We know from Fed Chair Powell at the July FOMC meeting that the Federal Reserve is data-dependent. It means that the data for the US labour market and inflation this month and next month (that comes out before the September FOMC meeting) will be crucial in helping to formulate the monetary policy decisions in the final three meetings of the year. Today’s downside surprise in US CPI (albeit marginal) continues to paint the picture of falling inflation pressures. This adds to the list of excuses for the Fed not hiking again. This is weighing on the latest USD rebound and could be key for the timing of opportunities on major pairs.

- US CPI was lower than forecast on both headline and core measures

- Expectations of Fed rate hikes are waning further

- A USD rally is waning, opening potential opportunities on pairs such as EUR/USD and GBP/USD

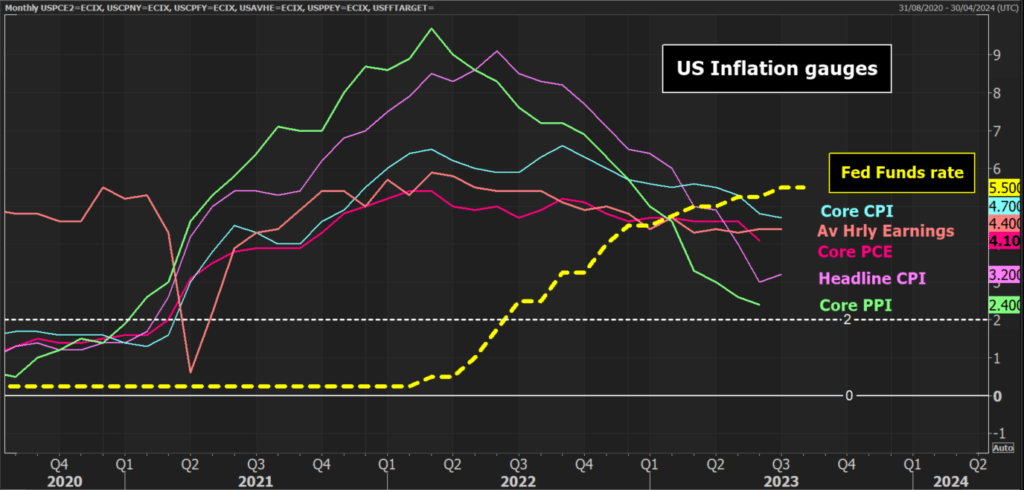

The moderation in US CPI continues

US CPI inflation increased by just +0.2% on the month for both headline and core CPI. This was broadly in line with expectations. However, on a 12-month basis, inflation surprised to the downside on both.

- Headline CPI increased slightly to 3.2% in July (from 3.0% in June) which was lower than the consensus forecast of 3.3%.

- Core CPI dropped again to 4.7% in July (from 4.8%) with the consensus having forecast inflation to stay steady at 4.8%.

Crucially, if the Fed is looking at the monthly run rates of the inflation data it is clear that the data is returning to far more acceptable levels. Monthly headline CPI has been at or below +0.2% for three consecutive months (despite the year-on-year CPI increasing slightly), with core CPI at +0.2% for the past two. Both of these are broadly around where the Fed would want to see them for inflation to get back towards the 2% target.

This is good news for the Fed and the economy as a whole. If inflation remains on this path lower, then with the labour market remaining solid and many no longer predicting a recession, the prospects of a soft landing have taken another step towards coming to fruition.

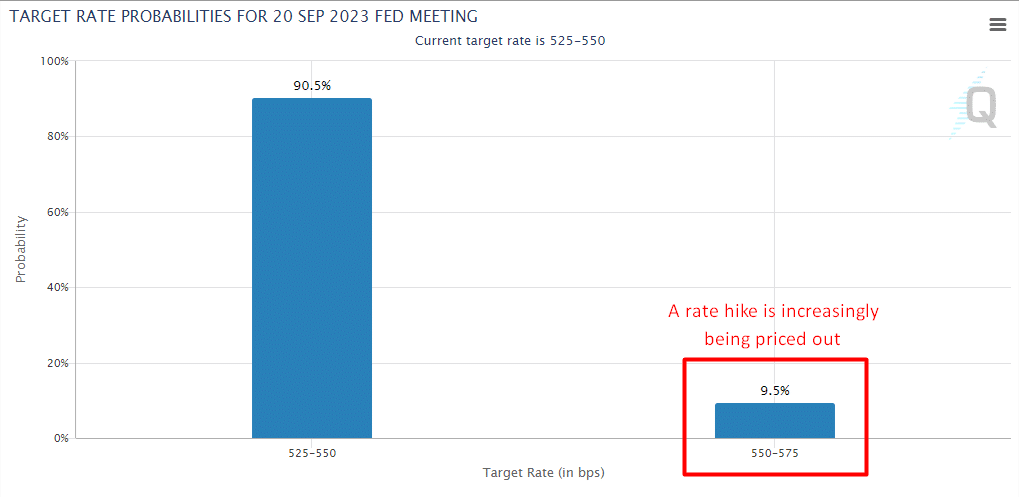

A September hike becomes even less likely

I said earlier that the data was crucial in front of the next FOMC meeting (the announcement is on 20th September). There is one more Nonfarm Payrolls and one more CPI release before that meeting. However, with the mixed payrolls report last week and this week’s marginally softer inflation, the data is pointing towards the Fed being on pause in September.

At least, that is what the interest rate futures are telling us. Last week, before the Nonfarm Payrolls report, according to CME Group’s FedWatch tool, the probability of a September hike sat at around 20%. This then fell to around 13% in the wake of the mixed jobs report. The probability has now fallen to around 10% after the July CPI.

We can see this also through the lens of US Treasury yields. Yields have fallen in recent days, but also have dropped back on the CPI data. Both the 2-year and 10-year Treasuries have fallen a couple of basis points (although yields have bounced off their session lows).

The impact of this fall in Treasury yields has been to weigh on USD too. The USD is weakening versus all major currencies apart from the Japanese yen today.

Is this an opportunity for USD pairs?

The USD has been recovering over the past few weeks. However, this CPI print, with the associated USD weakness poses a question. Is this an opportunity to trade USD pairs? Looking at the technical analysis of major pairs such as EUR/USD and GBP/USD, I think that there are such opportunities now. However, I will still be needing some confirmation first.

Starting with EUR/USD, there has been a corrective move back from 1.1275 as the USD has strengthened recently. However, support has already been threatening to leave a key low at 1.0910 in the past week. A small higher low (at 1.0927) has been followed by a higher high today (above the 1.1041 high from last week. A close above 1.1041 would be the signal for renewing upside momentum for near-term gains.

I am also looking for confirmation of the improvement with the Relative Strength Index momentum indicator. The RSI is already back above 50 and if this continues to rise into the high 50s it would suggest building upside momentum in a rally. The next test would be the late July lower high at 1.1149.

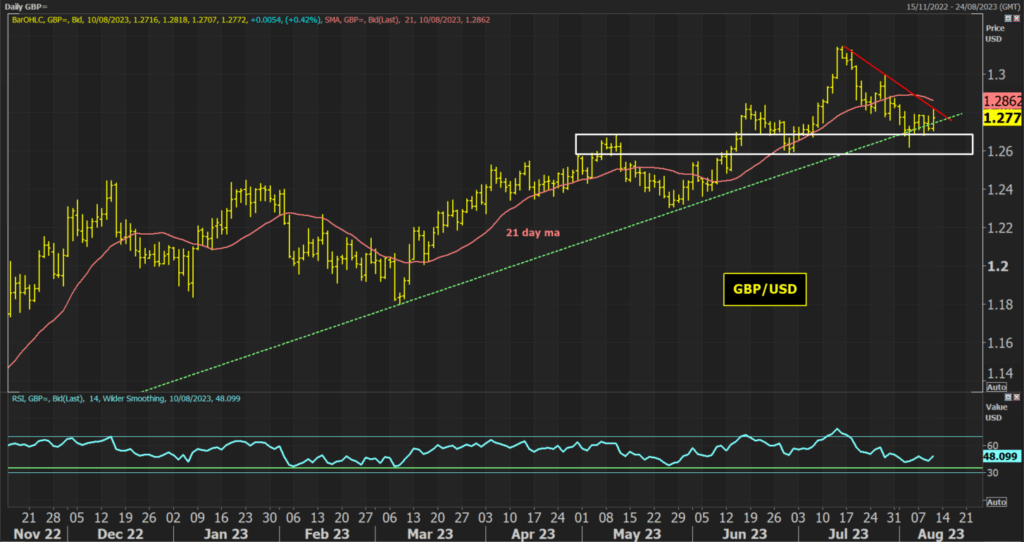

I am also looking at an improvement that is developing in Cable too. The near-term correction in GBP/USD has brought the pair back to the support of what has been a nine-month uptrend, but more importantly, the breakout support between 1.2590/1.2680. This support has come under considerable scrutiny but is holding. The key is whether Cable can now rally to break the resistance of a near four-week downtrend.

I will be looking closely at two technical indicators now. The daily RSI has been holding up well above 35 but if this now moves above 50 it would be a signal of improving momentum with the rally. Furthermore, the 21-day moving average has been a strong gauge for the near-term outlook, acting as support during the bull phases and resistance during the corrective moves. A move above this moving average would signal to me that the bulls are ready to push ahead again.