, i.e. the ECB.

This is not just an issue for the west. On Friday, September 6, the People’s Bank of China (PBOC), announced that it will cut the required reserve ratio for all commercial banks, freeing up long-term funding of around Yuan 900 billion ($126 billion) that banks will be allowed to deploy in boosting lending and support government efforts to stabilise up the real economy.

The 0.50% cut in the amount of reserves banks are required to hold at the central bank will be effective from September 16, the PBOC said. The required reserve ratio cut would boost bank’s lending capacity and more importantly lower their cost of capital received from the central bank.

Growth in China is still slowing and is forecast to be in the neighbourhood of 6% this year the lowest rate in 25 years. In China, a financial crisis can erupt at any time, causing domestic and worldwide growth to plummet and deteriorating living conditions for hundreds of millions of Chinese.

As Figure 1 illustrated the growth projections for the G20 emerging nations has been pared back by the OECD. The only exception is India which is still growing at 7%. Russia is experiencing very weak growth, around 1.2% in 2018 and a forecast of 1.3% for 2019. South Africa was in recession during H1 2019 and Brazil the leading economy of Latin America is has a low rate of barely over 1% in 2018.

The approaching new financial crisis falls within a much broader systemic crisis of global capitalism and is multi-faceted, with economic, environmental, social, political, moral, and institutional dimensions. As such there needs to be a radical break with the past. When a crisis hits, those responsible should be held accountable. Hardly any financier that sparked the financial crisis served jail time.

I do not advocate a ban on short selling as that boosts liquidity and determines real value. Nor do I want to see a financial transactions tax bought in. That was tried in the Swedish market in 1984 to 1991. When introduced, prices fell heavily, volumes all but collapsed and foreign trading quickly moved from Stockholm to Copenhagen.

If we can agree that the banking sector is essential to the success of a modern economy measures that can support and reshape the structure of the financial world and capitalist system should be implemented. This does not mean taking the banking sector under state control. It would be unaffordable, and it is a recipe for the state directing how loans are allotted. In short, lame duck enterprises will be supported.

We must be cruel to be kind and let zombie banks fold. They are of no use to society and are unlikely to ever recover. Once was enough for bailing out the banks, and it has been accepted that any further use of public debt that is hypothecated to save ailing banks is clearly illegitimate.

Let us have the central banks set hard, stress tests, not the lazy, soft approach that was adopted by the ECB. The audit must be conducted with bared teeth to determine other odious and unsustainable debts. Clear out the weak and then ensure that at the survivors all deposits are ring fenced. Isolate any proprietary so that if such a unit at Bank A fails, it only loses its own capital. It does not drag the parent bank down as well. Finally, reduce the reserve requirements but stop main banks accumulating sovereign debt to excessive levels so that t can be sold back to the central bank. That must stop as a way of weening the financial system off QE.

Only by following a course of action can we ever hope to return an era of sound money, normalised rates and a world where central banks resume their role of printing money and contribute actively to financing the expansion of a healthy market economy.